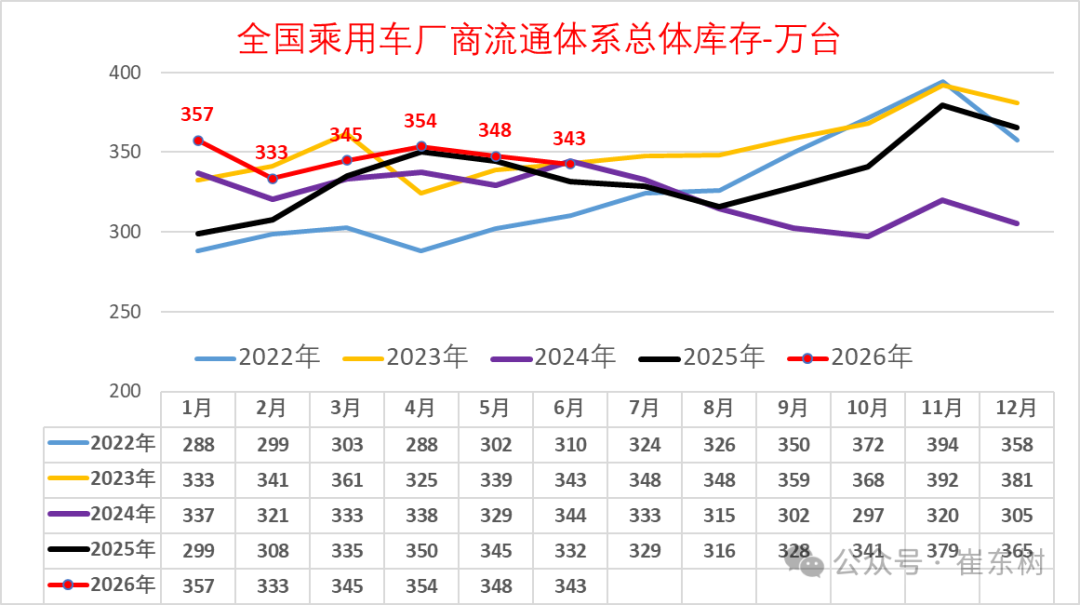

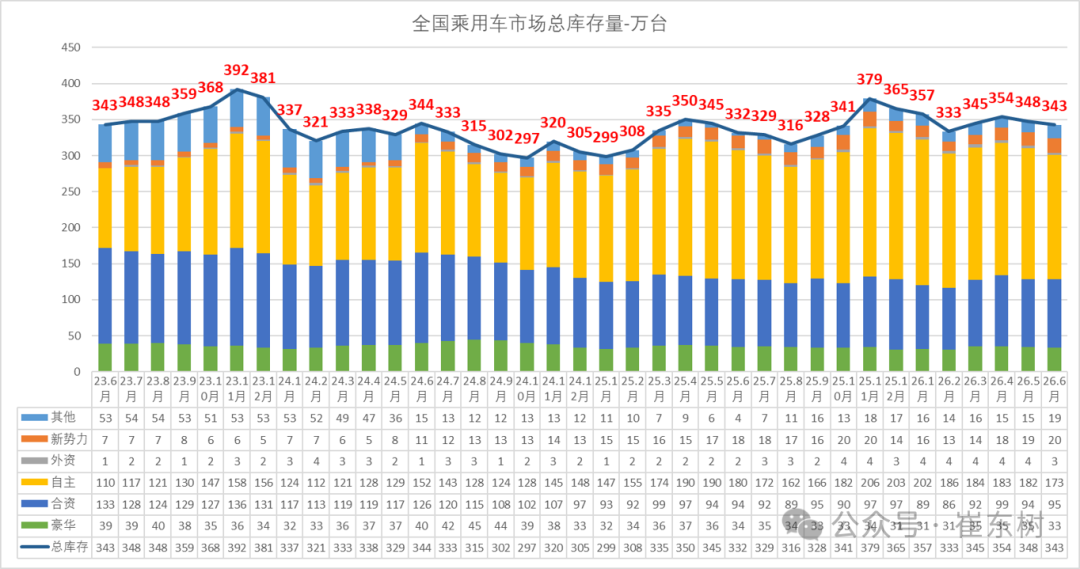

Cui Dongshu: At the end of June, the national passenger car industry inventory was 3.43 million vehicles, down 50,000 from the previous month, up 110,000 vehicles from June 2025

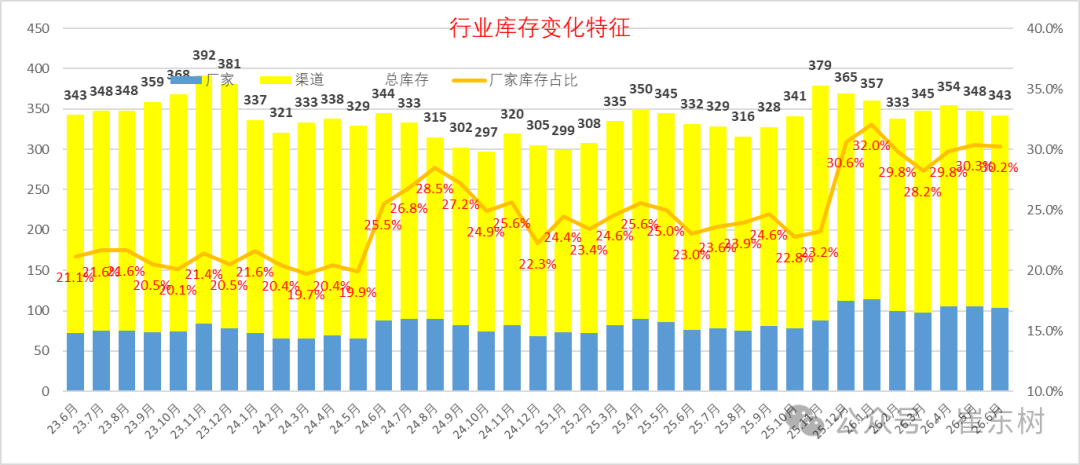

The Zhitong Finance App learned that Cui Dongshu, Secretary General of the Passenger Transport Association, published an article stating that at the end of June 2026, the national passenger car industry had 3.43 million units in stock, down 50,000 units from the previous month, and an increase of 110,000 units from June 2025, forming a trend where inventories continued to flatten. Among them, manufacturers' inventories accounted for 30.2%, which is relatively high.

The Passenger Link Branch predicts that the team's optimism for June 2026 is 31%, and the satisfaction rate after June at the beginning of July is 37%. Expectations are low but satisfaction is poor, mainly because the impact of high oil prices is too big. The team's optimism about the July market fell to 19%. This is a historically low forecast index for judging recent market optimism.

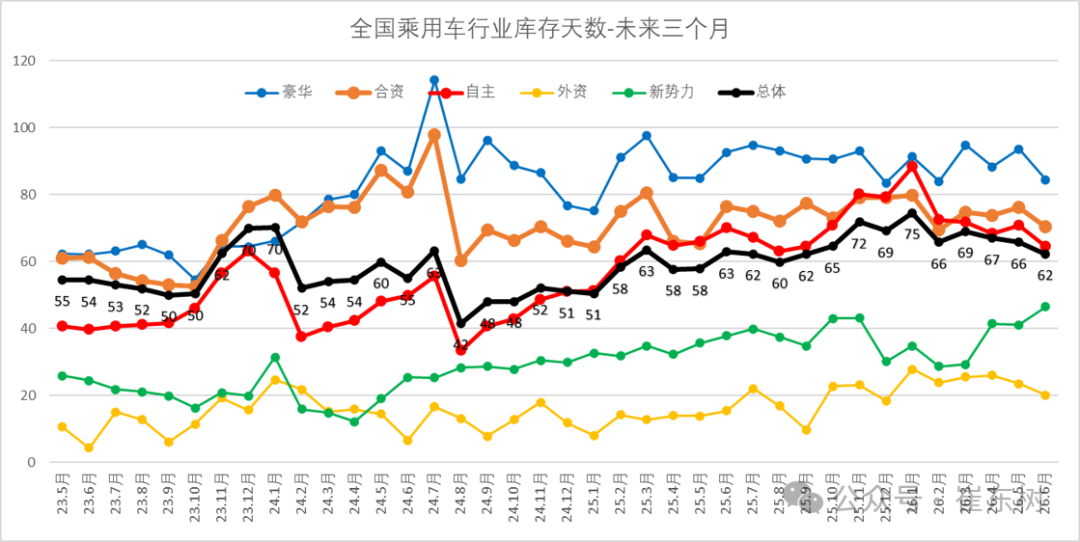

Inventory supports future days based on future N+3 monthly retail forecasts. Future retail changes on a rolling basis, so it is not a fixed monthly data, and the number of inventory days will also change according to forecast adjustments. Based on inventory at the end of June 2026 and a comprehensive estimate of domestic retail sales for the next 3 months, the number of future sales days is 62 days. Compared with 54 days in June 2023, 55 days in June 2024, and 63 days in June 2025, the overall inventory pressure in June this year is relatively high.

The total inventory of companies that only produce new energy vehicles remained at 790,000 units in June 2026, the same as the previous month, an increase of 10,000 units from the peak inventory in November 2025, but a decrease of 10,000 units from 800,000 units in June 2025. Recently, the manufacturer and channel inventories of new energy dealers faced lower than expected retail sales in the market, and the overall pressure on industry inventories was high.

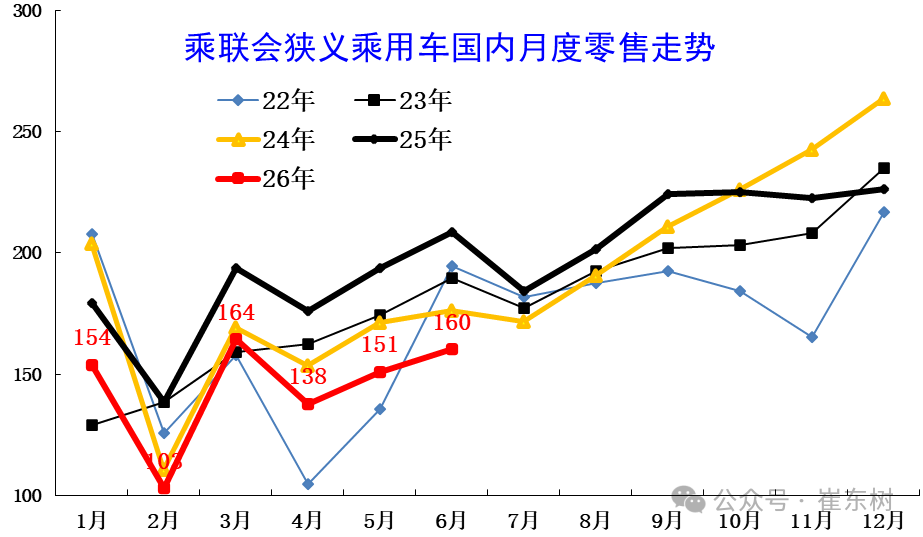

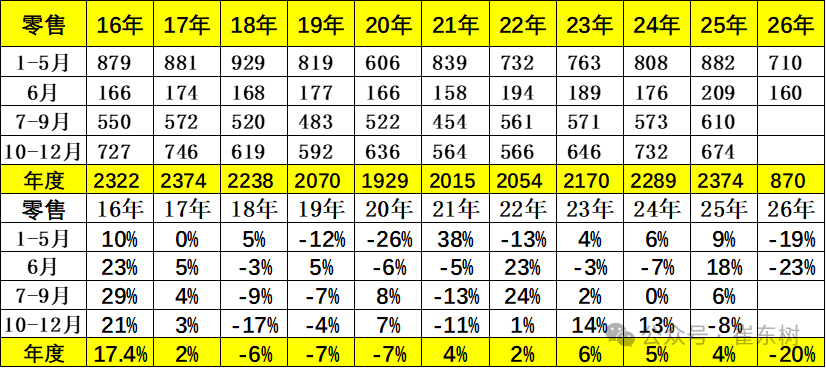

1. Passenger car retail trends in the narrow sense of the word in recent years

In June, the national passenger car market retailed 1.6 million vehicles. The year-on-year growth performance was weak, leaving the normal growth line. The reasons for the negative growth in June were diverse. The first was the impact of high oil prices, and the second was the strong regulation of the new trade-in policy and shrinking subsidies. Coupled with the sharp impact of upstream price increases, the underlying reason was low consumption capacity and willingness.

In June, the national passenger car market retailed 1.602 million vehicles, a year-on-year decrease of 23% and a year-on-month increase of 6%; since this year, 8.7 million vehicles have been retailed, a year-on-year decrease of 20%. In June 2026, the domestic passenger car market showed an operational trend of “total pressure, month-on-month strengthening, and extreme structural differentiation”.

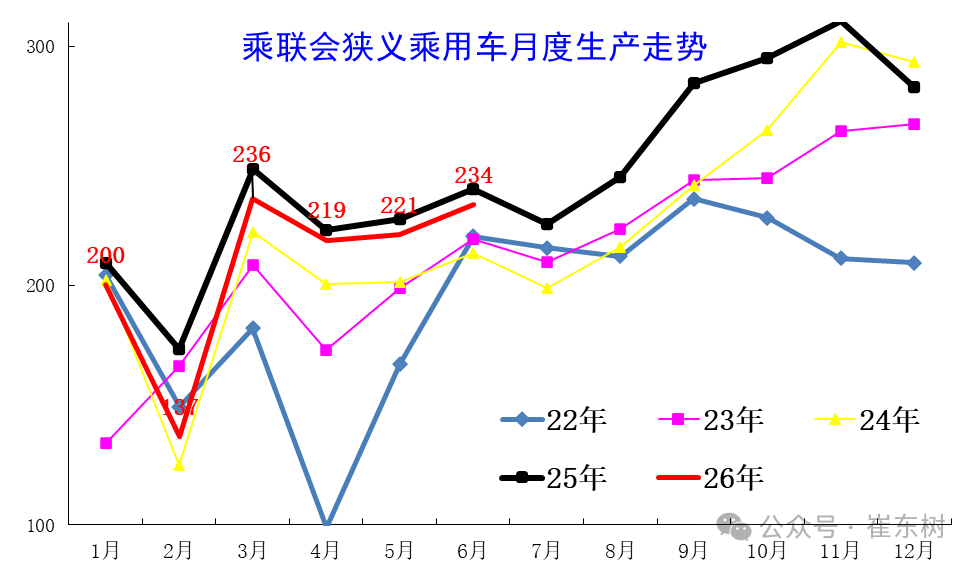

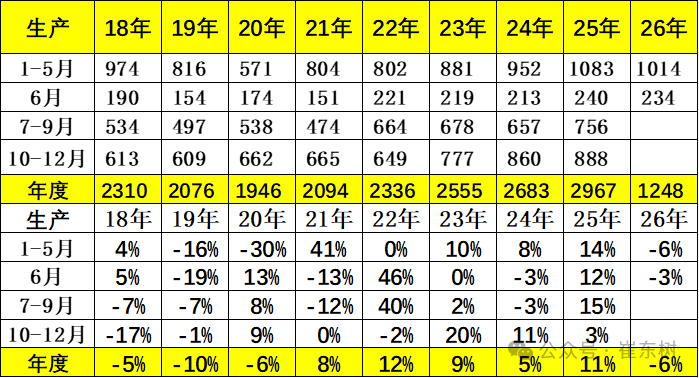

2. Passenger car production trends in the narrow sense of the word in recent years

Passenger car production declined sharply in the first quarter. The new national standard was launched in July, and market demand continued to be weak in June, leading to strong active production cuts in June. Passenger car exports boosted greatly in June.

Passenger car production in June was 2.338 million units, down 2.7% year on year and up 5.6% month on month.

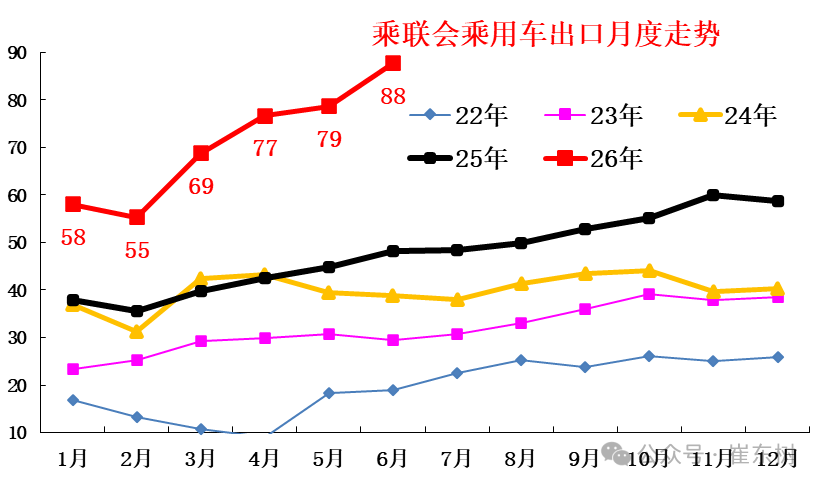

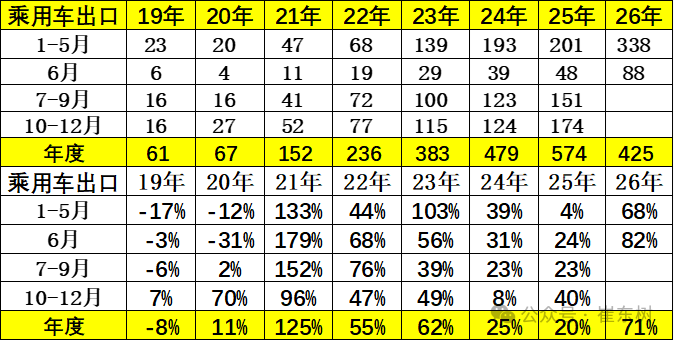

3. Recent passenger car export trends in the narrow sense

Passenger car exports (including complete vehicles and CKD) were 880,000 units in June. Few exploded for 3 consecutive months, and surged month-on-month in June, which is in sharp contrast to the 2025 trend.

Passenger car exports (including complete vehicles and CKD) were 887,000 units in June, up 82.3% year on year and 11.5% month on month, accounting for 37% of passenger car manufacturers' sales volume (36% last month, 19% in the same period in 2025).

4. National passenger car industry inventory tracking

At the end of June 2026, the national passenger car industry inventories were 3.43 million units, down 50,000 units from the previous month and 110,000 units higher than in June 2025, forming a trend where inventories continued to flatten. The launch of the trade-in policy in 2025 brought about overall optimism among manufacturers. The sales volume driven by trade-in was high, and manufacturers were relatively cautious in production, resulting in continuous inventory removal from May to August. Since the market has seriously fallen short of expectations since October of last year, inventory hit a new high of nearly two years in November, but production was drastically reduced thereafter. The added value of inventory in June was still high compared to inventory during the same period, and the market was relatively sluggish.

5. National passenger car industry inventory tracking

Since 2023, the overall inventory of the passenger car industry has remained relatively stable. It fell back to around 2.97 million units in October 2024, rebounded to 3.79 million units in November 2025, then declined. Inventory in June 2026 fell to 3.43 million units, of which manufacturer inventory accounted for 30.2%.

Due to good market expectations in the early stages, manufacturers are enthusiastic about production, and overall industry inventory pressure is relatively uncontrollable. Currently, the share of manufacturers' inventory is high, the market is seriously sluggish, and manufacturers are cutting production, but the pressure on sales to absorb inventory in the next few months will still not be small.

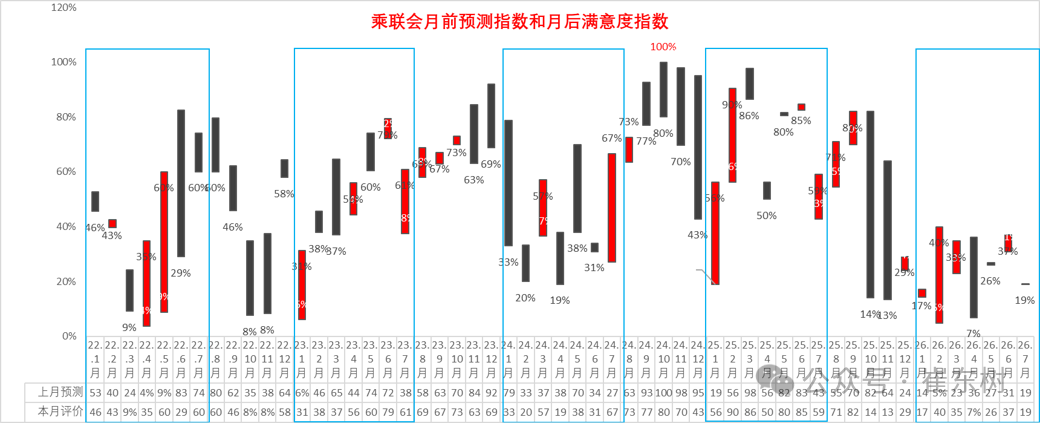

6. National Passenger Vehicle Market Forecast Index and Satisfaction Index

Monthly market performance is evaluated according to how the PMI index is set and evaluation results. According to the forecast summary estimates of the manufacturer's insiders, the prediction team of the Chengdu Branch has been very optimistic and gradually pessimistic since the beginning of 2025. The forecasting team was very optimistic about the market forecast from January to September 2025, and satisfaction plummeted in October. The Passenger Link Branch predicts that the team's optimism for June 2026 is 31%, and the satisfaction rate after June at the beginning of July is 37%. Expectations are low but satisfaction is poor, mainly because the impact of high oil prices is too big.

The team's optimism about the July market fell to 19%. This is a historically low forecast index for judging recent market optimism. From the current inventory level of 3.43 million vehicles and expectations to judging market growth in the next few months, the pressure on the industry to absorb inventory is still strong. In view of the current situation where sales continue to fall short of expectations, car companies need to promptly track changes in the policy environment and market, carefully set the pace of production and sales, carefully increase inventory according to the dealer inventory structure, and clean up historical inventory in a timely manner.

7. Overall inventory characteristics of the national passenger car market

As the share of new energy vehicles increased, fuel vehicle sales declined, and the corresponding inventory pressure gradually decreased. Looking at the inventory cycle, from 3.25 million units in April 2023, then rebounded to 3.92 million units in November 2023, then declined to a low inventory level of 2.97 million units in October 2024.

2025 to 2026 is still an inventory increase cycle, and the pressure on the industry is gradually increasing. Recently, the car market has declined significantly. Due to the severe contraction of new energy vehicles, the pressure on inventories has not been effectively relieved.

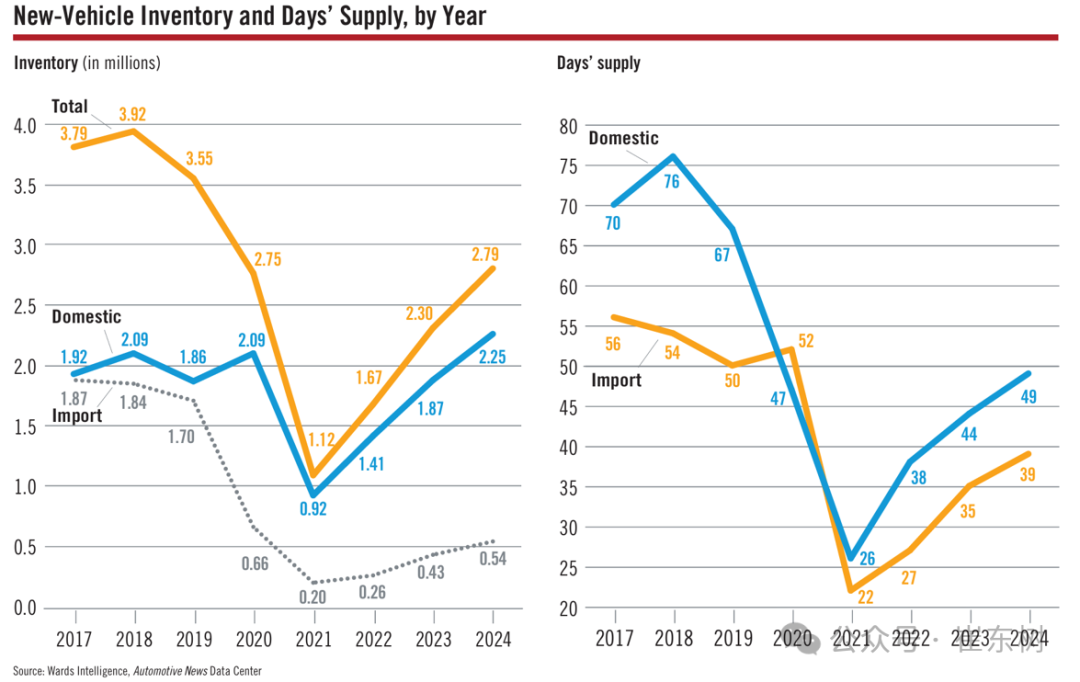

8. US passenger car industry inventory comparison

The US inventory is currently in 40-50 days, and the overall inventory pressure is low. This is also a reference target for the Chinese car market.

9. The number of inventory days in the national passenger car market declined slightly

As the market recovery arrived as scheduled in 2025, the production trend was strong. The characteristics of inventory removal in the early stages changed, and the reverse internal volume brought about inventory control in the industry, and inventory growth was relatively moderate. In the fourth quarter of 2025, although the expiration of the tax exemption policy was promoted, the trend actually fell short of expectations. The peak number of days in industry inventory rebounded to 77 days, and production declined sharply thereafter. Therefore, based on inventory at the end of June 2026 and the current inventory based on a comprehensive estimate of domestic retail sales volume for the next 3 months, the number of future sales days is 62 days. Compared with 54 days in June 2023, 55 days in June 2024, and 63 days in June 2025, the overall inventory pressure in June this year is relatively high.

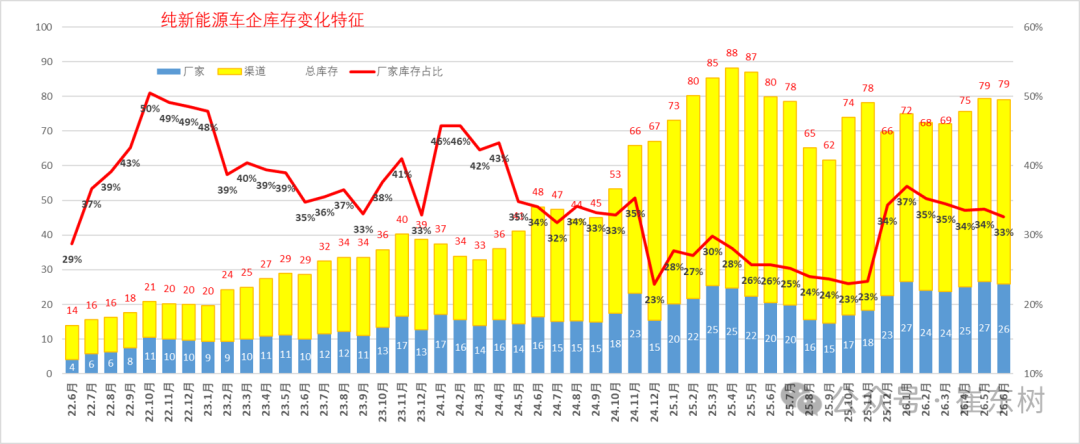

10. The national inventory of new energy passenger vehicles continues to rise

Judging from the analysis of inventory change characteristics of companies that only produce new energy vehicles, the inventory of 200,000 units was in early 2023, and then entered a period of rapid inventory growth. In April 2025, the inventory of companies that only produce new energy vehicles reached 880,000 units. This is a recent peak. With the push of internal scrutiny, industry inventories fell to 620,000 units in September 2025, and the total inventory of companies that only produced new energy vehicles remained at 790,000 units in June 2026, the same as the previous month, an increase of 10,000 units from the peak inventory in November 2025, but a decrease of 10,000 units from 800,000 units in June 2025. Recently, the manufacturer and channel inventories of new energy dealers faced lower than expected retail sales in the market, and the overall pressure on industry inventories was high.