Hudbay Minerals (TSX:HBM) Could Be 35% Undervalued As Earnings Near

Hudbay Minerals (TSX:HBM) has come under the spotlight after its share price fell 22.68% over the past month to close the latest session at CA$29.24, as investors look ahead to its July 29 earnings report.

See our latest analysis for Hudbay Minerals.

Over the past month, Hudbay Minerals’ 1 month share price return of down 28.21% and 1 day move of down 5.25% contrast with a 1 year total shareholder return of 117.34%. This signals fading short term momentum against a much stronger multi year backdrop.

If this shift in sentiment around Hudbay Minerals has you reassessing the sector, it could be a useful moment to scan for other copper focused opportunities using the 8 top copper producer stocks.

Bulls see Hudbay Minerals’ recent pullback as a reset after strong multi year gains, while bears see it as a warning sign. Which case do the current valuation signals support?

Most Popular Narrative: 34.7% Undervalued

Hudbay Minerals' most followed valuation narrative pegs fair value at CA$44.77, well above the recent CA$29.24 close, and anchors that view in copper growth projects and balance sheet strength.

Hudbay's upcoming Copper World project, now significantly derisked and funded through a joint venture with Mitsubishi, positions the company for a more than 50% increase in annual copper output. This is expected to enable direct exposure to intensifying demand from electrification, renewable energy, and U.S. critical mineral supply chain initiatives, with the likely result being higher future revenues and potential premium pricing.

Want to see what sits behind that copper growth story? The narrative leans heavily on rising revenue, robust margins and a richer earnings multiple than the wider metals sector.

Result: Fair Value of CA$44.77 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Hudbay Minerals’ story can change quickly if Copper World or other large projects face cost overruns or permitting delays, or if unrest disrupts Peru operations again.

Find out about the key risks to this Hudbay Minerals narrative.

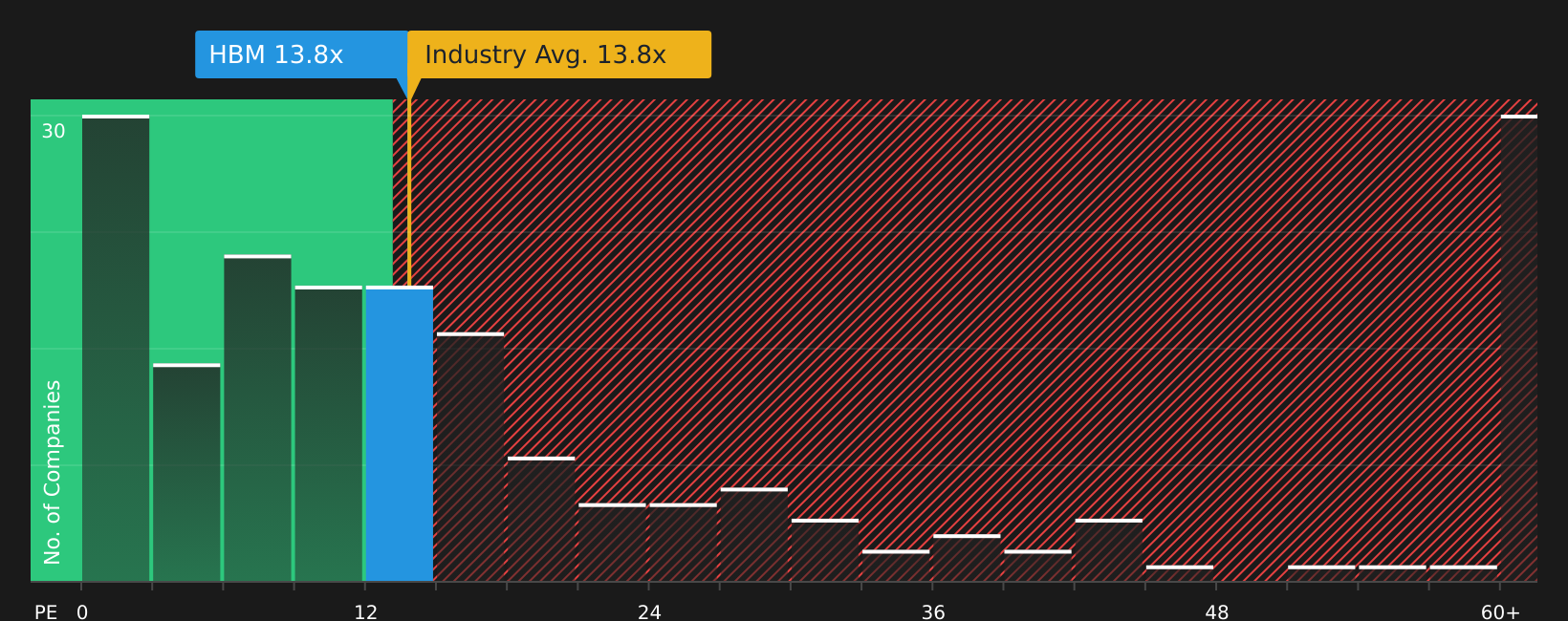

Another View: Hudbay Minerals Through a P/E Lens

Hudbay Minerals looks cheap on headline fair value estimates, with CA$29.24 trading about 50.4% below one modelled fair value. Yet its current 14x P/E is slightly above a 13.1x fair ratio and roughly in line with the Canadian metals and mining group at 14x. Is that a bargain or simply a full price for higher project risk?

To see how this pricing gap could close, and what that might mean for valuation risk or opportunity, it helps to look at what the numbers say about this price using our fair ratio based view, then compare it with peers through the See what the numbers say about this price — find out in our valuation breakdown..

Next Steps

With such a split between short term weakness and longer term optimism around Hudbay Minerals, it makes sense to move quickly and weigh the trade off yourself using the 4 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Hudbay Minerals?

Do not stop your research with Hudbay Minerals. Broaden your watchlist with other stock ideas filtered by quality, value and resilience using the Simply Wall St Screener.

- Target powerful upside potential by scanning for companies trading below what their fundamentals suggest using the 5 high quality undervalued stocks.

- Prioritise resilience by checking out stocks that pair financial strength with dependable fundamentals through the solid balance sheet and fundamentals stocks screener (11 results).

- Get ahead of the crowd by reviewing a screener containing 10 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com