How International Paper’s Carrollton Plant Closure and Footprint Shift Will Impact International Paper (IP) Investors

- International Paper recently announced it will permanently close its Carrollton South packaging facility in Carrollton, Texas by the end of the third quarter of 2026 as part of efforts to better align its manufacturing footprint with customer demand in North America.

- The move underscores how International Paper is reshaping its plant network, reallocating resources, and offering severance, continued benefits, outplacement support, and potential redeployment for nearly all 64 affected employees.

- Next, we will examine how this footprint rationalization, including the Carrollton South closure, could influence International Paper's broader turnaround investment narrative.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

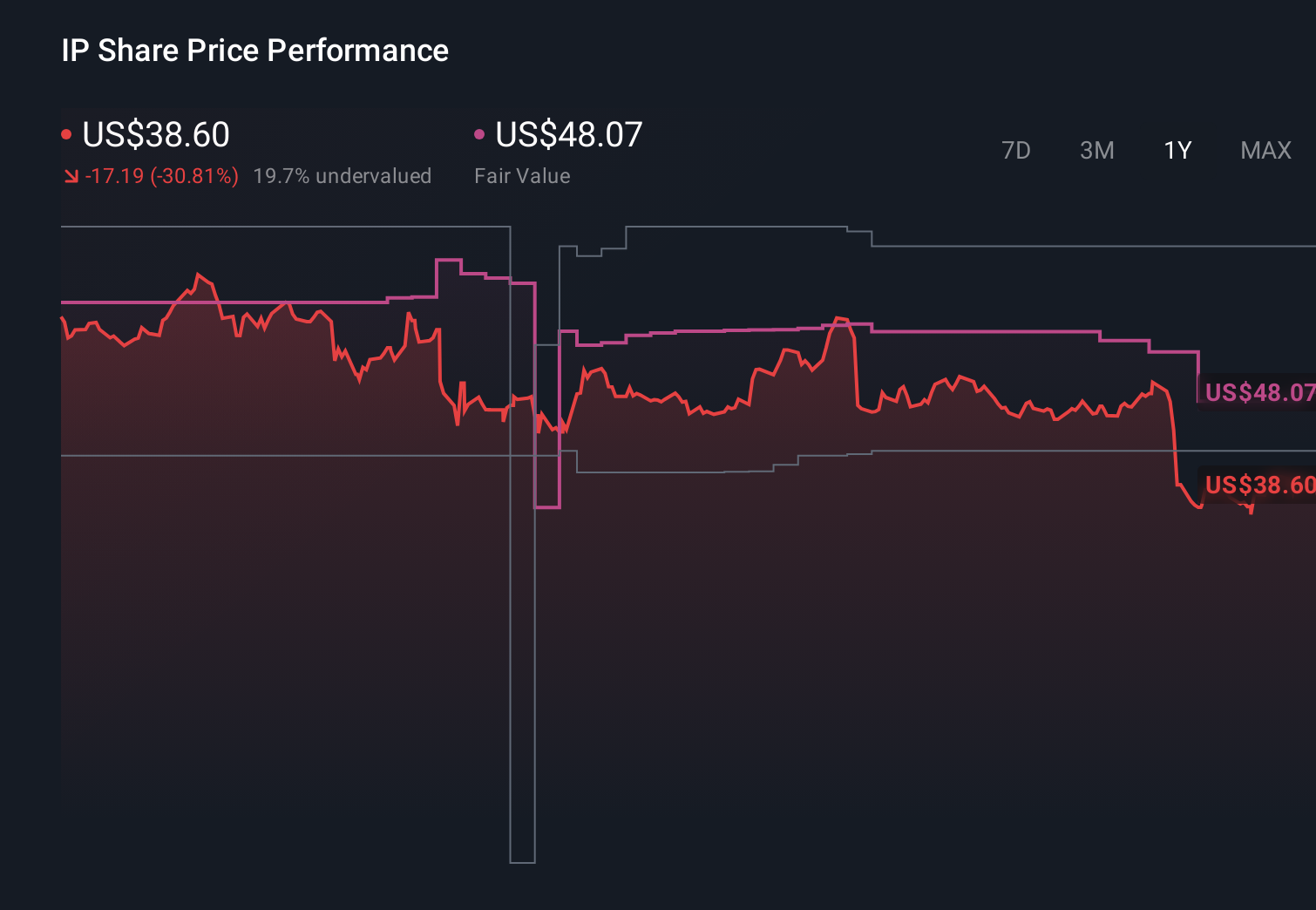

International Paper Investment Narrative Recap

To own International Paper, you need to believe its multi‑year turnaround in packaging, cost efficiency, and mill reliability can steadily translate into healthier earnings despite a slow‑growth backdrop. The Carrollton South closure looks incremental within a broader footprint reset and does not obviously change the key near‑term catalyst: consistent execution on asset optimization to support profitability. The biggest risk remains operational and integration complexity around mill reliability, plant closures, and the DS Smith combination.

In that context, the recent decision to maintain the quarterly common dividend at US$0.4625 per share is worth watching. It sits alongside plant closures like Carrollton and other network changes, and together they highlight the tension between funding reliability and optimization projects and supporting shareholder returns. How the company balances these priorities could influence how investors assess the credibility of its cost‑out and earnings improvement story over the next few years.

Yet beneath all of this, investors should be aware of the execution risk around complex mill reliability fixes and footprint changes that could...

Read the full narrative on International Paper (it's free!)

International Paper's narrative projects $26.2 billion revenue and $1.7 billion earnings by 2029.

Uncover how International Paper's forecasts yield a $39.36 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the lowest‑priced analysts were already cautious, assuming only about 2 percent annual revenue growth and earnings near US$1.8 billion by 2029, so this closure and related footprint shifts may prompt you to rethink whether their more pessimistic view on operational risk and capital intensity better fits your own expectations or whether the consensus story still feels more compelling.

Explore 3 other fair value estimates on International Paper - why the stock might be worth just $39.36!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your International Paper research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free International Paper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate International Paper's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com