Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalBe Wary Of Carrianna Group Holdings (HKG:126) And Its Returns On Capital

When researching a stock for investment, what can tell us that the company is in decline? Businesses in decline often have two underlying trends, firstly, a declining return on capital employed (ROCE) and a declining base of capital employed. This indicates to us that the business is not only shrinking the size of its net assets, but its returns are falling as well. So after we looked into Carrianna Group Holdings (HKG:126), the trends above didn't look too great.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Carrianna Group Holdings:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.00076 = HK$2.9m ÷ (HK$6.1b - HK$2.4b) (Based on the trailing twelve months to March 2024).

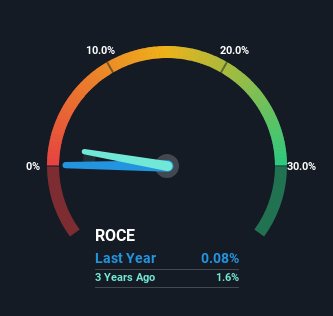

Thus, Carrianna Group Holdings has an ROCE of 0.08%. Ultimately, that's a low return and it under-performs the Hospitality industry average of 7.1%.

View our latest analysis for Carrianna Group Holdings

Historical performance is a great place to start when researching a stock so above you can see the gauge for Carrianna Group Holdings' ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Carrianna Group Holdings.

What The Trend Of ROCE Can Tell Us

In terms of Carrianna Group Holdings' historical ROCE movements, the trend doesn't inspire confidence. About five years ago, returns on capital were 2.5%, however they're now substantially lower than that as we saw above. And on the capital employed front, the business is utilizing roughly the same amount of capital as it was back then. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Carrianna Group Holdings to turn into a multi-bagger.

On a side note, Carrianna Group Holdings' current liabilities have increased over the last five years to 39% of total assets, effectively distorting the ROCE to some degree. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. While the ratio isn't currently too high, it's worth keeping an eye on this because if it gets particularly high, the business could then face some new elements of risk.

What We Can Learn From Carrianna Group Holdings' ROCE

In summary, it's unfortunate that Carrianna Group Holdings is generating lower returns from the same amount of capital. Unsurprisingly then, the stock has dived 71% over the last five years, so investors are recognizing these changes and don't like the company's prospects. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

One final note, you should learn about the 3 warning signs we've spotted with Carrianna Group Holdings (including 2 which are a bit concerning) .

While Carrianna Group Holdings may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.