Has Coupang (NYSE:CPNG) Fallen Far Enough To Still Be A Bargain?

Coupang stock has fallen about 56% over the past five years, yet its current valuation checks lean cheap. This sets up a clear question for investors about whether the market is being too harsh or the risks are simply catching up with the share price.

- The share price decline of roughly 56% over five years suggests long term holders have faced heavy losses and the market has repeatedly reassessed what Coupang is worth.

- On the one hand, Coupang's push into new offerings and markets can support higher revenue expectations. On the other hand, issues such as the recent data breach highlight that operational and regulatory risks may still weigh on how investors price the stock.

- Coupang currently screens as undervalued on most of Simply Wall St's checks, with the company looking cheap on 5 of 6 valuation measures, according to the value score.

The issue now is whether Coupang's discounted market price is signalling a genuine mispricing or simply reflects the business risks investors are being asked to accept.

Find out why Coupang's -45.9% return over the last year is lagging behind its peers.

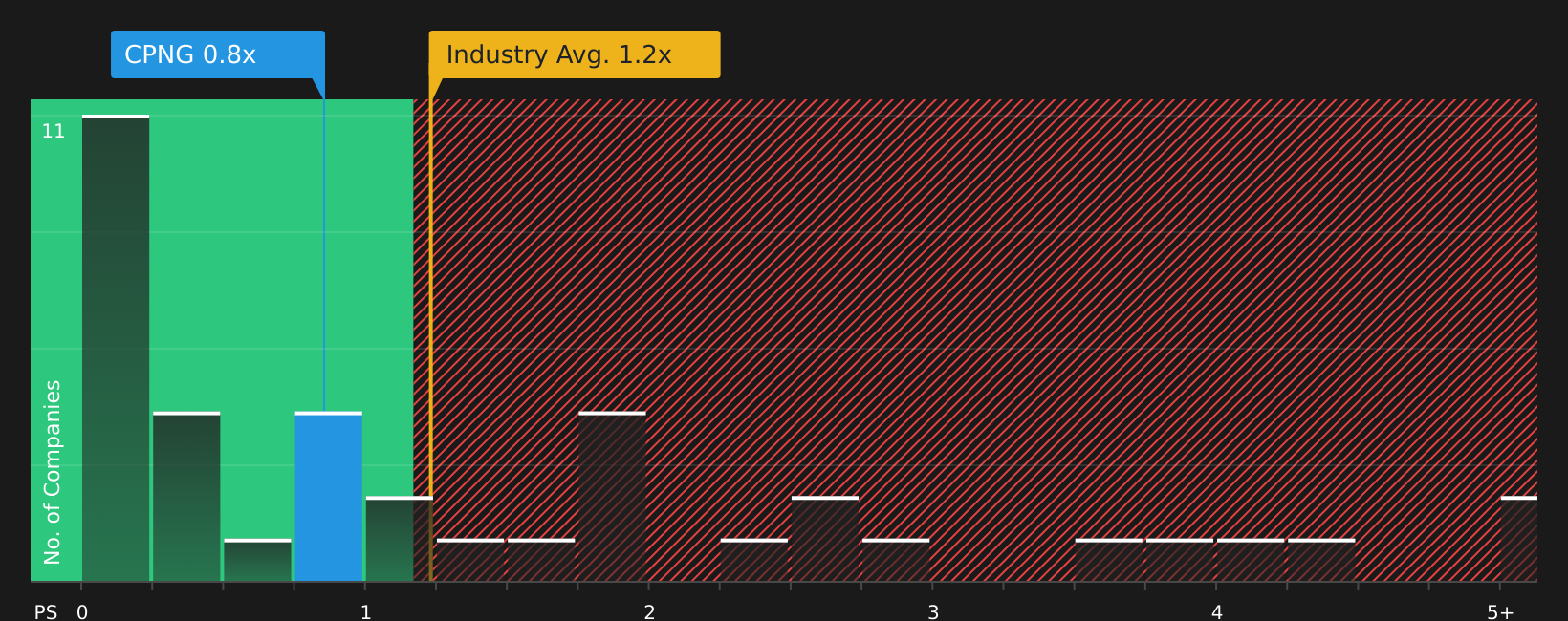

Is Coupang a Bargain on Sales?

P/S is a useful way to look at Coupang because the company is still more defined by its revenue base than by consistent earnings.

Coupang currently trades on a P/S of about 0.9x, which is below both the Multiline Retail industry average of roughly 1.2x and the peer group average of about 2.5x. The Simply Wall St fair P/S ratio for Coupang is 1.3x, which reflects what might be expected given its size, margins, sector and risk profile. On that basis, the current multiple sits at a discount to what this framework suggests as a more tailored benchmark.

Despite the recent data breach and the legal focus on control and regulation in Korea, Coupang's P/S still prices the stock below both industry norms and the modelled fair ratio. For investors who put more weight on revenue than short term profit metrics, this gap on the sales multiple stands out.

Overall, Coupang appears undervalued on its P/S ratio relative to both industry averages and the fair multiple implied by this model.

See what the numbers say about this price — find out in our valuation breakdown.

The Coupang Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Coupang's valuation puzzle leaves off by spelling out which combinations of future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price on the Community page. Instead of focusing on a single multiple or model output, each narrative sets out the assumptions behind its view of fair value so you can compare them with Coupang's actual results as they are reported.

Coupang investors on the community page are split between a recovery story and a tougher long haul where costs and regulation bite harder.

Bull case: 36% undervalued

"Ongoing investments in automation, AI, and logistics technology are already driving major improvements in operational efficiency and gross margins, and management sees significant further upside as these technologies are scaled…"

Read the full Bull Case to see why Coupang could be undervalued

Bear case: roughly fairly valued

"Coupang's long-term profitability is threatened by rising labor costs and the demographic challenges in South Korea, such as a shrinking workforce, which will significantly elevate operating expenses and strain last-mile logistics, leading to compressed net margins regardless of near-term gains in automation or process improvements…"

Read the full Bear Case to see why Coupang could be overvalued

Do you think there's more to the story for Coupang? Head over to our Community to see what others are saying!

The Bottom Line

For Coupang, the current set up is that the stock screens as undervalued on market multiples, yet the gap likely exists because investors are weighing execution, regulatory and operational risks raised by recent events. The key question is whether the discount reflects an overly cautious market or fairly prices those risks. What matters most from here is whether Coupang can defend and improve margins without running into heavier regulatory or cost pressure. That margin path, more than any single valuation metric, is what will determine whether today’s discount becomes an opportunity or proves to be a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com