Talen Energy (TLN) Could Be 22% Undervalued On PJM Capacity Auction Win

Why PJM Capacity Auction Results Matter For Talen Energy

Talen Energy (TLN) has become a talking point after reporting the results of PJM Interconnection’s latest capacity auction, which locked in 10,180 megawatts at about $325 per megawatt day for the 2028 to 2029 planning year.

This outcome points to an estimated $1.208b in future capacity revenues tied to Talen Energy’s generation fleet, giving investors a clearer view of contracted earnings and potential cash flow stability several years out.

See our latest analysis for Talen Energy.

The PJM auction update lands after a choppy period for Talen Energy’s stock, with the share price falling 9.4% over the past 30 days but still delivering a 39.5% total shareholder return over the past year and a very large 3 year total shareholder return. This suggests that recent short term weakness may be cooling, rather than reversing, the longer term trend.

If the PJM capacity win has you thinking about where the next grid or power opportunity might be, it could be worth scanning 35 power grid technology and infrastructure stocks

After a sharp run over three years and a recent pullback, Talen Energy now combines visible PJM capacity revenues with a stock that still sits well below analyst targets. Do current prices still skew the risk reward toward buyers?

Most Popular Narrative: 21.6% Undervalued

Against Talen Energy's last close of $368.29, the most followed narrative points to a higher fair value of $469.57, anchored on long term contracted power demand, higher assumed margins, and an 8.1% discount rate.

Major expansion and long term extension of carbon free nuclear power supply to AWS (1.9 GW through 2042) provide Talen with stable, inflation protected contracted revenue streams from a blue chip hyperscaler customer, de risking cash flows and enhancing margin visibility.

Read the complete narrative. Read the complete narrative.

Want to see how Talen Energy gets from current losses to the earnings profile implied here? The narrative leans on faster top line growth, a sharp margin reset, and a richer future earnings multiple typically reserved for higher growth sectors.

Result: Fair Value of $469.57 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the bullish Talen Energy narrative still leans on fossil heavy generation and debt financed growth, so policy shifts or weaker power pricing could quickly challenge those assumptions.

Find out about the key risks to this Talen Energy narrative.

Another View: Multiples Paint A Tougher Picture For Talen Energy

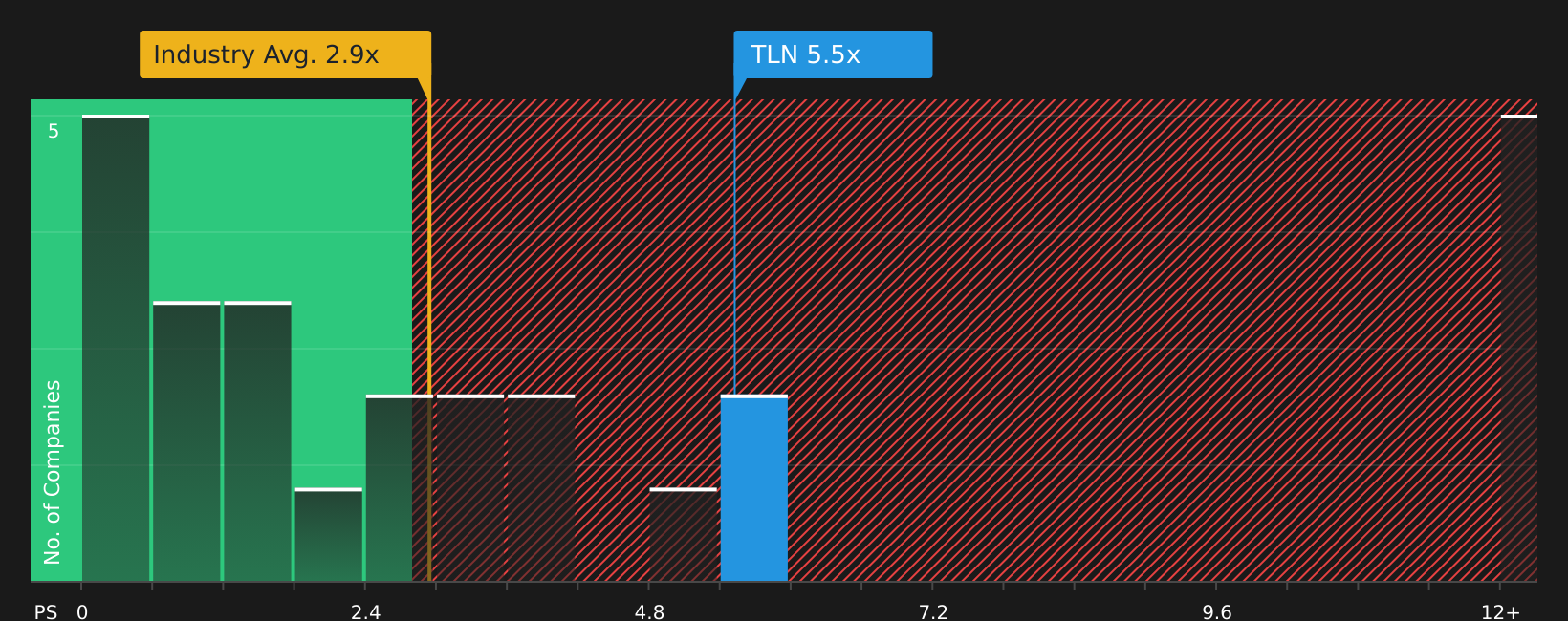

That 21.6% upside case for Talen Energy leans heavily on future earnings and cash flows, but today the stock trades on a P/S of 5.5x, compared with 2.9x for the North American renewable energy industry and a fair ratio estimate of 3.4x. In simple terms, the market is already paying a much richer revenue multiple than peers and the level our fair ratio points to. This raises the question of how much of the story is already in the price if execution slips at all.

To see how this revenue based view stacks up against other checks on Talen Energy, take a look at our valuation breakdown, then compare it with your own assumptions about growth, margins, and risk. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Talen Energy's story pulling in both optimism and concern, this is a moment to move quickly and check the balance of risks and rewards for yourself through the 3 key rewards and 2 important warning signs.

Looking For More Ideas Beyond Talen Energy?

If Talen Energy has sharpened your focus on where to put fresh capital next, do not stop here. Line up your next watchlist candidates before others move first.

- Target income resilience by scanning stocks that show up in our 8 dividend fortresses while still keeping an eye on balance sheet strength and payout history.

- Hunt for mispriced quality by checking companies highlighted in the 49 high quality undervalued stocks, where fundamentals and valuation screens already do the first round of filtering for you.

- Stay one step ahead by reviewing the screener containing 20 high quality undiscovered gems, so you are looking at strong businesses before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com