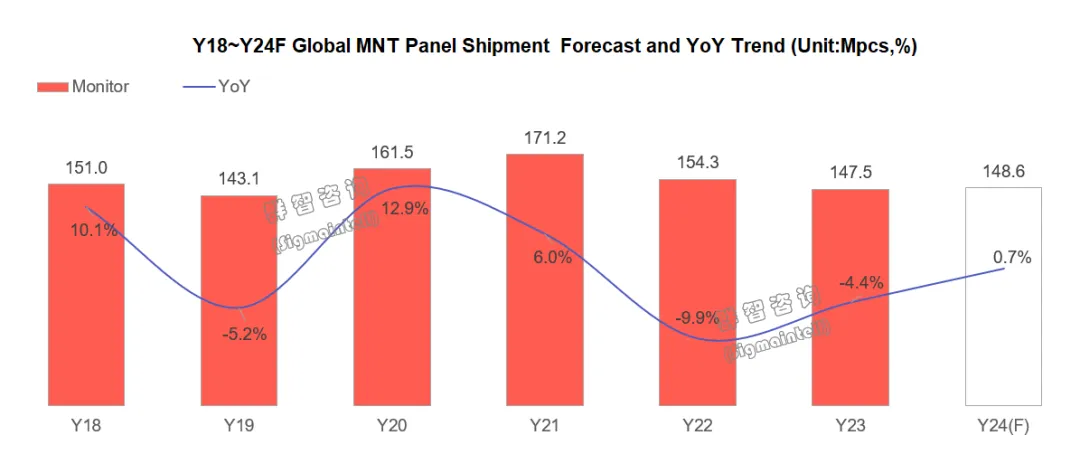

Qunzhi Consulting: Global display panel shipments are expected to reach 149 million pieces in 2024, a slight increase of 0.7% year-on-year

The Zhitong Finance App learned that Qunzhi Consulting published an article stating that the challenges facing the global display panel industry in 2024 still exist. On the one hand, uncertainty in the macroeconomic environment will continue to affect market demand. Slowing global economic growth and increasing geopolitical risks are likely to have a negative impact on the display panel industry. On the other hand, changes in the demand structure have also brought new challenges to the industry. The recovery in commercial demand is uncertain, and consumer demand has been overdrawn to a certain extent ahead of schedule, which will put pressure on future market growth. According to statistics from Qunzhi Consulting, benefiting from the optimization of panel inventory, global display panel shipments are expected to reach 149 million pieces in 2024, a slight increase of only 0.7% over the previous year.

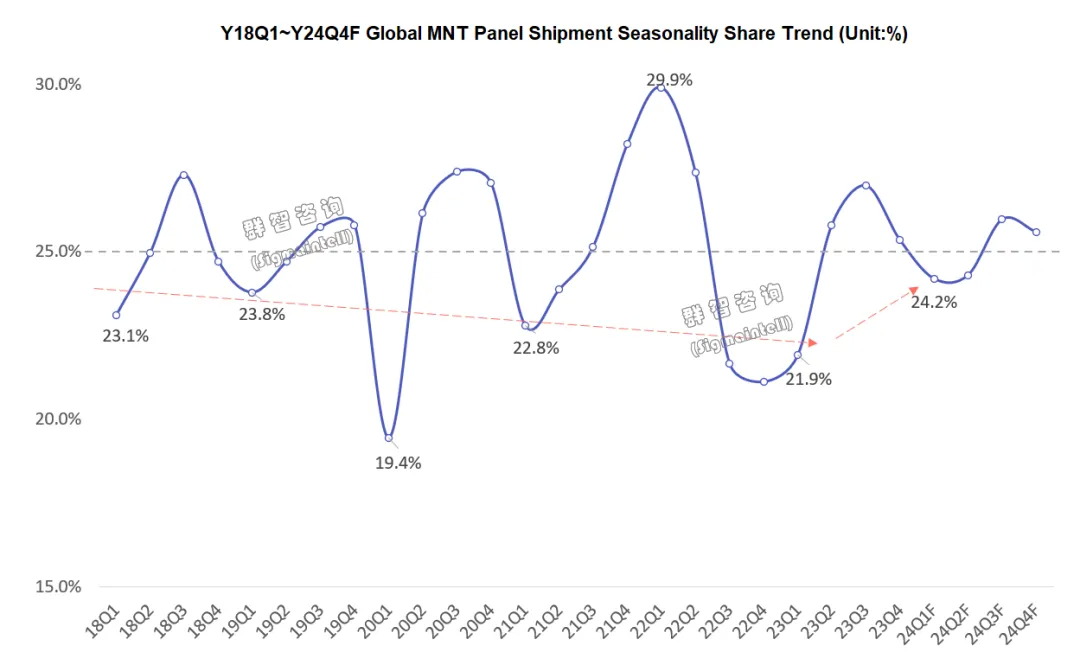

It shows that industrial stocking usually has certain seasonal characteristics. Due to the influence of holidays such as the Spring Festival, the first quarter is often a period for enterprises and consumers to adjust inventory and purchase plans, making it a traditional low season for procurement. However, this year, under the influence of multiple factors such as limited supply, increased shipping time, and rising panel prices, most brands have strategically increased demand for display panels in the first quarter. The Q1 shipment scale was significantly higher than expected, accounting for about 24.2% of annual shipments, changing the “traditional off-season” image of the past. The supply situation in the second quarter will be further limited, and the increase in the scale of shipments will be limited. Overall, although the recovery in total display panel shipments in 2024 was limited, the seasonal index adjustment of panel demand accelerated.

Panel supply: Production control has become the norm, and monitor supply priorities are at a disadvantage

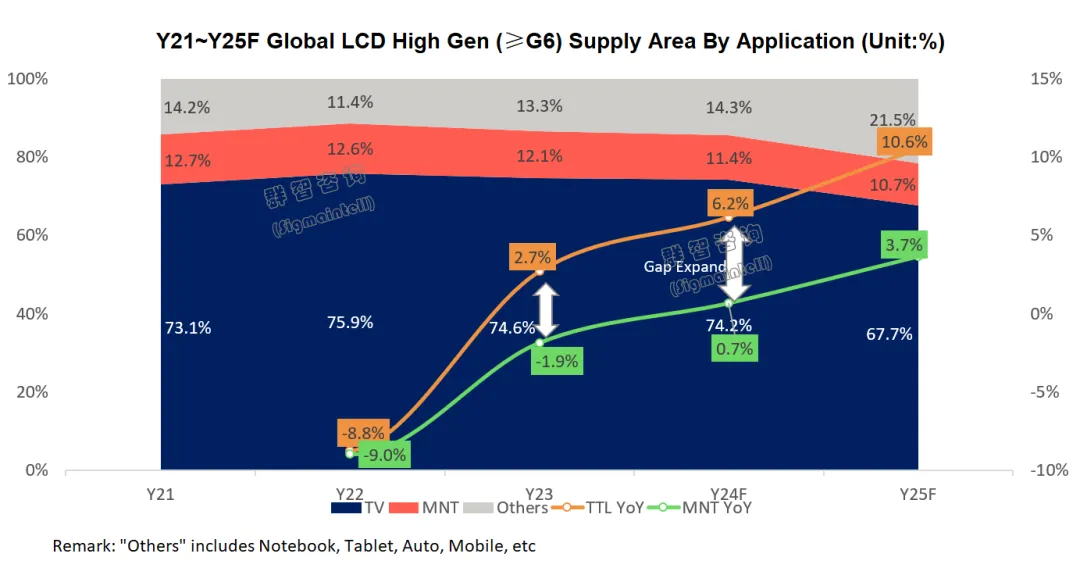

In recent years, with the continuous expansion of high-generation production capacity, it shows that industrial supply has become quite adequate. However, declining market demand and profit pressure forced panel manufacturers to adjust their strategies and increase production control efforts to cope with drastic changes in the market. Large-scale applications are the most effective way to reduce production capacity. At the same time, in order to improve profitability, large-scale applications are particularly effective in controlling production. In small-sized applications, such as laptops, tablets, vehicles, mobile phones, etc., with the continuous advancement of technology and diversification of demand, the requirements for display panels are also getting higher and higher. In order to optimize costs and product structure, production capacity for small-size applications is gradually being transferred to higher generation lines.

According to the Qunzhi Consulting Panel Capacity Database tracking, the share of small-size applications (others) in the global medium- and high-generation (≥G6) LCD production capacity area allocation continues to grow, and the share of large-size applications (TV, monitor) production capacity area is gradually shrinking. Under large-scale application production control, the price of TV panels has risen above the profit level in 2023. Looking ahead to 2024, the global LCD supply area (≥G6) is expected to increase 6.2% year on year, but the monitor application capacity area is expected to increase by only 0.7% year on year. The gap between changes in total production capacity area and changes in the single Monitor application area continues to widen, and the strategy of “controlling production and price increases” is gradually being transmitted to Monitor applications.

Looking at the G8.5 & G8.6 LCD production line, since the comprehensive cost of a single-board monitor is significantly higher than that of a TV, in order to ensure appropriate profit margins, the monitor's ASA (average sales price per square meter) is often significantly higher than TV ASA. According to the Qunzhi Consulting Panel revenue analysis database, in January 2022, the G8.5 23.8 “FHD IPS OC ASA is about 2.8 times that of the 55" UHD OC. However, as the price difference between the two gradually narrows in 2023, the ASA difference has shrunk to around 1.2 times. This change shows that the Monitor application is not only facing pressure from the overall market, but also from other internal applications. In the context of continuous production control, panel manufacturers have made drastic adjustments to capacity allocation in different application areas in order to cope with market changes and improve profitability. Since the Monitor application lost its advantage in terms of revenue and loss in profit, its production capacity allocation priority has clearly lagged behind that of TV.

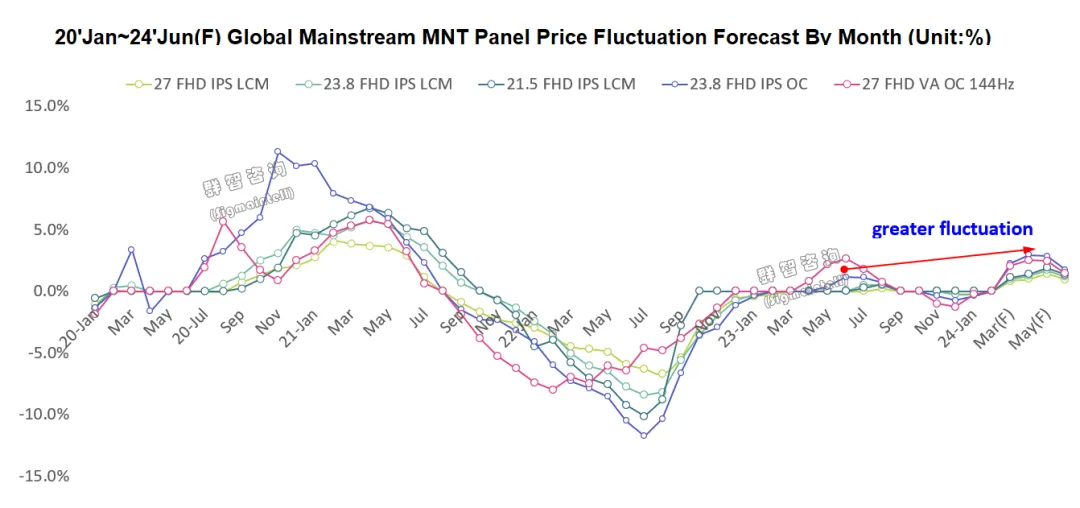

Panel price: Expanding monitor panel price fluctuations in 2024 will push the terminal market out of the “price war”

Entering 2024, it has become the consensus of panel manufacturers to urgently improve Monitor's profitability. The formation of this consensus is not only a deep understanding of the current market situation, but also an accurate grasp of future development trends. Looking at the supply side of the market, under limited production capacity resources, the Monitor production capacity allocation is gradually being squeezed. This has caused the Monitor market to gradually lean towards the supply side, and the market supply is gradually tight. As a result, the rise in panel prices has become a general trend. At the same time, panel manufacturers focus not only on the short-term trend of rising panel prices, but also on how to achieve Monitor's annual profit target and how to ensure the long-term healthy development of the industry.

According to the Qunzhi Consulting panel price monitoring database, the price fluctuation of monitor panels in 2023 is significantly weaker than that of TVs, but this year this year, this trend will change markedly. Driven by panel manufacturer price strategies, monitor panel price fluctuations are expected to expand significantly in 2024.

The rise in monitor panel prices not only helps improve the profit status of panel manufacturers, but also helps slow the price war in the display terminal market. There is no doubt that price increases in the short term will increase the cost pressure on brands, but in the long run, breaking out of the price war can drive the return of brand value in the terminal market, enhance the technological innovation vitality of all links in the industrial chain, and ultimately enhance the sustainable development capacity of the entire industry chain. It is undoubtedly a win-win choice for panel manufacturers and brands.