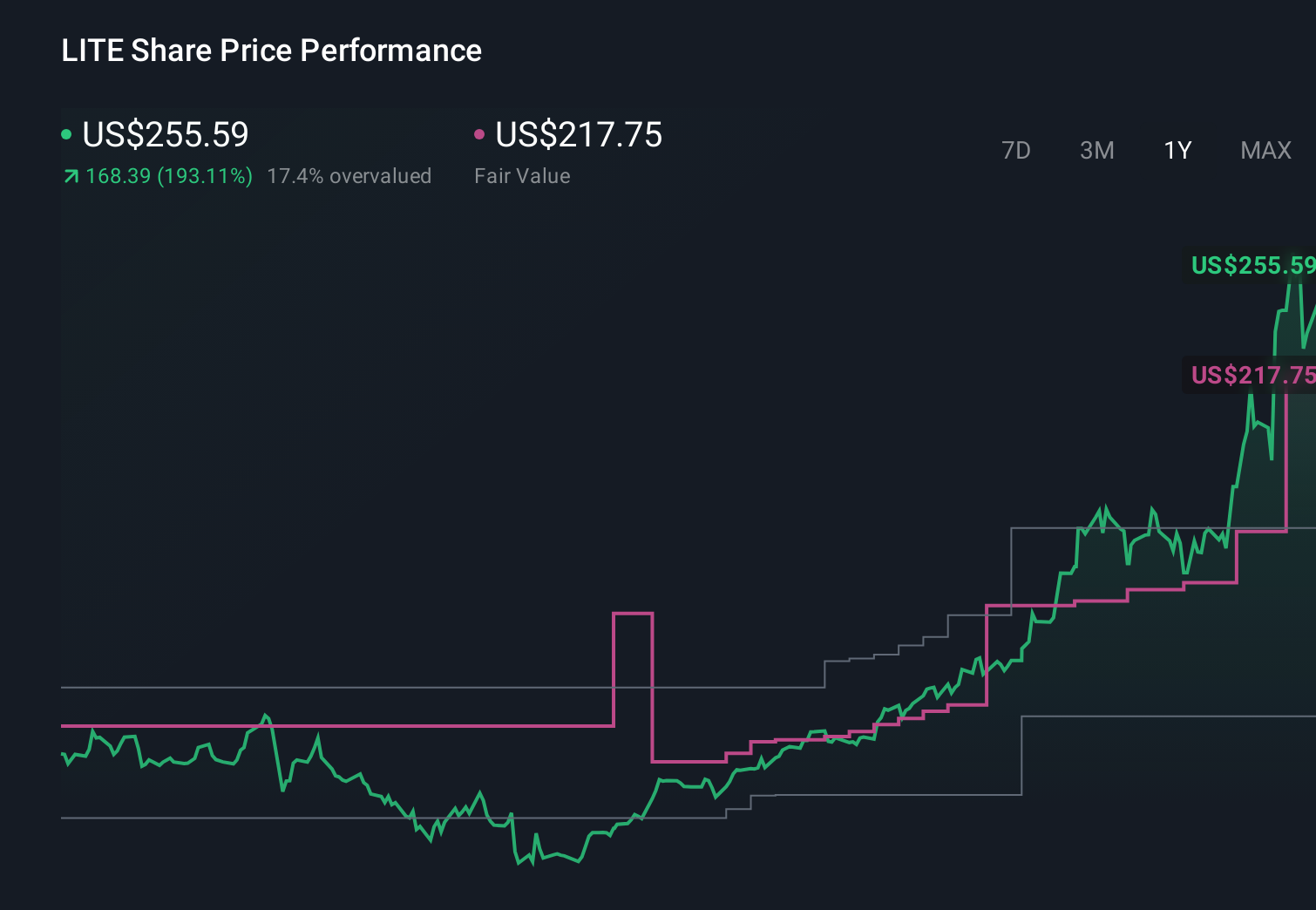

Lumentum (LITE) Is Down 10.1% After AI Optics-Fueled Zacks Upgrade Has The Bull Case Changed?

- Lumentum Holdings was recently upgraded by Zacks to a Rank #2 (Buy) after analysts raised earnings estimates amid rising demand for its optical components in AI-focused data centers, supported by fresh capital from an NVIDIA-led investment.

- This combination of stronger earnings expectations and AI data center exposure highlights how shifts in infrastructure spending can quickly reshape analyst views on Lumentum’s fundamentals.

- We’ll now examine how this Zacks upgrade, driven by higher earnings estimates tied to AI optics demand, affects Lumentum’s existing investment narrative.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Lumentum Holdings Investment Narrative Recap

To own Lumentum, you need to believe AI data center demand can offset cyclical telecom weakness and justify its premium valuation and customer concentration. The Zacks Rank #2 upgrade, tied to higher earnings estimates from AI optics demand and NVIDIA-linked capital, reinforces that near term AI infrastructure spending remains the key catalyst, while execution on capacity ramps and managing reliance on a few hyperscalers still looks like the central risk. The upgrade itself does not remove that concentration risk.

The most relevant recent development here is Lumentum’s strong Q3 2026 results, with revenue of US$808.4 million and a swing to US$144.2 million in net income. That profitability turnaround, alongside guidance for Q4 revenue of US$960 million to US$1,010 million, provides some fundamental backdrop for the more optimistic earnings revisions driving the Zacks upgrade and puts extra focus on whether AI driven cloud optics strength can persist as telecom and other end markets remain choppy.

Yet against the AI enthusiasm, investors should also be aware that heavy dependence on a handful of hyperscale customers means that any pullback in orders or move to in house optics could...

Read the full narrative on Lumentum Holdings (it's free!)

Lumentum Holdings' narrative projects $11.8 billion revenue and $4.2 billion earnings by 2029. This requires 67.8% yearly revenue growth and about a $3.8 billion earnings increase from $439.0 million today.

Uncover how Lumentum Holdings' forecasts yield a $1111 fair value, a 57% upside to its current price.

Exploring Other Perspectives

Some analysts were already very optimistic before this news, projecting revenue to grow about 82.6 percent annually and earnings to reach roughly US$5.3 billion, so you should expect a wide range of views on whether today’s AI demand and customer concentration risk justify that much upside or call for more caution.

Explore 8 other fair value estimates on Lumentum Holdings - why the stock might be worth just $802.35!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Lumentum Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Lumentum Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lumentum Holdings' overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com