Yum! Brands (YUM) Stock Looks Fairly Valued After A 39% Run

Yum! Brands stock has returned 38.9% over the past five years, and after that steady climb the current market price around US$152 now sits close to what a Discounted Cash Flow (DCF) intrinsic value estimate and earnings multiples both suggest is a roughly fair valuation, even as fresh food safety headlines put its risk profile under closer scrutiny.

- A 38.9% gain over five years points to solid long term shareholder returns that now look more in line with a mature, fairly valued consumer stock than a clear bargain.

- The current investigation into a Cyclospora outbreak tied to fresh ingredients at Taco Bell may cap how much investors are willing to pay for Yum! Brands in the near term, even though its large scale and diversified restaurant portfolio can support expectations for ongoing cash generation.

- With a valuation score of 4 out of 6, Yum! Brands screens as a mixed picture rather than obviously cheap or clearly overpriced on the broader checks.

The issue now is whether Yum! Brands' current price already reflects the food safety risk and its recent performance, or if there is still a margin of safety for new investors.

Where Does Yum! Brands Sit on Cash Flow?

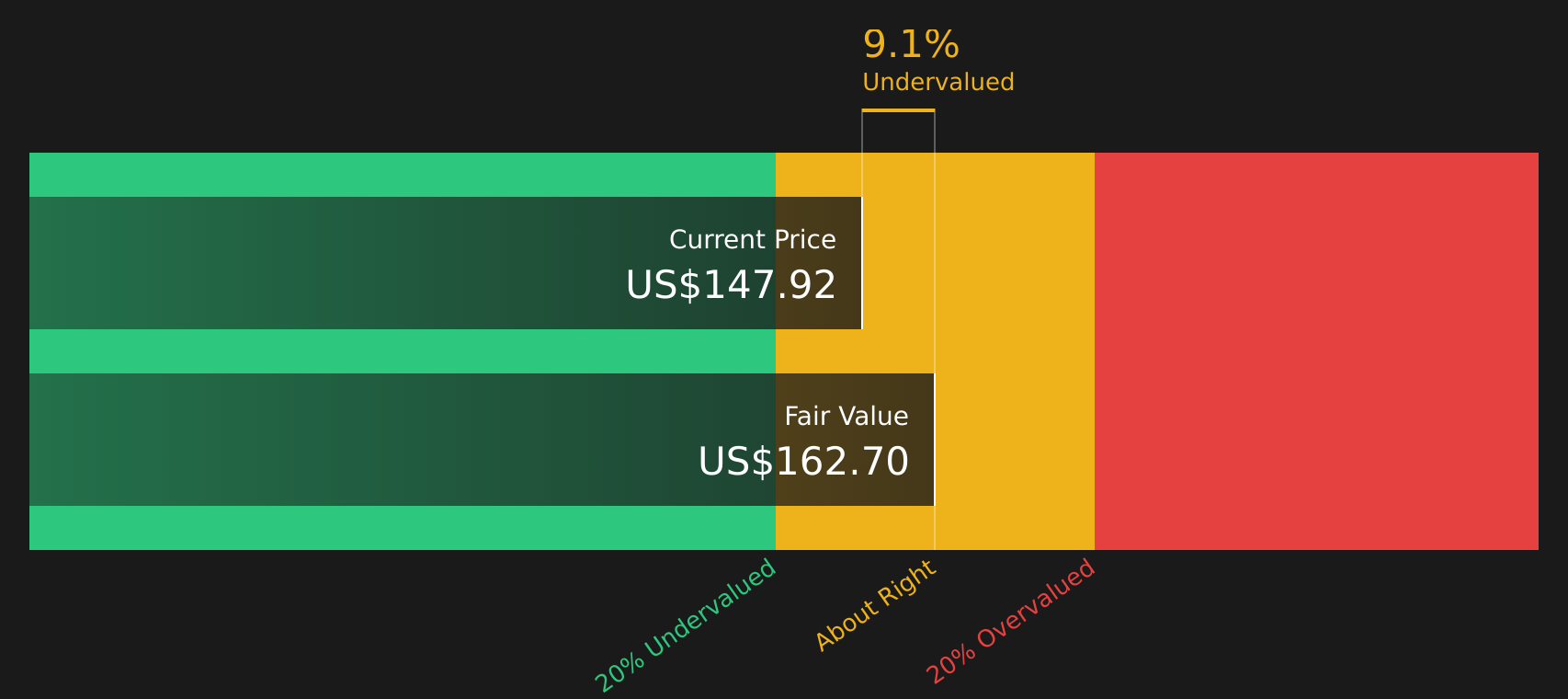

The Discounted Cash Flow (DCF) model estimates what Yum! Brands might be worth based on the cash it is expected to generate for shareholders. On this view, the company produced about $1.68b in free cash flow over the last twelve months, and the model assumes those cash flows continue growing over time rather than shrinking.

Putting those projections together, the DCF arrives at an estimated intrinsic value of about $162 per share, compared with a current share price near $152. This implies Yum! Brands screens as roughly 6.4% undervalued on this cash flow basis. The recent Cyclospora outbreak investigation at Taco Bell helps explain why the stock trades below that intrinsic estimate, as some investors appear to be pricing in higher risk around food safety and brand perception.

Overall, Yum! Brands appears to be trading close to the value suggested by its cash flows, with the current price sitting near that level.

Yum! Brands is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Is Yum! Brands Fairly Priced on Earnings?

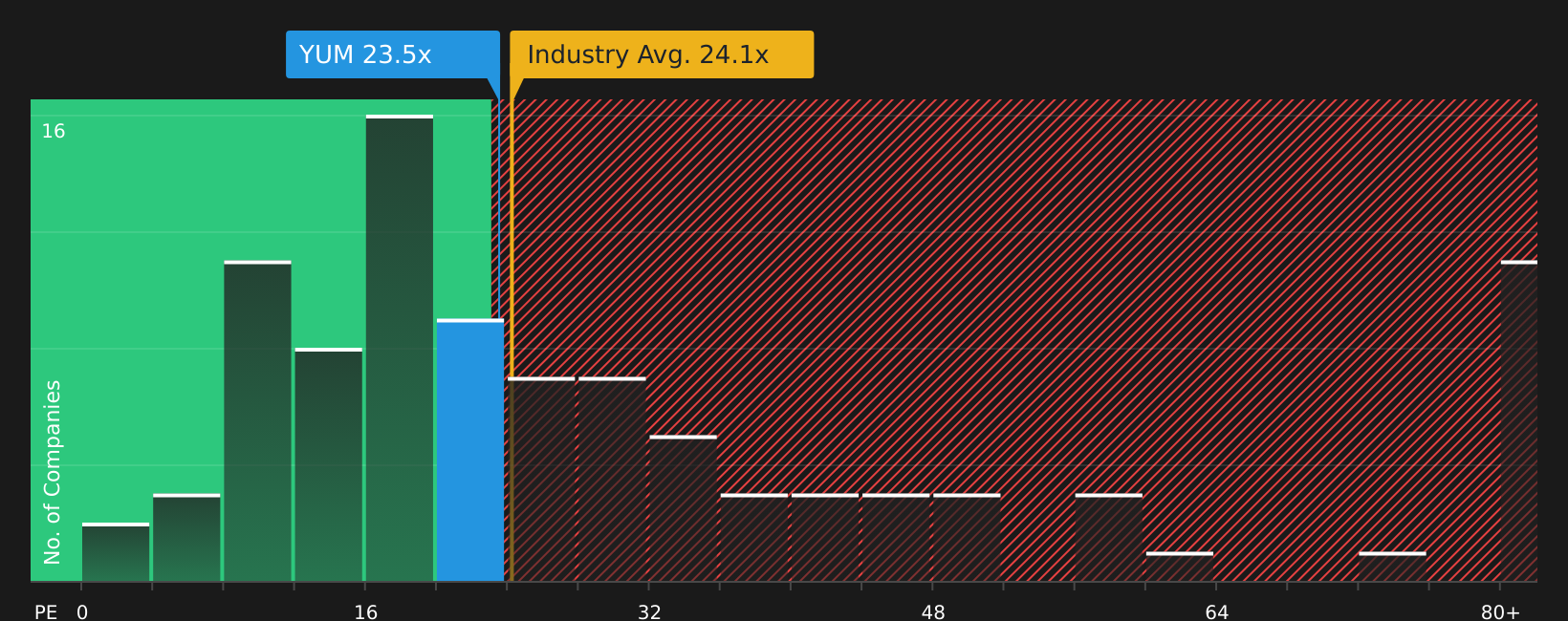

P/E is a useful check for Yum! Brands because earnings are a core focus for how investors price established consumer franchises. Yum! Brands currently trades on a P/E of about 24.1x, which is almost identical to both its tailored fair P/E of roughly 24.1x and the broader hospitality industry average of about 24.2x.

That tight clustering suggests the market is pricing Yum! Brands in line with what its earnings profile, size, and risk level would typically justify, rather than assigning a clear premium or discount. Peer companies on average trade closer to 40.4x earnings, so Yum! Brands sits well below that peer group, yet the fair ratio points to the current level as broadly appropriate rather than obviously cheap.

On balance, Yum! Brands appears roughly fairly valued on its current P/E multiple.

See what the numbers say about this price — find out in our valuation breakdown.

The Yum! Brands Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Yum! Brands build on the valuation work by outlining which paths for Yum! Brands' growth, margins, and earnings would need to materialise for the stock to be worth meaningfully more or less than its current price. Each narrative links a fair value estimate to a clear storyline about Yum! Brands' potential catalysts and risks, so you can observe over time which version of events is actually unfolding on the Community page.

Share a narrative on Yum! Brands to set out your number driven view on whether Taco Bell's Cyclospora response and the current valuation add up, and see how your thesis holds up as new data and news arrive.

Do you think there's more to the story for Yum! Brands? Head over to our Community to see what others are saying!

The Bottom Line

For Yum! Brands, the Discounted Cash Flow (DCF) view and the earnings multiple both point to a stock that looks roughly fairly valued rather than clearly mispriced. The small intrinsic value gap suggests there may be only a modest valuation cushion, so the real swing factor from here is how comfortably investors live with the food safety and brand risks highlighted by the recent Taco Bell investigation. The core debate is whether that risk is now adequately reflected in the price, or if it still justifies a tighter margin of safety before you commit fresh capital.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com