3 Asian Stocks That May Be Undervalued By As Much As 35.6%

As geopolitical tensions and fluctuating energy prices continue to shape global markets, Asian equities have shown mixed performances, with some indices experiencing declines while others benefit from sector-specific rallies. Amidst this volatility, identifying undervalued stocks can be a strategic approach for investors seeking opportunities in the region's diverse economic landscape.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Samsung Electro-Mechanics (KOSE:A009150) | ₩1277000.00 | ₩2497698.83 | 48.9% |

| Rakus (TSE:3923) | ¥1019.00 | ¥2024.04 | 49.7% |

| Pan-United (SGX:P52) | SGD1.59 | SGD3.14 | 49.4% |

| NC Chem (KOSDAQ:A482630) | ₩13350.00 | ₩25814.95 | 48.3% |

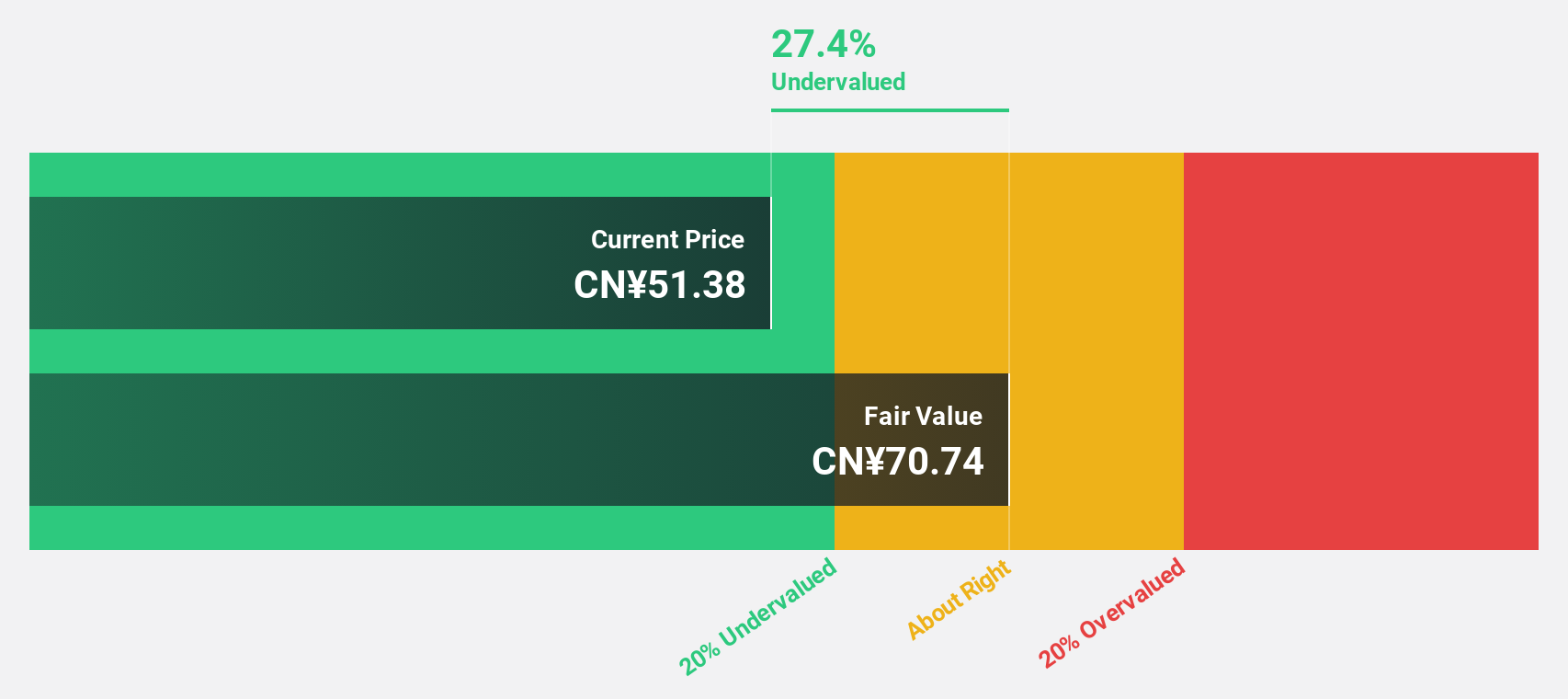

| Matrix Design (SZSE:301365) | CN¥37.58 | CN¥72.88 | 48.4% |

| Laopu Gold (SEHK:6181) | HK$373.40 | HK$745.96 | 49.9% |

| Huatu Cendes (SZSE:300492) | CN¥23.56 | CN¥45.75 | 48.5% |

| GreenEnergy (TSE:1436) | ¥1382.00 | ¥2699.40 | 48.8% |

| Citicore Renewable Energy (PSE:CREC) | ₱4.34 | ₱8.42 | 48.5% |

| BEAUTY GARAGE (TSE:3180) | ¥1475.00 | ¥2885.00 | 48.9% |

Let's take a closer look at a couple of our picks from the screened companies.

East Buy Holding (SEHK:1797)

Overview: East Buy Holding Limited is an investment holding company that operates a livestreaming e-commerce business for sales of private label products in the People's Republic of China, with a market cap of HK$25.63 billion.

Operations: The company generates revenue of CN¥4.52 billion from its online live commerce business in the People's Republic of China.

Estimated Discount To Fair Value: 25.3%

East Buy Holding is trading at HK$24.32, significantly below its estimated future cash flow value of HK$32.57, indicating it may be undervalued based on cash flows. The company's earnings are expected to grow at 24.7% annually over the next three years, outpacing the Hong Kong market's growth rate of 12.6%. Despite a low forecasted return on equity of 9%, recent profitability and ongoing share buybacks could enhance shareholder value and improve financial metrics further.

- Our comprehensive growth report raises the possibility that East Buy Holding is poised for substantial financial growth.

- Click here to discover the nuances of East Buy Holding with our detailed financial health report.

AcrobiosystemsLtd (SZSE:301080)

Overview: Acrobiosystems Co., Ltd. develops and manufactures recombinant proteins, antibodies, and other biological reagents for pharmaceutical and biotechnology companies, as well as research institutions, with a market cap of CN¥8.98 billion.

Operations: The company's revenue primarily comes from its Research and Experimental Development segment, which generated CN¥872.65 million.

Estimated Discount To Fair Value: 35.6%

Acrobiosystems Ltd. is trading at CN¥53.71, well below its estimated future cash flow value of CN¥83.35, highlighting potential undervaluation based on cash flows. The company's revenue and earnings are forecast to grow significantly at 20.2% and 28.6% annually, respectively, outpacing the Chinese market's averages. Despite an unstable dividend track record and low projected return on equity of 11.5%, a recent share buyback program could bolster shareholder value by reducing capital base.

- Insights from our recent growth report point to a promising forecast for AcrobiosystemsLtd's business outlook.

- Navigate through the intricacies of AcrobiosystemsLtd with our comprehensive financial health report here.

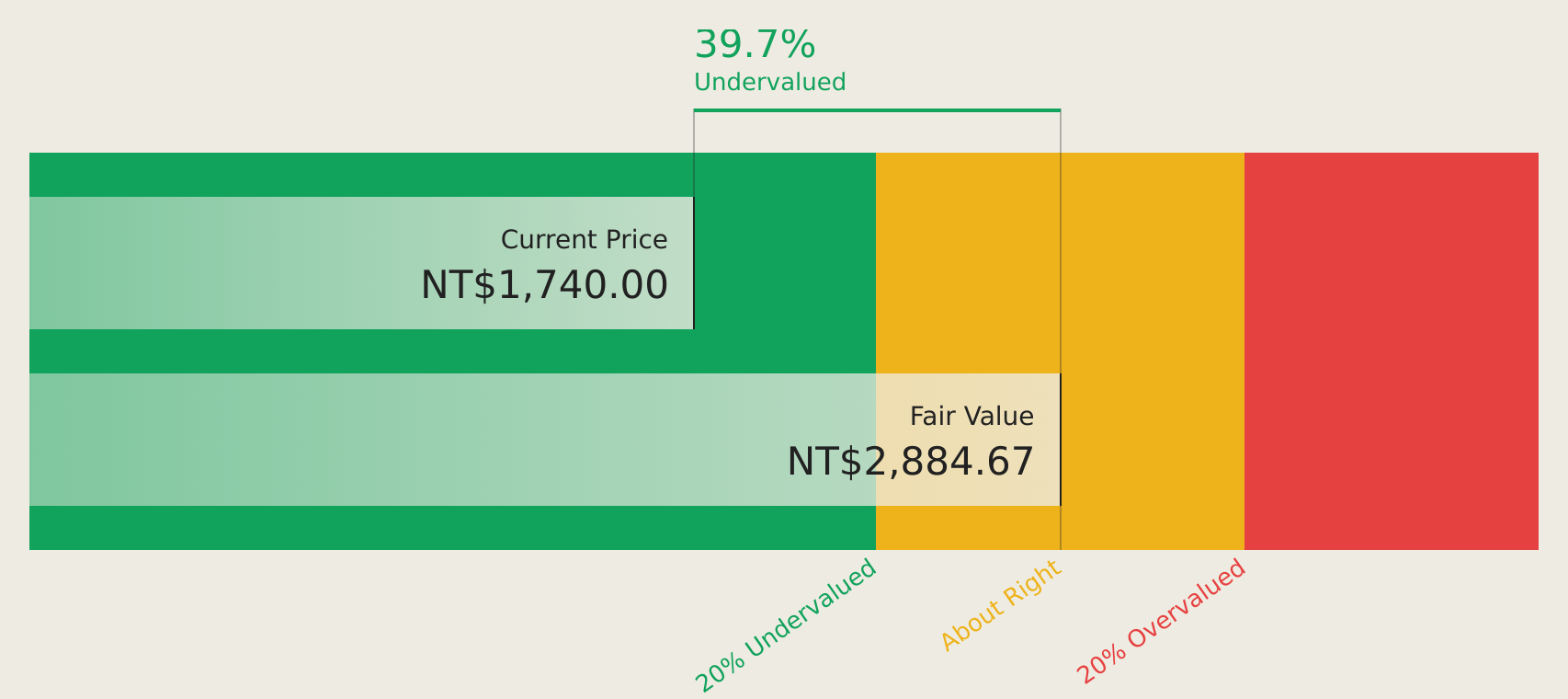

Delta Electronics (TWSE:2308)

Overview: Delta Electronics, Inc., along with its subsidiaries, offers power and thermal management solutions across Mainland China, the United States, Taiwan, Thailand, and other international markets with a market cap of NT$4.95 trillion.

Operations: Delta Electronics generates revenue through its Power Supply and Spare Parts Business Group (NT$305.88 billion), Infrastructure Business Group (NT$198.65 billion), Automation Business Group (NT$55.62 billion), and Transportation Business Group (NT$34.13 billion).

Estimated Discount To Fair Value: 33.7%

Delta Electronics, trading at NT$1,905, is significantly undervalued compared to its estimated future cash flow value of NT$2,875.01. Recent earnings growth of 77.4% and a forecasted annual profit increase of 29.7% suggest robust financial health. The company's innovative AI data center solutions showcased at COMPUTEX 2026 enhance operational efficiency and sustainability, potentially boosting future revenue streams in high-demand sectors like AI infrastructure and energy-intensive industries through strategic partnerships in Europe and the UK.

- Our earnings growth report unveils the potential for significant increases in Delta Electronics' future results.

- Take a closer look at Delta Electronics' balance sheet health here in our report.

Key Takeaways

- Delve into our full catalog of 193 Undervalued Asian Stocks Based On Cash Flows here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com