Nasdaq (NDAQ) Could Be 11% Undervalued As Earnings Expectations Build

Nasdaq (NDAQ) is drawing fresh attention as investors position ahead of its July 23 earnings report, with expectations for higher quarterly earnings and revenue, while mixed sentiment creates uncertainty around a potential beat or miss.

See our latest analysis for Nasdaq.

At a share price of $94.25, Nasdaq has seen a 7.69% 7 day share price return and a 6.37% 90 day share price return. The 1 year total shareholder return of 6.10% sits against a softer year to date share price return that is down 2.49%, suggesting recent momentum has picked up ahead of the earnings event.

If this earnings setup has you looking beyond a single stock, it could be a good moment to widen your watchlist through the Simply Wall St screener for 18 top founder-led companies

Nasdaq is now trading at $94.25, with recent gains sitting alongside a spread between its market price, analyst targets and some intrinsic value estimates. So where might fair value really sit before earnings reset expectations?

Most Popular Narrative: 11.5% Undervalued

Nasdaq is trading at $94.25 compared with a widely followed fair value narrative of $106.53, which sets up a clear valuation gap for investors to unpack.

The expansion of Verafin's AI-driven solutions is anticipated to enhance the platform's value, facilitating upselling opportunities, attracting new clients, and increasing engagement. This should support growth in ARR and revenue, contributing to profitability through increased customer retention and usage.

Want to see what sits behind that valuation gap, and why Verafin, cloud partnerships and long term earnings assumptions carry so much weight in the model?

Result: Fair Value of $106.53 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this Nasdaq narrative still faces pressure from potential delays in larger FinTech deals and tougher competition across exchanges that could restrain revenue and margin progress.

Find out about the key risks to this Nasdaq narrative.

Another View: Nasdaq And The Cash Flow Debate

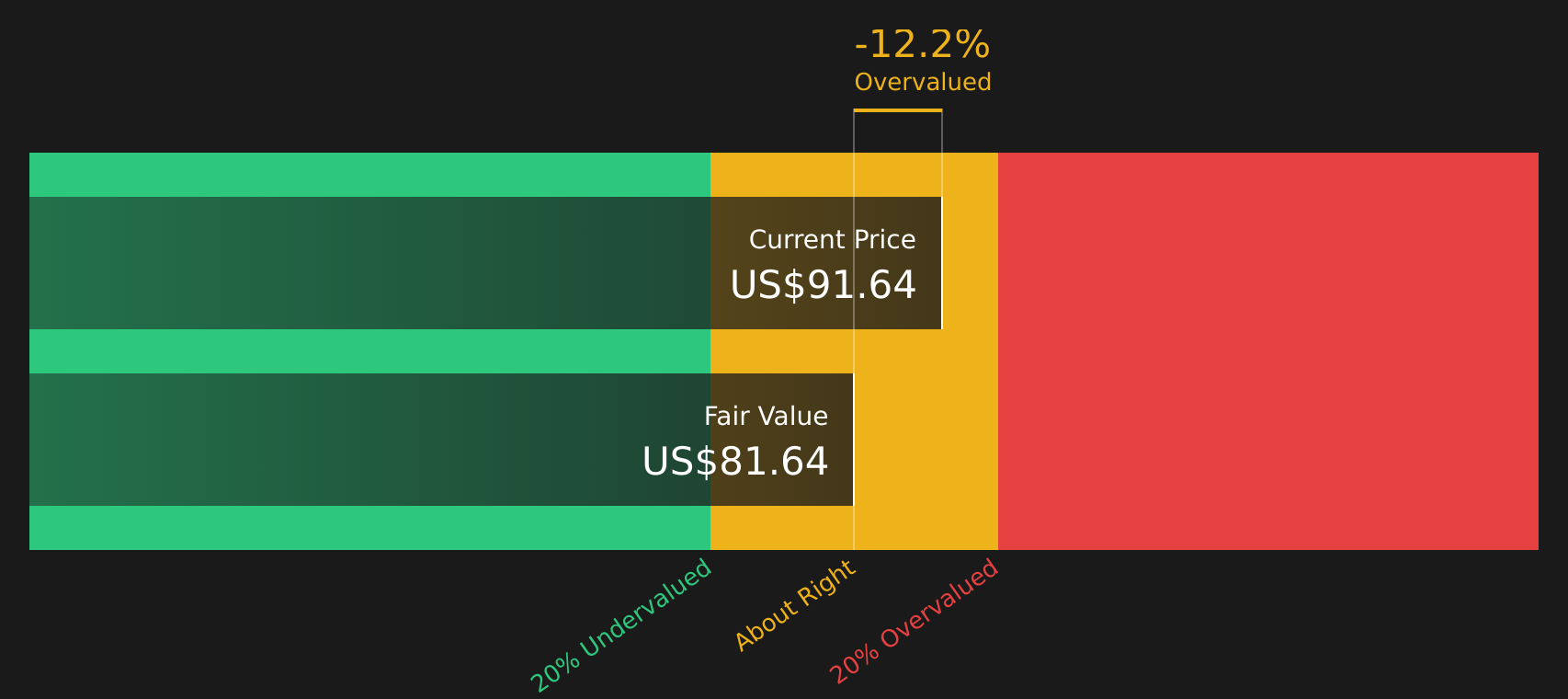

While the current Nasdaq narrative leans on a fair value of $106.53 based on future earnings and P/E assumptions, the SWS DCF model paints a more cautious picture, with an estimate of $81.41 per share that frames the stock as overvalued on a cash flow basis.

This clash between an earnings based fair value that suggests upside and a cash flow model that points to downside raises a simple question for you as an investor: which set of assumptions feels closer to how you think Nasdaq will actually generate cash over time?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nasdaq for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between upside potential and cash flow caution for Nasdaq, it is worth checking the full picture yourself and acting before the narrative moves. To see the mix of concerns and bright spots in one place, start with these 3 key rewards and 2 important warning signs

Looking for more stock ideas beyond Nasdaq?

Do not stop with Nasdaq alone. New opportunities often sit in corners of the market you have not checked yet, and the right filters can surface them fast.

- Target steady compounders by zeroing in on businesses with robust finances and dependable metrics through the solid balance sheet and fundamentals stocks screener (48 results).

- Hunt for value by focusing on companies that combine quality fundamentals with appealing pricing using the 49 high quality undervalued stocks.

- Prioritise resilience by concentrating on stocks that score well on risk, stability, and balance sheet strength via the 82 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com