World Gold Council: Gold ETFs in the Chinese market still achieved significant inflows in the first half of the year

The Zhitong Finance App learned that data from the World Gold Council showed that despite the June outflow, gold ETFs in the Chinese market achieved significant inflows in the first half of the year, driving a slight increase in total asset management (AUM) to 243 billion yuan, and the total holdings increased by 29 tons to 277 tons.

Upstream physical gold demand rebounded month-on-month in June, but the total volume in the first half of the year was still significantly below the ten-year average. The People's Bank of China increased its gold holdings by 15 tons in June, making it the largest monthly gold purchase since October 2023. China's official gold reserves increased by 40 tons in the first half of the year.

Entering the second half of the year, with gold prices stabilizing, the scale of gold ETF outflows from the Chinese market has narrowed significantly, but weak Au9999 trading volume and sluggish domestic and foreign gold price premiums indicate that demand for physical gold was still weak in early July.

Gold prices weakened in June, erasing gains in the first half of the year

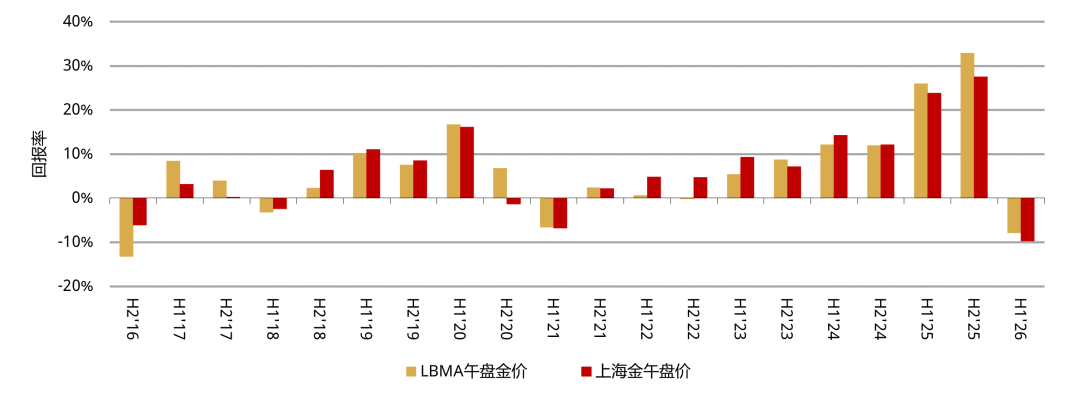

The London Midday Gold Price (LBMA) in US dollars and the Shanghai Midday Benchmark Gold Price (SHAUPM) in RMB both fell 11% in June, mainly due to rising opportunity costs and cooling trend momentum:

The statement made by the new Federal Reserve Chairman Kevin Walsh at the June monetary policy meeting was interpreted by the market as a hawkish signal, boosting the real yield on US bonds and the US dollar exchange rate, causing investors to reduce their holdings in gold ETFs, and their options positions also became skewed.

First half

The weakening of gold prices in June reversed previous increases, and gold ended with a decline in the first half of the year

As detailed in the “2026 Global Gold Market Mid-Year Outlook”, gold prices experienced a roller coaster in the first half of the year. Various risks, changes in investor positions, and rising opportunity costs were the main driving factors behind this round of intense fluctuations.

International gold prices in US dollars fell 8%, while RMB gold prices fell 10%. The strengthening of RMB against the US dollar amplified the weak performance of RMB gold prices, which experienced the first semi-annual decline since 2021.

Semi-annual returns on Shanghai SHAUPM midday gold prices and London LBMA midday gold prices

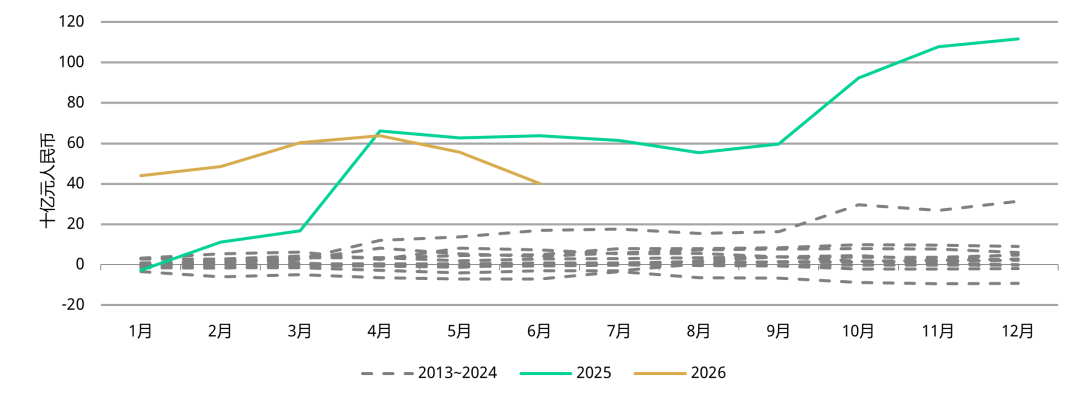

In June, the outflow of gold ETFs from the Chinese market was 15 billion yuan. As the weakest monthly performance on record, the total asset management scale of gold ETFs fell 16% to 243 billion yuan, reducing total holdings by 17 tons to 277 tons, the lowest level since December 2025.

Main influencing factors:

Weakening gold prices have weakened domestic investors' interest in allocating gold;

Investors are enthusiastic about the stock market, and the number of new accounts opened continued to increase dramatically in June, distracting the market from gold.

First half

Gold ETF performance in the Chinese market was weak in June, causing the year-to-date inflow to narrow to 40 billion yuan. It is still the second-strongest first-half performance on record

The inflow volume of gold ETFs in the Chinese market in the first half of the year reached the second highest level in history

Cumulative monthly demand for gold ETFs in the Chinese market

The total demand for gold ETFs in the Chinese market reached 29 tons, and the total scale of asset management increased slightly by 1%

Main influencing factors:

Demand for gold ETFs remains strong against the backdrop of heightened geopolitical and economic uncertainty;

The People's Bank of China continues to announce gold purchases and continues to support market sentiment;

Institutional investors' participation in gold ETFs in the Chinese market has also increased, providing further support for demand for such products.

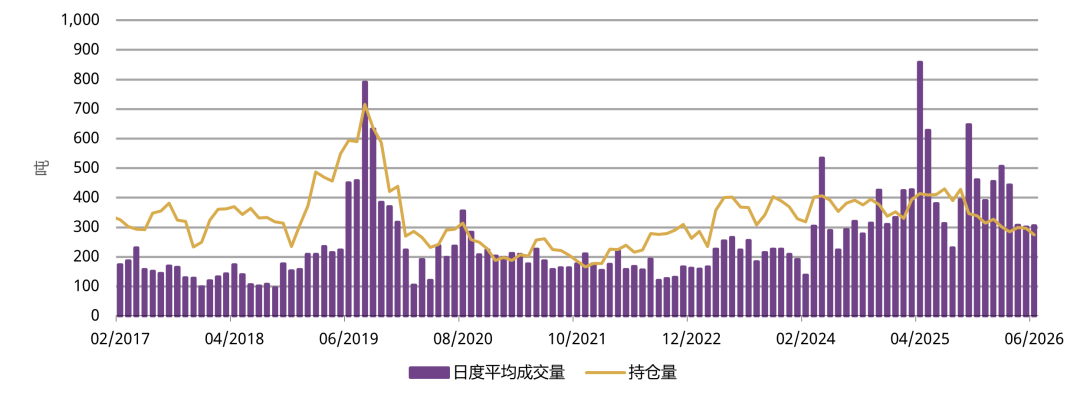

In June, the average daily trading volume of gold futures on the Shanghai Futures Exchange reached 305 tons, up 4 tons from the previous month. Although lower than the 2025 average of 457 tons, it is still significantly higher than the five-year average of 265 tons.

Gold futures holdings on the Shanghai Futures Exchange reached 274 tons, down 8% month-on-month and 13% lower than the level at the end of 2025.

Gold futures trading volume remains high on the Shanghai Futures Exchange

However, the volume of holdings has declined

The average daily trading volume of gold futures on the Shanghai Futures Exchange and the volume of holdings at the end of the period

The average daily trading volume of gold futures on the Shanghai Futures Exchange reached 386 tons in the first half of the year, which is the main supporting factor for maintaining a high trading volume:

Fluctuations in gold prices have intensified;

Market participants hedge against increased demand.

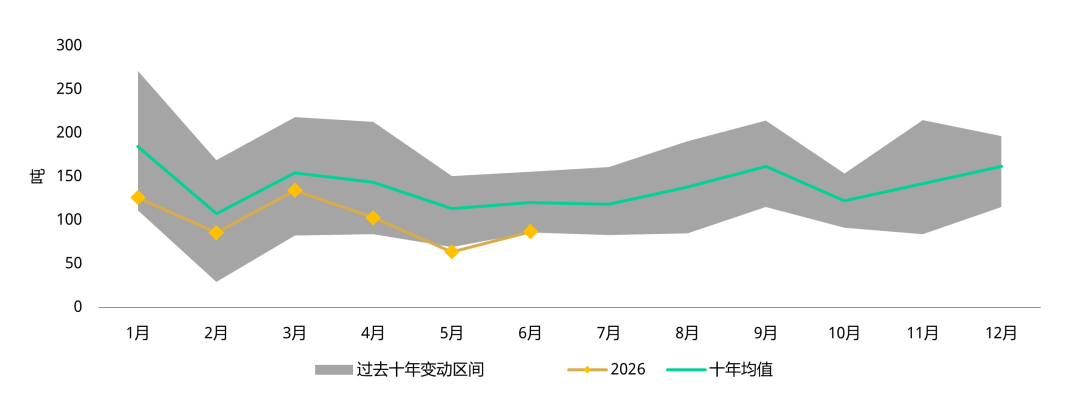

Upstream physical gold demand rebounded in the first half of the year

Gold shipments from the Shanghai Gold Exchange (SGE) in June were 87 tons, up 36% from the previous month, mainly driven by the following factors:

Falling gold prices drive opportunity replenishment in all parts of the supply chain;

Individual investors buy on dips, and demand for gold bars and coins remains steady;

The previous month's base was extremely low — May recorded its weakest performance in 16 years.

Against the backdrop of continued weakness in jewellery demand, upstream physical gold demand in June was still close to the low level of the past decade.

Upstream physical gold demand rebounded in June, but is still below the ten-year average

Monthly gold shipments and ten-year monthly average from the Shanghai Gold Exchange

Market participants extracted 598 tons of gold from the Shanghai Gold Exchange in the first half of the year, down 12% from the same period last year and 27% lower than the 10-year average.

Although demand for physical gold investment remains strong, jewellery consumption continues to weaken, and manufacturers and retailers are cautious about replenishing stocks, thereby dragging down overall upstream physical gold demand.

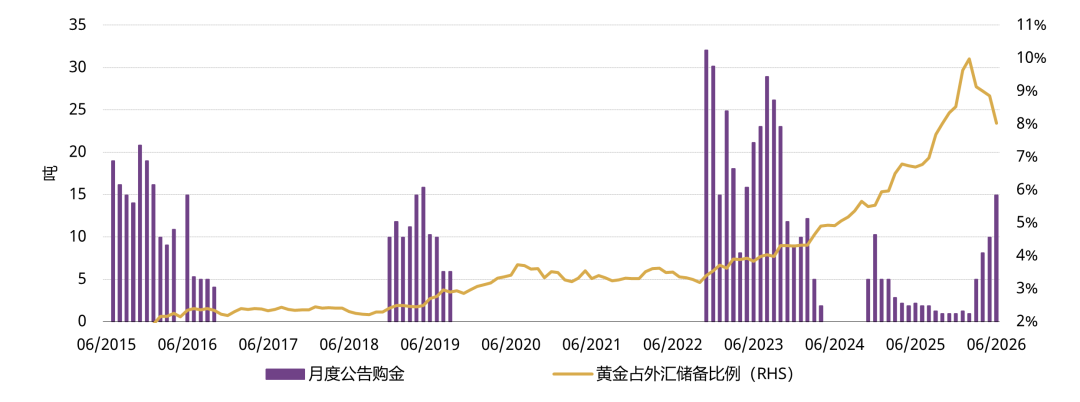

The People's Bank of China continues its gold buying trend

In June, the official gold reserves of the People's Bank of China increased by 15 tons, making it the largest monthly purchase since October 2023, achieving 20 consecutive months of increase, making the longest continuous growth cycle in history, driving official gold reserves to 2,346 tons, accounting for 8% of foreign exchange reserve assets.

First half

Despite fluctuations in gold prices, the People's Bank of China continued to buy gold in the first half of the year. Official gold reserves increased by 40 tons. Over the past 20 months, the total amount of gold purchased reached 82 tons.

During this period, global geopolitical tension intensified, trade controls tightened, and financial market fluctuations heated up, further highlighting the strategic advantages of gold as a safe, stable, and credit-free asset. As shown in the “2026 Global Central Bank Gold Reserve Survey”, these properties of gold are the factors that central banks value the most.

China's official gold reserves have been growing continuously for a long time

The People's Bank of China announced the scale of gold purchases and the share of gold in foreign exchange reserves

Gold imports fell slightly in May

In May, the Chinese market imported 151 tons of gold, down 6 tons from the previous month.

Gold imports fell slightly in May

Net import volume of gold under customs code 7108