3 UK Stocks Estimated To Be Trading Up To 49.1% Below Intrinsic Value

The United Kingdom's stock market has recently faced challenges, with the FTSE 100 index experiencing declines following weak trade data from China, highlighting concerns over global economic recovery. As investors navigate these uncertain conditions, identifying stocks that are trading below their intrinsic value can offer potential opportunities for long-term growth.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Rosebank Industries (LSE:ROSE) | £3.02 | £5.43 | 44.3% |

| RHI Magnesita (LSE:RHIM) | £30.15 | £59.25 | 49.1% |

| Playtech (LSE:PTEC) | £3.744 | £7.41 | 49.5% |

| Morgan Advanced Materials (LSE:MGAM) | £2.19 | £3.95 | 44.5% |

| Living REIT (LSE:LIVE) | £0.794 | £1.57 | 49.3% |

| Kistos Holdings (AIM:KIST) | £2.775 | £5.35 | 48.1% |

| Eurocell (LSE:ECEL) | £1.14 | £2.19 | 48% |

| Entain (LSE:ENT) | £5.684 | £10.95 | 48.1% |

| AstraZeneca (LSE:AZN) | £126.28 | £226.61 | 44.3% |

| Accsys Technologies (AIM:AXS) | £0.741 | £1.43 | 48.3% |

Let's explore several standout options from the results in the screener.

Fresnillo (LSE:FRES)

Overview: Fresnillo plc is a company engaged in the mining, development, and production of non-ferrous minerals in Mexico, with a market cap of £18.09 billion.

Operations: The company's revenue is primarily derived from its operations at Herradura ($1.24 billion), Saucito ($1.01 billion), Juanicipio ($892.47 million), Fresnillo ($699.78 million), SAN Julian ($524.36 million), Cienega ($230.10 million), and Noche Buena ($51.79 million).

Estimated Discount To Fair Value: 13.8%

Fresnillo is trading at £24.55, below its estimated future cash flow value of £28.48, suggesting it may be undervalued based on cash flows. Despite a volatile share price and unstable dividend history, the company shows potential with forecasted earnings growth of 13.09% annually and revenue growth outpacing the UK market at 9% per year. Recent production reports indicate a decline in silver and gold output but stable lead and zinc production levels.

- Insights from our recent growth report point to a promising forecast for Fresnillo's business outlook.

- Navigate through the intricacies of Fresnillo with our comprehensive financial health report here.

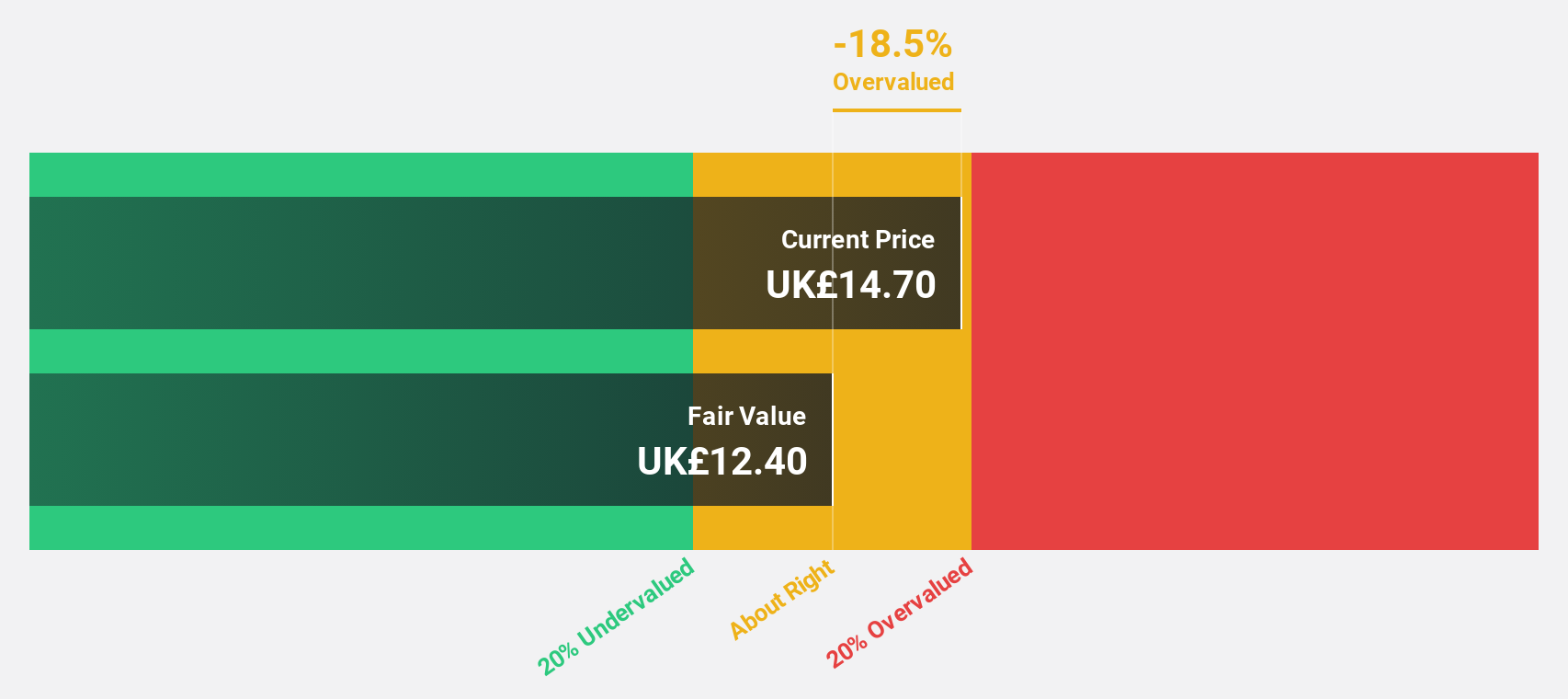

RHI Magnesita (LSE:RHIM)

Overview: RHI Magnesita N.V. is a company that develops, produces, sells, installs, and maintains refractory products and systems for industrial high-temperature processes globally, with a market capitalization of approximately £1.43 billion.

Operations: The company's revenue is derived from several key segments, including €441 million from India, €80 million from Minerals, €727 million from Europe & CIS, €536 million from Latin America, €863 million from North America, €377 million from China & East Asia, and €342 million from the Middle East, Türkiye & Africa.

Estimated Discount To Fair Value: 49.1%

RHI Magnesita is trading at £30.15, significantly below its estimated future cash flow value of £59.25, indicating potential undervaluation based on cash flows. While the company faces challenges with high debt levels and a dividend yield not fully covered by earnings, it benefits from expected annual earnings growth of 26.2%, surpassing the UK market average. However, revenue growth remains modest at 2.3% per year, with profit margins declining to 2.6% from last year's 4.1%.

- Our comprehensive growth report raises the possibility that RHI Magnesita is poised for substantial financial growth.

- Delve into the full analysis health report here for a deeper understanding of RHI Magnesita.

Sage Group (LSE:SGE)

Overview: The Sage Group plc provides technology solutions and services for small and medium businesses across North America, Europe, the United Kingdom, Ireland, Africa and Asia-Pacific with a market cap of £7.63 billion.

Operations: Revenue segments for Sage Group include £682 million from Europe and £1.19 billion from North America.

Estimated Discount To Fair Value: 33.3%

Sage Group is trading at £8.50, below its estimated future cash flow value of £12.75, reflecting potential undervaluation based on cash flows. Despite significant insider selling and high debt levels, Sage's earnings are projected to grow 12.73% annually, outpacing the UK market average. The company recently completed a share buyback worth £258 million and reported half-year sales growth from £1.24 billion to £1.36 billion, with net income rising to £196 million from the previous year's £180 million.

- Upon reviewing our latest growth report, Sage Group's projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Sage Group.

Where To Now?

- Reveal the 40 hidden gems among our Undervalued UK Stocks Based On Cash Flows screener with a single click here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com