Is Evotec (XTRA:EVT) Cheap After Cutting Its 2026 Revenue Guidance?

Evotec (XTRA:EVT) cut its full year 2026 revenue guidance to a range of €570 million to €610 million after issuing preliminary first half figures, with investors now watching the upcoming Q2 earnings call for clarity.

See our latest analysis for Evotec.

The lowered 2026 guidance appears to have weighed heavily on sentiment, with Evotec’s share price down 30.62% over the past week and its 1 year total shareholder return falling 53.29%. This extends already weak multi year performance and suggests momentum has been fading rather than building.

If this guidance reset has you reassessing your watchlist, it could be a good moment to look at other biotech and pharma related ideas through our healthcare focused screener, including 126 healthcare AI stocks.

After Evotec’s sharp reset and steep share price fall, the key question is whether investors are now looking at meaningful upside from a depressed base or if most of the easy recovery is already behind the stock. This is where valuation comes in.

Most Popular Narrative: 49.3% Undervalued

On the most followed narrative, Evotec’s fair value of €6.83 sits well above the last close at €3.46, which puts a spotlight on what is driving that gap.

Evotec's expansion and deepening of large pharma partnerships, as evidenced by the rapid growth of its Just, Evotec Biologics (JEB) business with three major pharma clients and a move to an asset lighter, technology focused licensing model, are expected to drive recurring, higher margin revenue streams, supporting revenue growth and boosting net margins.

Want to see why this valuation leans so far above today’s price? The narrative leans heavily on earnings turning positive, margins rebuilding and a richer profit multiple a few years out.

Result: Fair Value of €6.83 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upside narrative for Evotec still leans heavily on a small group of large partners and on early stage biotech funding not weakening further.

Find out about the key risks to this Evotec narrative.

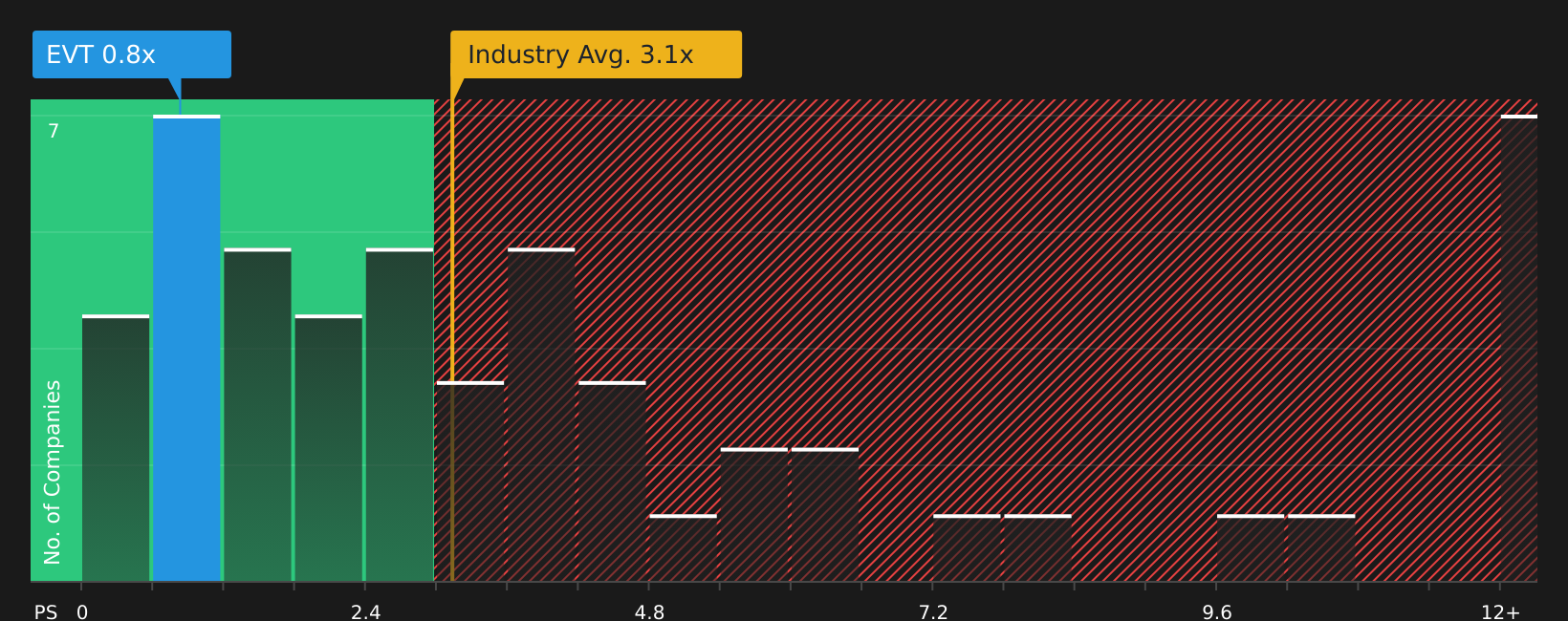

Another View: What Multiples Say About Evotec

There is a different signal coming from simple sales-based pricing. Evotec trades on a P/S ratio of 0.8x, which sits below both peers at 4.8x and the wider European Life Sciences industry at 3.1x, yet above a fair ratio of 0.6x implied by regression analysis.

In plain terms, the stock looks inexpensive compared to its sector but not especially inexpensive versus where the fair ratio suggests the market could move to. This leaves open the question of whether investors are being too cautious or still paying up for long-term potential.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages on Evotec's outlook and valuation can be hard to reconcile, so move quickly, review the full data set and weigh up the trade off between 2 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Evotec?

If Evotec has you rethinking your portfolio, do not stop at a single stock, use this moment to refresh your watchlist with other focused ideas.

- Target potential mispricing by scanning companies that look out of favor but still financially robust through the 228 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks offering higher yields and resilient payouts via the 470 dividend fortresses.

- Reduce portfolio stress by concentrating on companies with healthier finances and fewer red flags using the 289 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com