Will Siemens' (XTRA:SIE) AI-Focused Chip Design Push Reshape Its Digitalization Narrative?

- Siemens has completed the integration of Brightly Software into its core brand as Asset Management Software, expanded its Asset Essentials solution into the UK, and enlarged its Saskatoon R&D hub to support AI-driven electronic design automation and semiconductor design.

- Together with third-party recognition of Siemens’ role in enterprise AI ecosystems, these moves deepen its position in software-enabled industrial asset management and chip design tools.

- Next, we’ll examine how Siemens’ expanded AI-driven semiconductor design R&D could influence the existing investment narrative around its digital and automation businesses.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Siemens Investment Narrative Recap

To own Siemens, you need to believe in its push to blend industrial hardware with higher margin software and AI, while managing cyclical demand in automation and infrastructure. The Brightly integration, UK rollout of Asset Essentials, and Saskatoon EDA expansion support that software and AI narrative, but they do not materially change the near term tension between solid revenue guidance and recent earnings compression, or the risk that weak Digital Industries demand and tough competition weigh on margins.

The Saskatoon expansion into AI driven semiconductor design looks most relevant here, because it connects directly to Siemens’ existing strengths in EDA and simulation, where software driven recurring revenues are an important potential offset to softer automation trends and integration risks in its broader portfolio.

Yet against this progress, the question of how much Siemens should lean into AI and data center exposure is something investors should be aware of, especially if...

Read the full narrative on Siemens (it's free!)

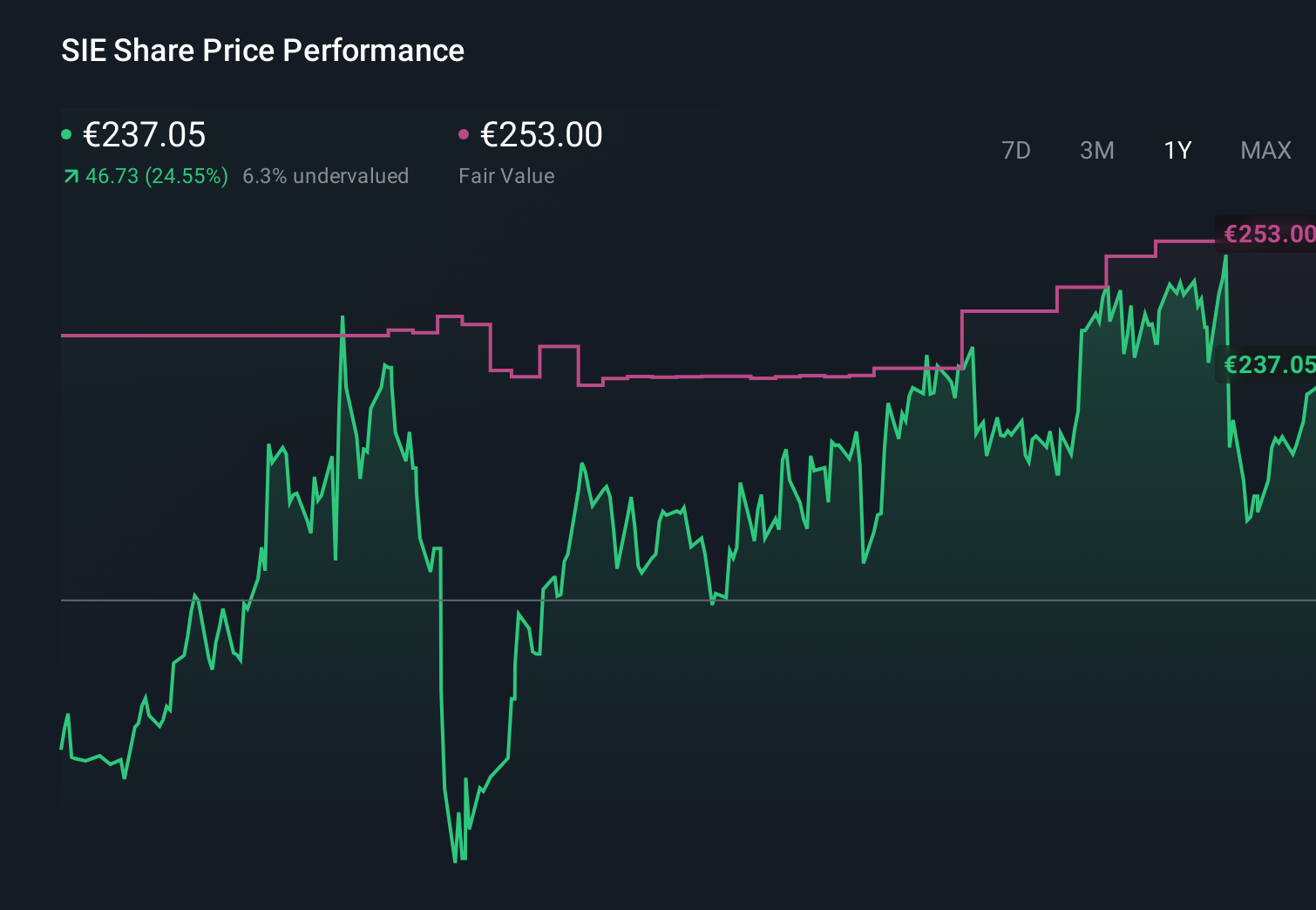

Siemens' narrative projects €93.6 billion revenue and €10.9 billion earnings by 2029. This requires 5.5% yearly revenue growth and about a €3.3 billion earnings increase from €7.6 billion today.

Uncover how Siemens' forecasts yield a €286.17 fair value, a 6% upside to its current price.

Exploring Other Perspectives

While the consensus view is cautious on growth, the most optimistic analysts were already penciling in about €108.8 billion of revenue and €13.8 billion of earnings by 2029, implying a far stronger payoff from AI and software than the baseline narrative, so you should weigh how news like the Saskatoon EDA build out could shift both that upside case and the risk of overreliance on AI related demand.

Explore 5 other fair value estimates on Siemens - why the stock might be worth just €286.17!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Siemens research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Siemens research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Siemens' overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com