FuelCell Just Landed the Deal That Could Finally Turn It Profitable

FuelCell Energy (FCEL) had a big win earlier in the week. The stock jumped over 11% on Monday after the company announced a new collaboration with Siemens to develop scalable fuel cell power solutions. Under the partnership, Siemens will design and supply the electrical systems needed for large fuel cell installations. This should help FuelCell roll out commercial projects of 100 megawatts or more. The two companies also plan to work together across engineering, integration, and delivery, combining fuel cells with battery storage and microgrid controls.

For FuelCell, the timing of this deal matters a lot. The 100-plus MW project is expected to have a significant impact on the company’s profitability. As I covered earlier, the management said that the company’s EBITDA, which was negative $17.1 million last quarter, should turn positive once annual production reaches or exceeds 100 MW. So a deal that pushes project sizes into that range doesn’t just add revenue; it moves FuelCell closer to actually making money.

The Siemens deal also builds on strong recent momentum. Just weeks ago, FuelCell signed an agreement with Fit Energy to supply up to 380 MW of clean power for AI data centers. It has also been expanding its Torrington facility to reach as much as 500 MW of annual production capacity. With AI driving huge demand for reliable power, FuelCell is placing itself right in the middle of that opportunity.

About FCEL Stock

FuelCell Energy is a clean energy company that builds and operates fuel cell platforms for reliable, low-emission power generation. Its product portfolio includes fuel cell power systems, hydrogen production, carbon capture technology, and long-duration energy storage. Founded in 1969, the company is headquartered in Danbury, Connecticut, and is led by President and CEO Jason Few.

Year-to-date (YTD), FuelCell Energy’s stock has surged 128%, easily outperforming the iShares Global Clean Energy ETF’s (ICLN) 9% gain during the same period. The growth was helped by the growing data center pipeline, including the recent agreement with Fit Energy. FCEL stock has recently declined from its late-June high of $36 due to the company announcing a public offering of 10.7 million shares at a discount.

FuelCell Energy’s valuation looks more reasonable than it did just a couple of weeks ago. The company not yet being profitable means that the forward GAAP P/E is not meaningful, making the forward price-to-sales ratio a better measure. The P/S ratio of 9.83x sits around 20% above the company’s 5-year average. Not long ago, the stock was trading at nearly double its historical norms.

The earnings outlook further strengthens the valuation. The EPS growth estimate is over 50% each year from 2026 to 2028, which means the currently loss-making company could turn profitable in the next few years. The recent Siemens collaboration could help accelerate that path, with the management expecting projects of 100 MW or more to turn FuelCell’s EBITDA positive. The balance sheet should further improve investor confidence. FuelCell holds $373 million in cash against just $159 million in debt. For a company investing heavily, being net cash positive by $214 million is a genuinely strong position to be in. Overall, with the premium reducing significantly and the company potentially turning profitable, FuelCell’s valuation looks a lot better than it did during its earlier surge.

FuelCell's Loss Widens on a One-Time Charge

FuelCell Energy reported its second-quarter fiscal 2026 earnings on June 8, with results coming in below expectations. Revenue for the quarter reached $35.6 million, down 5% from Q2 fiscal 2025, missing Wall Street analysts' expectations of $40.5 million. CFO Michael Bishop tied the quarter’s revenue decline to mix and operational issues. Service revenue was lower as there were no module replacement projects during the quarter, while generation revenue was lower because the Groton project was being repaired. FuelCell posted earnings per share of -$1.45, which was below the analysts' estimates of -$0.44. Operating loss totaled $77.9 million, a 117% increase year-over-year (YoY). This loss was largely driven by a non-cash $42.6 million impairment charge related to the Groton project.

Going forward, management did not provide formal revenue or EPS guidance. However, the company plans to increase capacity at its Torrington facility from 350 megawatts to 500 megawatts of annual capacity. Moreover, in response to analyst questions, Bishop reaffirmed the company’s profitability framework and said that once the company achieves consistent production volumes at or above 100 megawatts on an annualized basis, it expects positive adjusted EBITDA.

What Analysts Are Saying About FCEL Stock

On June 29, B. Riley upgraded FCEL stock to a “Buy” rating from “Neutral.” The firm also revised its price target upwards to $32 from $13. The upward price target revision came after the company's Fit Energy data center deal. The agreement with Fit Energy boosts FuelCell’s confidence as the company can win business from major data center operators and convert them into long-term customers, the analyst told investors in a research note.

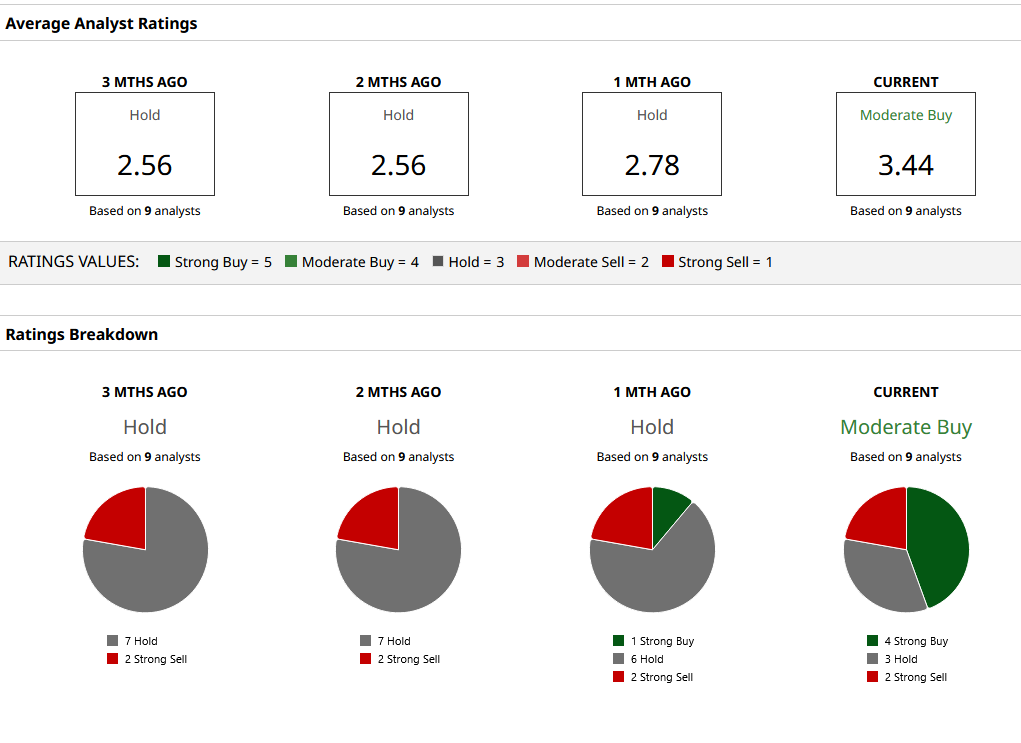

FuelCell is currently covered by nine Wall Street analysts and carries a consensus “Moderate Buy” rating. The mean price target of $25.29 implies a 14% potential upside from current levels. Out of the nine analysts covering the stock, four have a “Strong Buy” rating, three a “Hold,” and two “Strong Sell” ratings. Notably, FCEL has only recently picked up any “Strong Buy” ratings after months of just holds and sells.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.