Middle Eastern Dividend Stocks To Consider For Your Portfolio

As geopolitical tensions between the U.S. and Iran escalate, many Gulf markets remain subdued, reflecting broader economic uncertainties affecting investor sentiment in the region. In such a climate, dividend stocks can offer a degree of stability and income potential for investors seeking to navigate market volatility while benefiting from consistent cash flows.

Top 10 Dividend Stocks In The Middle East

| Name | Dividend Yield | Dividend Rating |

| Yeni Gimat Gayrimenkul Yatirim Ortakligi (IBSE:YGGYO) | 3.19% | ★★★★★★ |

| Turkiye Garanti Bankasi (IBSE:GARAN) | 3.41% | ★★★★★☆ |

| Saudi Awwal Bank (SASE:1060) | 6.21% | ★★★★★☆ |

| National General Insurance (P.J.S.C.) (DFM:NGI) | 7.92% | ★★★★★☆ |

| Matrix IT (TASE:MTRX) | 4.06% | ★★★★★☆ |

| Emirates Insurance Company P.J.S.C (ADX:EIC) | 7.41% | ★★★★★★ |

| Emaar Properties PJSC (DFM:EMAAR) | 8.65% | ★★★★★☆ |

| Dubai Insurance Company (P.S.C.) (DFM:DIN) | 5.88% | ★★★★★☆ |

| Arab National Bank (SASE:1080) | 6.25% | ★★★★★☆ |

| Anadolu Hayat Emeklilik Anonim Sirketi (IBSE:ANHYT) | 7.98% | ★★★★★☆ |

Click here to see the full list of 70 stocks from our Top Middle Eastern Dividend Stocks screener.

Let's uncover some gems from our specialized screener.

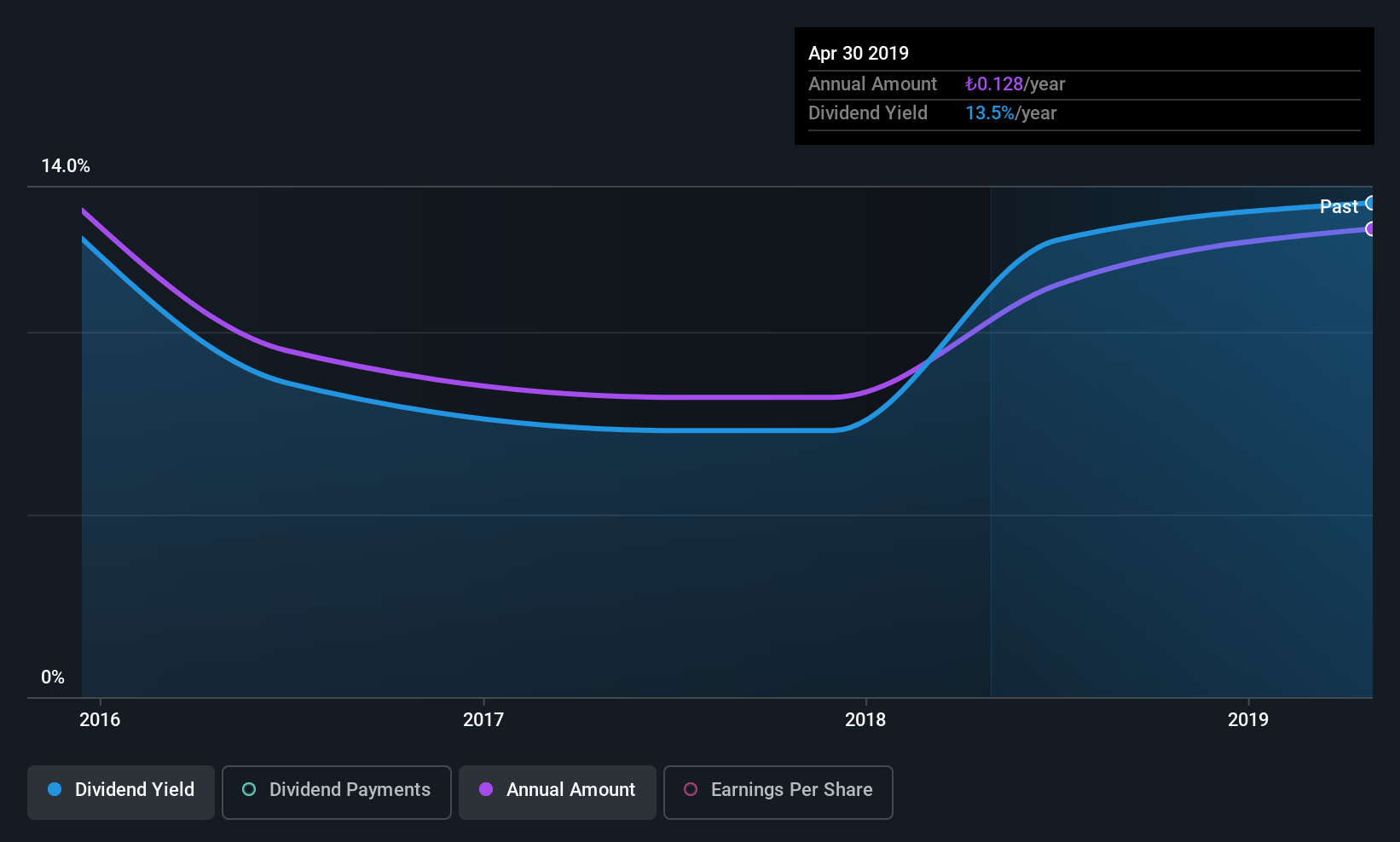

OYAK Çimento Fabrikalari (IBSE:OYAKC)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: OYAK Çimento Fabrikalari A.S., along with its subsidiaries, is involved in the production and sale of clinker and cement in Turkey, with a market cap of TRY98.69 billion.

Operations: OYAK Çimento Fabrikalari's revenue is primarily derived from its Cement segment, contributing TRY34.25 billion, and its Ready-Mixed Concrete segment, which adds TRY19.41 billion.

Dividend Yield: 4.9%

OYAK Çimento Fabrikalari's dividend yield of 4.93% ranks in the top 25% of Turkish market payers, yet its sustainability is questionable due to a high cash payout ratio of 165%, indicating dividends are not well covered by free cash flows. Despite trading at good value and below analyst price targets, recent earnings have decreased significantly. While dividends have grown over the past decade, they have been volatile and unreliable, with inconsistent growth patterns.

- Get an in-depth perspective on OYAK Çimento Fabrikalari's performance by reading our dividend report here.

- Our valuation report unveils the possibility OYAK Çimento Fabrikalari's shares may be trading at a discount.

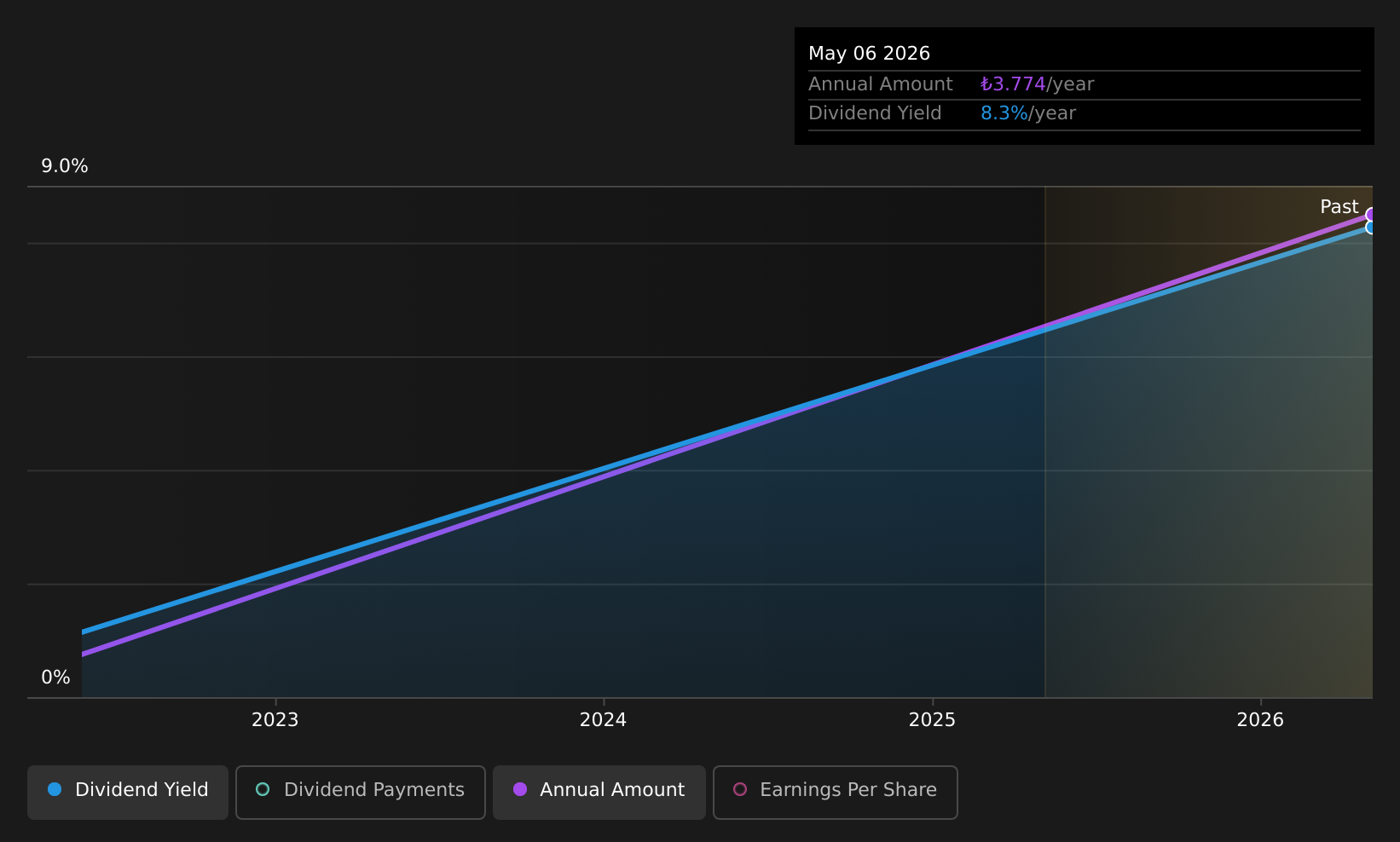

Oyak Yatirim Menkul Degerler (IBSE:OYYAT)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Oyak Yatirim Menkul Degerler A.S., along with its subsidiaries, offers research, brokerage, portfolio management, corporate finance, and fund operation services for capital market instruments in Turkey and has a market cap of TRY12.19 billion.

Operations: Oyak Yatirim Menkul Degerler A.S. generates revenue through its services in research, brokerage, portfolio management, corporate finance, and fund operations related to capital market instruments in Turkey.

Dividend Yield: 9.3%

Oyak Yatirim Menkul Degerler's dividend yield of 9.29% places it among the top payers in Turkey, supported by a low cash payout ratio of 29.7% and a reasonable earnings payout ratio of 60.4%. However, its dividends have been unreliable and volatile over the past four years, with an unstable track record despite recent earnings growth. The company's price-to-earnings ratio of 6.5x suggests good value compared to the Turkish market average.

- Unlock comprehensive insights into our analysis of Oyak Yatirim Menkul Degerler stock in this dividend report.

- The valuation report we've compiled suggests that Oyak Yatirim Menkul Degerler's current price could be inflated.

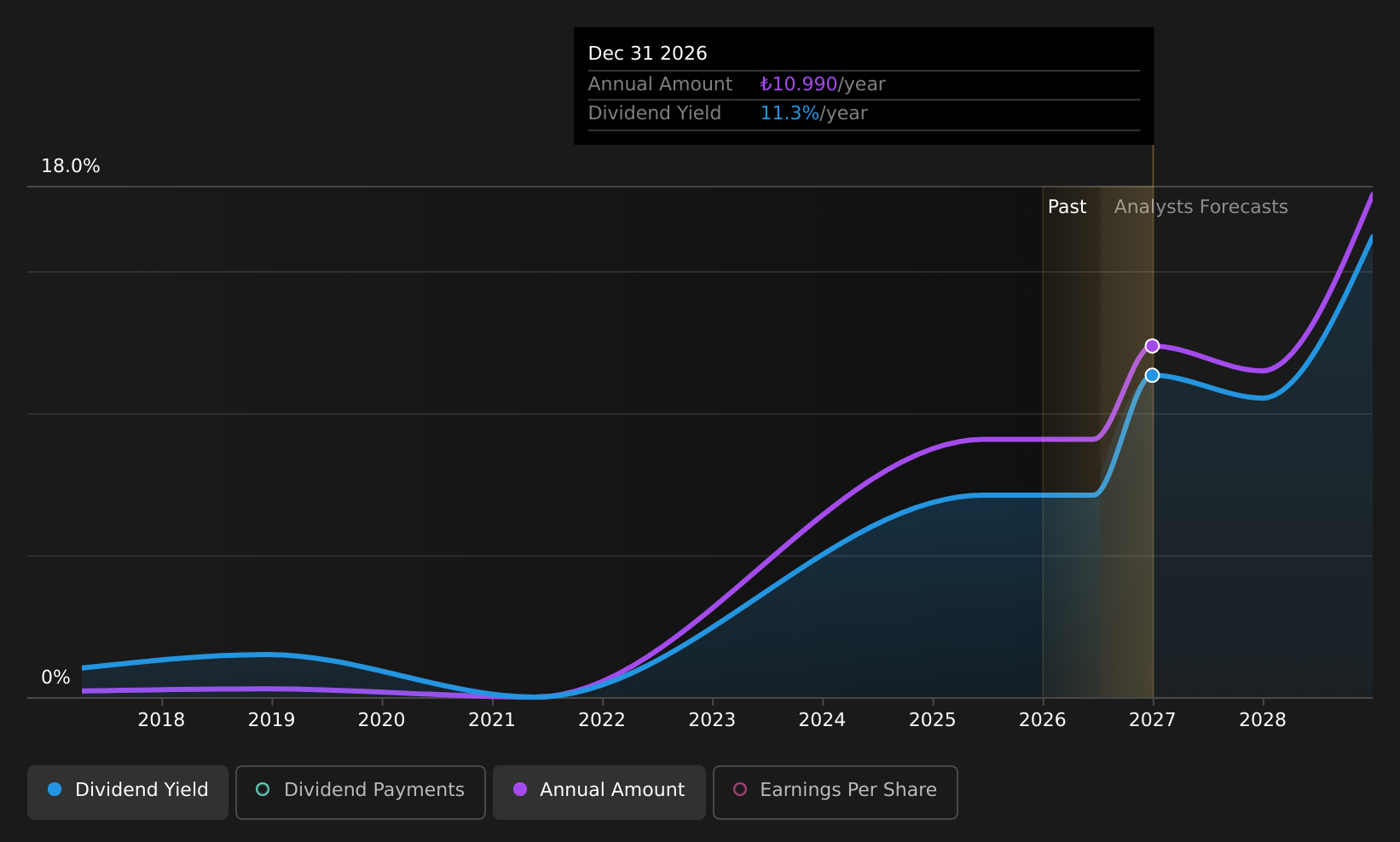

Ülker Bisküvi Sanayi (IBSE:ULKER)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Ülker Bisküvi Sanayi A.S. is a company that, along with its subsidiaries, produces and distributes biscuits, chocolates, chocolate-coated biscuits, wafers, and cakes both in Turkey and internationally, with a market cap of TRY36.58 billion.

Operations: Ülker Bisküvi Sanayi A.S. generates revenue primarily from the marketing and sales of biscuits, chocolate biscuits, wafers, cakes, and chocolates amounting to TRY110.53 billion.

Dividend Yield: 8.1%

Ülker Bisküvi Sanayi offers a competitive dividend yield of 8.15%, placing it in the top 25% of Turkish dividend payers. Despite a low payout ratio of 48.6% and cash payout ratio of 41.7%, indicating good coverage, its dividends have been unstable and volatile over the past decade, with recent decreases to TRY 5.73 per share. The company faces challenges with declining profit margins and earnings, impacting overall financial stability despite trading at a significant discount to estimated fair value.

- Take a closer look at Ülker Bisküvi Sanayi's potential here in our dividend report.

- According our valuation report, there's an indication that Ülker Bisküvi Sanayi's share price might be on the cheaper side.

Key Takeaways

- Click here to access our complete index of 70 Top Middle Eastern Dividend Stocks.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com