Atlas Copco (OM:ATCO A) Posts Record Orders, Is The Stock Still Undervalued?

Atlas Copco (OM:ATCO A) stock is in focus after the company reported record order intake, higher second quarter sales of SEK 44,974 million and net income of SEK 7,060 million, alongside five completed acquisitions.

See our latest analysis for Atlas Copco.

The earnings release and record order intake have been met with a positive reaction, with Atlas Copco’s 1 day share price return of 4.44% lifting the stock to SEK195.15 and adding to a year to date share price return of 16.33%. The 1 year total shareholder return of 22.91% and 5 year total shareholder return of 50.30% point to momentum that has built over time rather than just this quarter’s news.

If strong industrial demand has your attention, it could be a good moment to broaden your watchlist and explore 32 robotics and automation stocks

After the latest jump, Atlas Copco now trades only a single digit percentage below the average analyst target, while one intrinsic estimate sits slightly above the market. So where does fair value really sit in that spread?

Most Popular Narrative: 2.1% Undervalued

Atlas Copco's most followed narrative points to a fair value of about SEK199.33, slightly above the SEK195.15 last close. This puts a tight spotlight on the earnings and margin story underpinning that number.

The expanding, high-margin service and aftermarket business continues to grow robustly across business areas, increasing recurring revenue streams and helping to stabilize and lift group operating margins even amid volatility in equipment orders.

The central question is simple. Can Atlas Copco turn a growing installed base and service mix into the earnings profile this narrative expects? The answer rests on how revenue, margins and valuation multiples interplay over the next few years. That tension is exactly what this fair value framework lays out.

Result: Fair Value of SEK199.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Atlas Copco narrative can quickly be challenged if currency headwinds persist or if large compressor and Gas & Process orders remain weaker for longer.

Find out about the key risks to this Atlas Copco narrative.

Another View on Atlas Copco’s Valuation

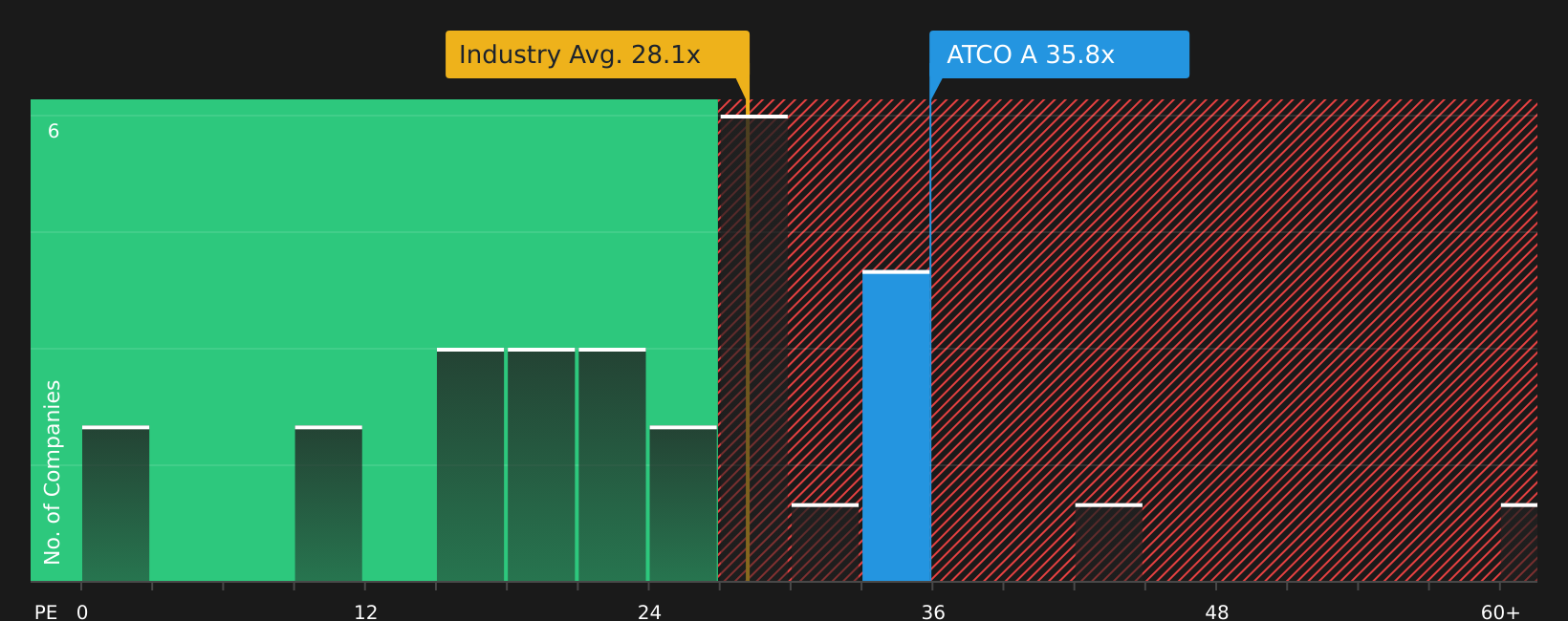

While the fair value narrative suggests Atlas Copco is about 2.1% undervalued at SEK199.33, the current P/E of 36.5x is higher than both Swedish Machinery peers at 28.3x and the stock’s own fair ratio of 36.7x. That leaves only a narrow cushion, so how much valuation risk are you really comfortable with?

See what the numbers say about this price in our valuation breakdown See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mixed signals around Atlas Copco’s valuation, do you feel the optimism is justified, or is the cushion too thin for comfort? To move quickly from headline numbers to your own verdict, review the full reward profile in our 1 key reward

Looking for more ideas beyond Atlas Copco?

If Atlas Copco has sharpened your focus, do not stop there. Give yourself options by lining up a few more high quality candidates on your radar.

- Spot potential bargains early by scanning 230 high quality undervalued stocks that pair stronger fundamentals with prices that may not fully reflect them yet.

- Strengthen the core of your portfolio by reviewing solid balance sheet and fundamentals stocks screener (417 results) that prioritize healthier debt profiles and steadier financial footing.

- Get ahead of the crowd by checking the screener containing 507 high quality undiscovered gems before they appear on every investor’s watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com