3 Australian Dividend Stocks For Reliable Income In Uncertain Markets

With inflation readings mixed, bond yields shifting across major markets and policy signals from central banks still in flux, the appeal of cash flow you can see and count is front and center again. Reliable dividend income offers a way to stay invested while letting regular payouts contribute to total returns. The Dividend Powerhouses screener focuses on companies with a 5%+ yield that is covered, growing and historically stable. In this article, you will see three stocks from that list and how their dividend profiles might fit into a long term income strategy.

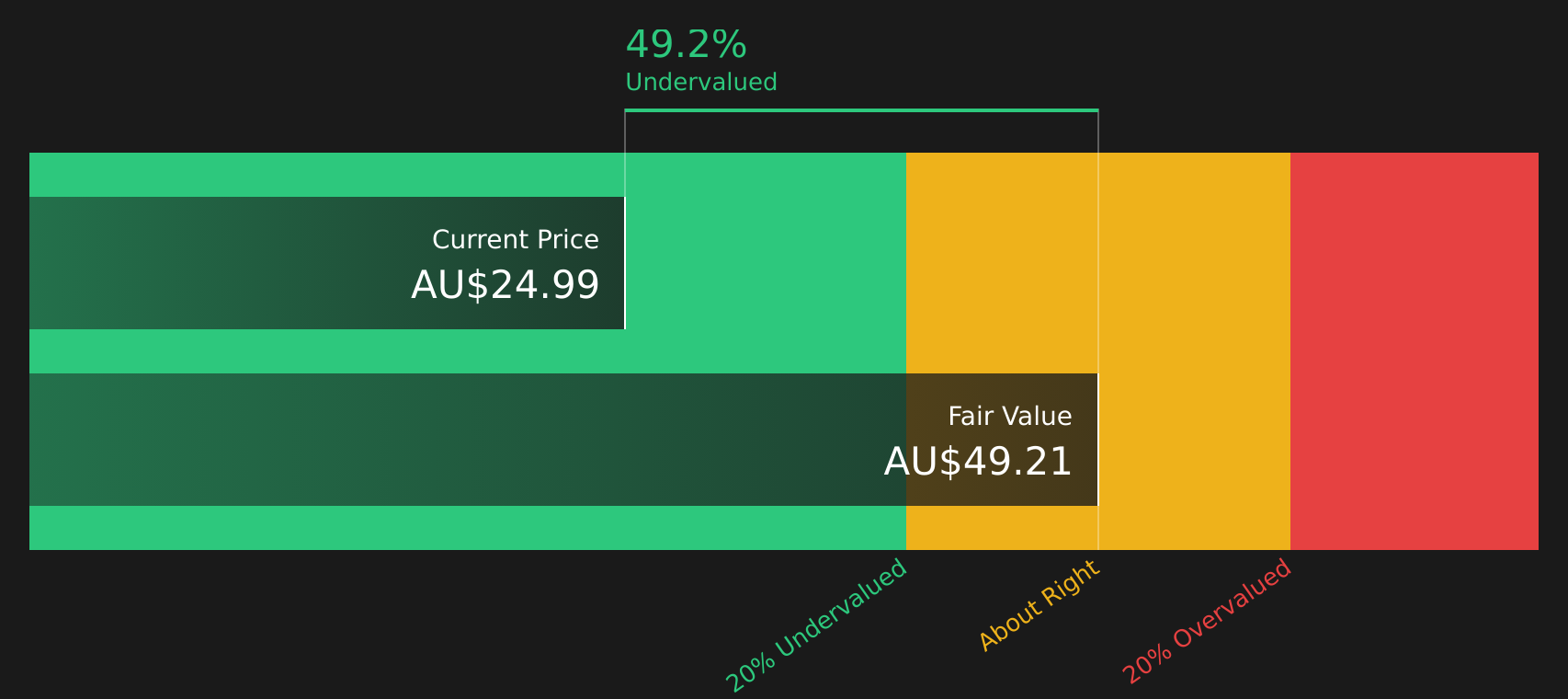

CSL (ASX:CSL)

Overview: CSL is a global biopharmaceutical group that develops and manufactures plasma derived therapies, vaccines and treatments for conditions such as immune disorders, bleeding disorders, iron deficiency and kidney disease, operating through its CSL Behring, CSL Seqirus and CSL Vifor segments across Australia, the United States, Europe, China and other markets.

Operations: CSL generates most of its revenue from CSL Behring at about US$10.9b, with CSL Vifor contributing about US$2.4b and CSL Seqirus about US$2.2b, supported by large customer bases in the United States at about US$7.3b and the Rest of World at about US$4.6b.

Market Cap: A$58.4b

CSL stands out on the Dividend Powerhouses list because it combines a 3.42% yield with a globally important plasma and vaccine business that holds a significant competitive position after a challenging period. The stock is trading well below Simply Wall St's estimate of fair value, which may appeal to investors who focus on income plus potential capital upside. The trade off is that the company currently has a high P/E, substantial use of debt, weak earnings over the past year and a dividend that is not well covered by current profits. For investors willing to look past one off hits and recent underperformance, the full CSL story is more complex and potentially more interesting than the share price alone suggests.

CSL’s mix of a 3.42% yield, a global plasma and vaccine footprint, and a share price below one estimate of fair value suggests the market may be missing key context, and the real twist shows up in the 2 key rewards and 4 important warning signs

QBE Insurance Group (ASX:QBE)

Overview: QBE Insurance Group is a global insurer and reinsurer based in Sydney that provides a wide range of cover including property, motor, liability, workers’ compensation, crop and specialty insurance, as well as managing Lloyd’s syndicates and investment portfolios across Australia Pacific, North America and other international markets.

Operations: QBE Insurance Group generates most of its revenue from International at about US$11.2b, with North America contributing about US$8.2b, Australia Pacific about US$5.7b and Corporate & Other about US$77m.

Market Cap: A$37.1b

QBE Insurance Group earns a place on the Dividend Powerhouses list because it combines a sizeable global footprint, improving profitability and a valuation that sits well below one cash flow based fair value estimate, even as analysts expect only modest revenue growth and a lower future return on equity. The trade off is real, including an unstable dividend history, reliance on external borrowing rather than deposits and exposure to underwriting volatility and natural catastrophe losses. Recent moves such as the full buyout of its Indian joint venture and steady investment in cyber and digital capabilities hint at an insurer that is quietly reshaping its mix. The full QBE story around earnings quality, capital strength and dividend capacity runs deeper than headline yield alone suggests.

QBE Insurance Group’s global reach and improving profitability are only half the story. The real tension is how its earnings quality, capital strength and dividend capacity fit together in the 2 key rewards and 1 important warning sign

Evolution Mining (ASX:EVN)

Overview: Evolution Mining is an Australian based gold producer that explores, develops and operates gold and gold copper mines in Australia and Canada, selling gold and gold copper concentrates while also pursuing copper and silver opportunities.

Operations: Evolution Mining generates most of its revenue from Cowal at about A$1.7b and Ernest Henry at about A$1.1b, with additional contributions from Mungari at about A$780m, Red Lake at about A$670m, Northparkes at about A$580m, Mt Rawdon at about A$150m and Corporate at about A$160m.

Market Cap: A$22.3b

Evolution Mining brings together high margin gold production, strong ESG credentials and meaningful copper and lithium exposure through assets like Ernest Henry and the Nevada North Lithium joint venture. These collectively support a case for resilient cash generation even as compliance and labor costs weigh on sector profitability. Earnings growth has been strong, margins are healthy at around 26% and return on equity is high, yet the stock screens as expensive relative to the broader metals and mining industry and carries an unstable dividend record. For an income focused investor, the key question is how this combination of quality assets, cost pressures and an evolving commodity mix influences the durability of future payouts and valuation support beyond the headline yield.

Evolution Mining’s high margin gold production, copper leverage and lithium option are only part of the puzzle; the bigger question is how all of this is reflected in the analysis report for Evolution Mining

The three stocks covered here are only a starting point, with the full Dividend Powerhouses screen surfacing 28 more companies that combine 5%+ yields with covered, growing and historically stable dividends, each with its own income story and risk trade off, inside the Dividend Powerhouses (3%+ Yield) screener. Using Simply Wall St, you can quickly identify, analyze and filter for the specific catalysts and narratives that matter most to you, so you can focus on the highest conviction dividend ideas for your portfolio.

Take Control of Your Investment Journey

If Evolution Mining or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh breakout stories and under the radar stocks rarely stay quiet for long. Momentum can build, prices can move and the best entry points can be taken quickly, so consider acting in a timely way.

- Spot companies quietly building momentum across sectors and use the 8 resilient stocks with low risk scores to focus on opportunities where balance sheets and risk scores aim to keep downside in check.

- Target fast growing themes in automation and industry 4.0 by running the 32 robotics and automation stocks and focus on businesses positioned to benefit if robotics spending increases.

- Seek exposure to critical metals with the 29 best rare earth metal stocks while these producers are still under the radar and before any renewed demand stories start influencing prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com