Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalUncovering Three Promising UK Stocks with Strong Potential

In the last week, the United Kingdom market has stayed flat, yet it has risen by 6.5% over the past year with earnings projected to grow by 14% annually in the coming years. In this environment, identifying promising stocks involves looking for companies with strong fundamentals and growth potential that align well with these positive market trends.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Livermore Investments Group | NA | 9.92% | 13.65% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| Metals Exploration | NA | 12.92% | 73.62% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| VH Global Sustainable Energy Opportunities | NA | 18.30% | 20.03% | ★★★★★★ |

| Kodal Minerals | NA | nan | 72.74% | ★★★★★★ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

Here we highlight a subset of our preferred stocks from the screener.

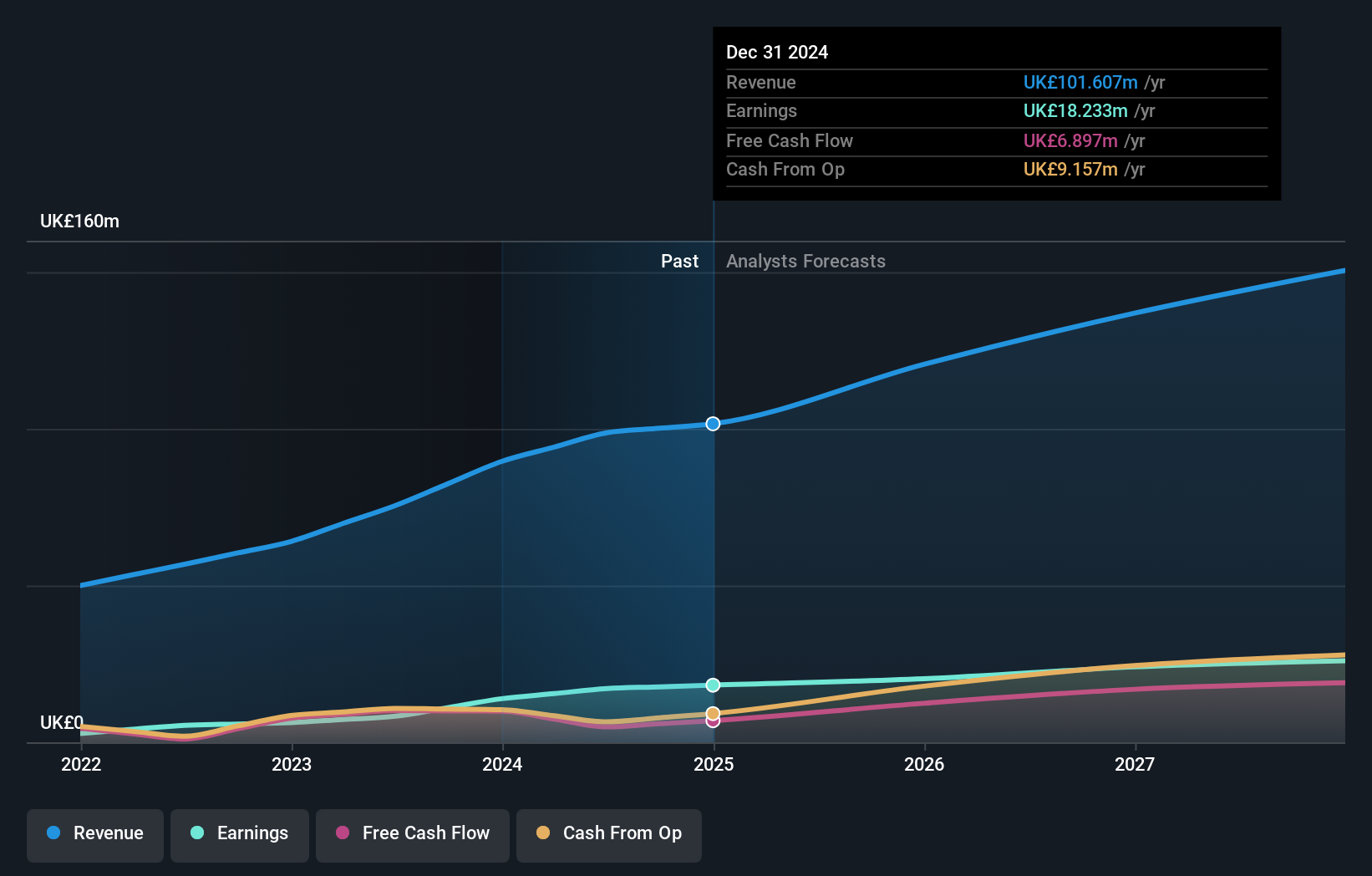

Warpaint London (AIM:W7L)

Simply Wall St Value Rating: ★★★★★★

Overview: Warpaint London PLC, along with its subsidiaries, is engaged in the production and sale of cosmetics and has a market capitalization of approximately £435.36 million.

Operations: Warpaint London generates revenue primarily through its Own Brand segment, contributing £96.72 million, while the Close-Out segment adds £2.12 million. The company's financial performance is significantly driven by its Own Brand offerings.

Warpaint London, a nimble player in the beauty industry, has shown impressive financial strides with earnings soaring by 106% over the past year. The company is debt-free, having reduced its debt to equity ratio from 4.4% five years ago to zero today. Recent half-year results revealed sales of £45.85 million and net income of £8.02 million, both up from last year’s figures. Despite share price volatility, Warpaint's robust earnings growth outpaces its industry peers significantly.

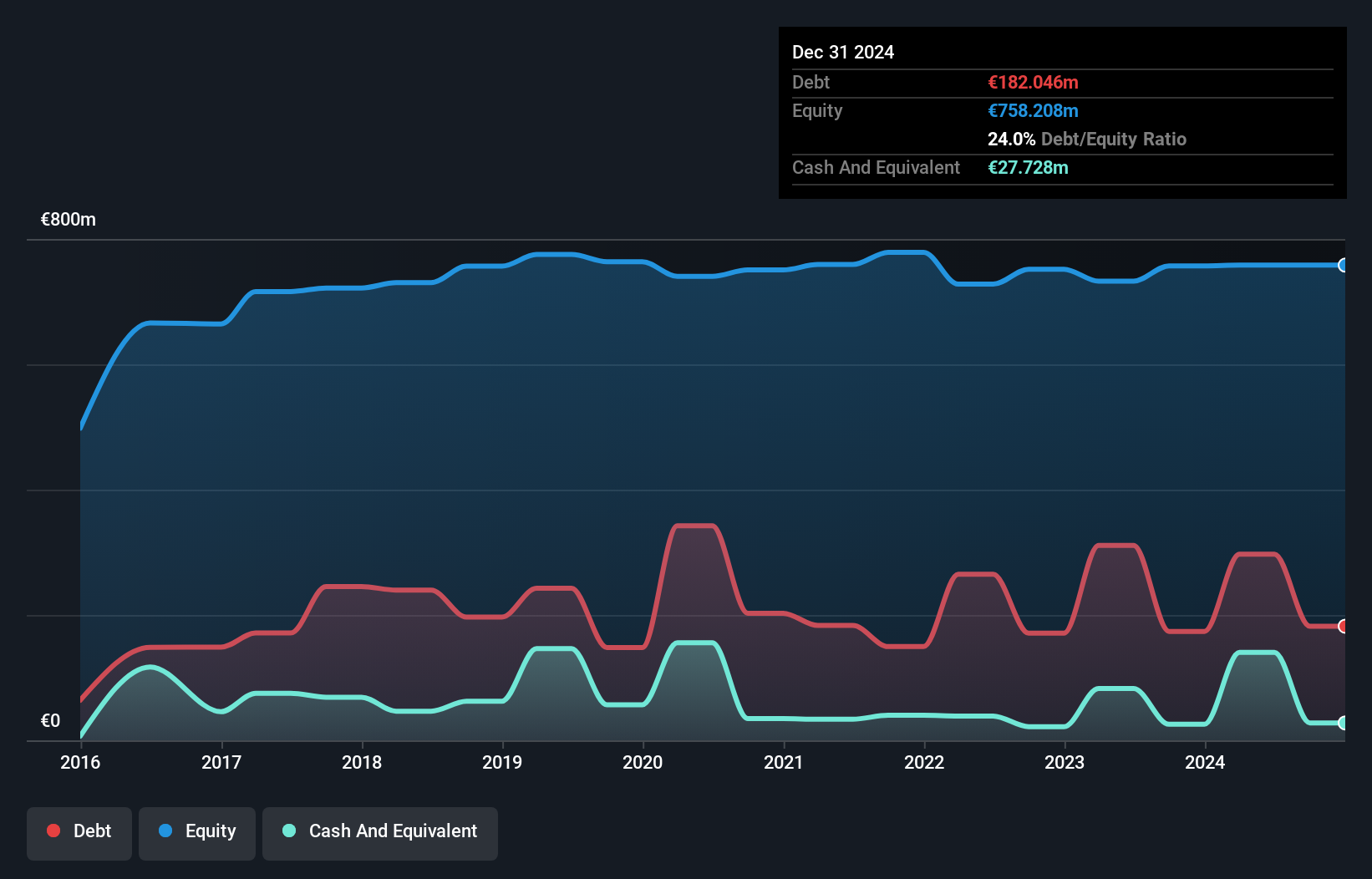

Cairn Homes (LSE:CRN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cairn Homes plc is a holding company that operates as a home and community builder in Ireland with a market capitalization of £1.10 billion.

Operations: Cairn Homes generates revenue primarily from its building and property development segment, amounting to €813.40 million.

With a net debt to equity ratio of 20.7%, Cairn Homes seems well-positioned in its industry, especially with a price-to-earnings ratio of 11.8x, which is below the UK market average. The company reported impressive earnings growth of 49.5% over the past year, outpacing its peers in the Consumer Durables sector by a significant margin. Recent buybacks saw €70 million spent on repurchasing shares, enhancing shareholder value alongside an interim dividend payout announced recently.

- Unlock comprehensive insights into our analysis of Cairn Homes stock in this health report.

Gain insights into Cairn Homes' past trends and performance with our Past report.

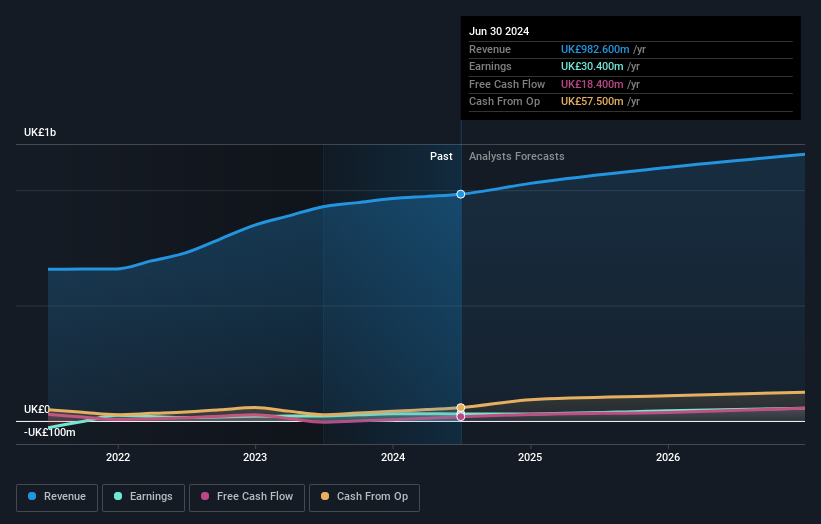

Senior (LSE:SNR)

Simply Wall St Value Rating: ★★★★★☆

Overview: Senior plc designs, manufactures, and sells high-technology components and systems for major original equipment manufacturers in various sectors including aerospace, defense, land vehicles, and power and energy across the United States, the United Kingdom, and internationally; it has a market cap of £551.24 million.

Operations: Senior plc generates revenue primarily from its Aerospace segment (£651.10 million) and Flexonics segment (£333 million).

Senior plc, a notable player in the aerospace sector, has shown promising growth with earnings rising 40.1% over the past year, surpassing industry averages. The company's net debt to equity ratio stands at a satisfactory 34.4%, reflecting sound financial health, while EBIT covers interest payments by 3.1 times, indicating robust profitability management. Recent developments include securing significant contracts with Deutsche Aircraft and Rolls-Royce and announcing a 25% interim dividend increase to 0.75 pence per share for November payout.

- Get an in-depth perspective on Senior's performance by reading our health report here.

Evaluate Senior's historical performance by accessing our past performance report.

Make It Happen

- Gain an insight into the universe of 84 UK Undiscovered Gems With Strong Fundamentals by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com