Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalNEXTURNBIOSCIENCE Co., Ltd.'s (KOSDAQ:089140) 33% Price Boost Is Out Of Tune With Revenues

NEXTURNBIOSCIENCE Co., Ltd. (KOSDAQ:089140) shares have had a really impressive month, gaining 33% after a shaky period beforehand. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 31% in the last twelve months.

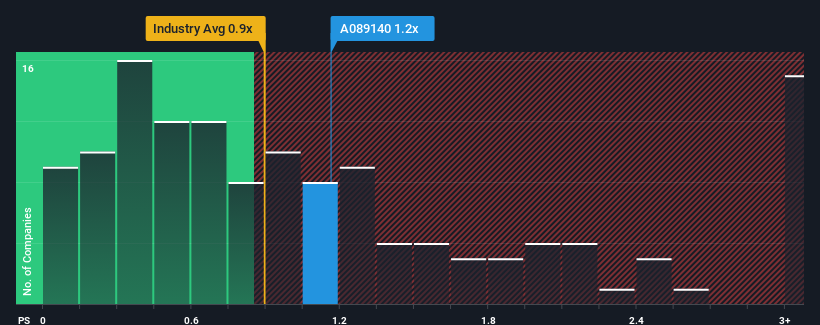

Even after such a large jump in price, it's still not a stretch to say that NEXTURNBIOSCIENCE's price-to-sales (or "P/S") ratio of 1.2x right now seems quite "middle-of-the-road" compared to the Machinery industry in Korea, where the median P/S ratio is around 0.9x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for NEXTURNBIOSCIENCE

How Has NEXTURNBIOSCIENCE Performed Recently?

As an illustration, revenue has deteriorated at NEXTURNBIOSCIENCE over the last year, which is not ideal at all. One possibility is that the P/S is moderate because investors think the company might still do enough to be in line with the broader industry in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

Although there are no analyst estimates available for NEXTURNBIOSCIENCE, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

NEXTURNBIOSCIENCE's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered a frustrating 1.1% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 132% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

This is in contrast to the rest of the industry, which is expected to grow by 36% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this in mind, we find it intriguing that NEXTURNBIOSCIENCE's P/S is comparable to that of its industry peers. Apparently many investors in the company are less bearish than recent times would indicate and aren't willing to let go of their stock right now. They may be setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

What Does NEXTURNBIOSCIENCE's P/S Mean For Investors?

Its shares have lifted substantially and now NEXTURNBIOSCIENCE's P/S is back within range of the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of NEXTURNBIOSCIENCE revealed its poor three-year revenue trends aren't resulting in a lower P/S as per our expectations, given they look worse than current industry outlook. When we see weak revenue with slower than industry growth, we suspect the share price is at risk of declining, bringing the P/S back in line with expectations. If recent medium-term revenue trends continue, the probability of a share price decline will become quite substantial, placing shareholders at risk.

We don't want to rain on the parade too much, but we did also find 3 warning signs for NEXTURNBIOSCIENCE that you need to be mindful of.

If these risks are making you reconsider your opinion on NEXTURNBIOSCIENCE, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.