AngloGold Ashanti Stock Tops 3 Dividend Ideas For Geopolitical Defense

With inflation trends diverging across regions, bond yields shifting and energy prices adding extra noise to markets, many investors are looking for ways to rely more on income rather than short term price moves. That is where Dividend Powerhouses paying 5%+ yields with coverage, growth and stability can help. Instead of guessing what central banks or housing data might do next, this screener focuses on companies with a track record of paying shareholders regularly. In this article, you will see 3 stocks from the Dividend Powerhouses screener that illustrate how this income focused approach can fit into a portfolio.

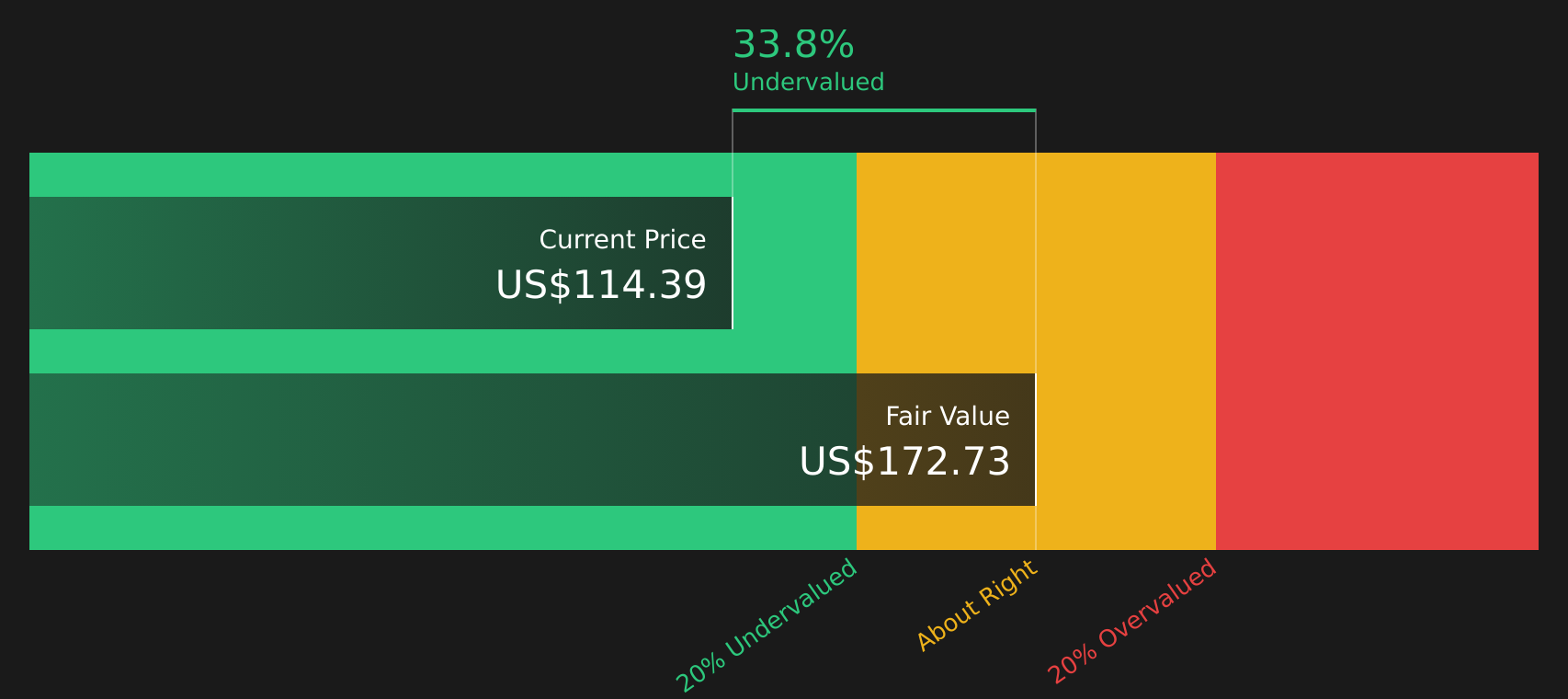

AngloGold Ashanti (AU)

Overview: AngloGold Ashanti is a global gold producer that operates mines across Africa, Australia and the Americas, with silver and sulphuric acid as by products, and its flagship Geita mine in Tanzania. The company focuses on exploring, developing and operating gold assets while returning capital to shareholders from its mining operations.

Operations: AngloGold Ashanti generates about US$11.2b from metals and mining activities focused on gold and other precious metals, with revenue primarily sourced from Africa (US$8.1b), and the rest from the Americas, Australia and an unallocated segment.

Market Cap: US$38.6b

Income focused investors may find AngloGold Ashanti interesting because it combines a high dividend yield with strong recent earnings momentum, wider profit margins and a high 39.4% Return on Equity, while also planning a US$2b share buyback that could further support shareholder returns. At the same time, the stock is assessed as trading well below fair value estimates and below sector P/E levels, although earnings expectations have been revised down recently. The key watchpoints are rising production and royalty costs, dependence on firm gold prices and an unstable dividend record, all of which can affect future payouts. To see how these factors translate into potential income durability and valuation support, the full Simply Wall St analysis provides more detail.

AngloGold Ashanti’s combination of high yield, wide margins and a planned US$2b buyback raises a simple question: is the market missing something in its current valuation gap, or is one crucial risk being underpriced in the 5 key rewards and 1 important warning sign

CNOOC (SEHK:883)

Overview: CNOOC is a major Hong Kong based oil and gas producer that explores, develops and produces crude oil and natural gas from offshore fields around China and a portfolio of assets across Asia, Africa, the Americas, Oceania and Europe, and then sells that production into global energy markets.

Market Cap: HK$1,112.2b

Income investors looking at CNOOC are often drawn to its dividend policy backed by low cost offshore production, resilient margins and rising volumes, as shown by Q1 2026 net production of 205.1 million BOE and net income of CNY 39,144 million. At the same time, the stock trades at a discount to several valuation measures. This raises the question of whether the market is overpricing long term transition and regulatory risks tied to its reliance on traditional oil and gas.

Rising volumes, low cost barrels and a discounted share price make CNOOC look like a story investors have not fully priced in yet, and the 2 key rewards and 1 important warning sign could reveal the twist that changes how you see it

Paychex (PAYX)

Overview: Paychex provides human capital management services that handle payroll, HR, benefits, retirement plans and insurance for small and mid sized businesses across the United States, Europe and India, helping clients stay compliant while outsourcing much of their people management workload.

Operations: Paychex generates about US$6.5b in revenue from Staffing & Outsourcing Services, reflecting its focus on recurring payroll, HR and related support services.

Market Cap: US$40.8b

Income investors looking at Paychex get a 4.16% dividend yield backed by earnings quality and long standing payroll and HR relationships, now being reshaped by the Paycor acquisition and new AI platforms like WISE and the Gen AI HR Copilot tool. One potential upside is that deeper automation, cost synergies that management is targeting in excess of US$80m and stronger client retention could support cash flows and margin improvement over time, even if revenue growth remains steady. The main considerations are that leverage levels, dividend coverage and the execution risk of integrating Paycor and monetising AI tools create pressure points that investors may want to weigh carefully alongside the Simply Wall St view on value and the analyst debate around where this stock could trade next.

Paychex’s push into AI and the Paycor integration could be reshaping its 4.16% income story in ways the headline yield does not show yet, and the analysis report for Paychex hints at the key pressure point investors often miss

The three income ideas covered here are just a starting point. The full Dividend Powerhouses screen on Simply Wall St surfaces 1,928 more companies in the Dividend Powerhouses (3%+ Yield) screener with equally compelling income stories and risk profiles. Use the platform to identify, filter and analyze the exact catalysts and narratives that matter to you so you can focus on the highest conviction dividend plays for your own portfolio.

Take Control of Your Investment Journey

If AngloGold Ashanti or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh breakout stories can move fast, and once momentum builds, entry points get away quickly. Scan these under the radar ideas before the crowd catches on and act now.

- Target resilient companies built to ride out volatility by scanning the curated 83 resilient stocks with low risk scores while price dislocations and sentiment gaps still offer room to position early.

- Hunt for overlooked miners and producers with leverage to metal prices through the hand picked 9 top silver producer stocks before renewed sector interest starts lifting valuations and shrinking your margin for error.

- Jump ahead of the energy transition narrative by reviewing the focused 90 nuclear energy infrastructure stocks while these infrastructure plays are still largely under the radar for now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com