European Market's Hidden Gems Estimated Below Fair Value July 2026

As geopolitical tensions and energy market volatility capture global attention, European stocks have experienced a downturn, with the STOXX Europe 600 Index falling by 1.79% amidst concerns over inflation and potential monetary policy tightening. In this environment, identifying undervalued stocks becomes crucial as investors seek opportunities that may offer resilience against market fluctuations.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Vossloh (XTRA:VOS) | €58.55 | €115.61 | 49.4% |

| VIGO Photonics (WSE:VGO) | PLN500.00 | PLN993.48 | 49.7% |

| New Wave Group (OM:NEWA B) | SEK92.60 | SEK180.07 | 48.6% |

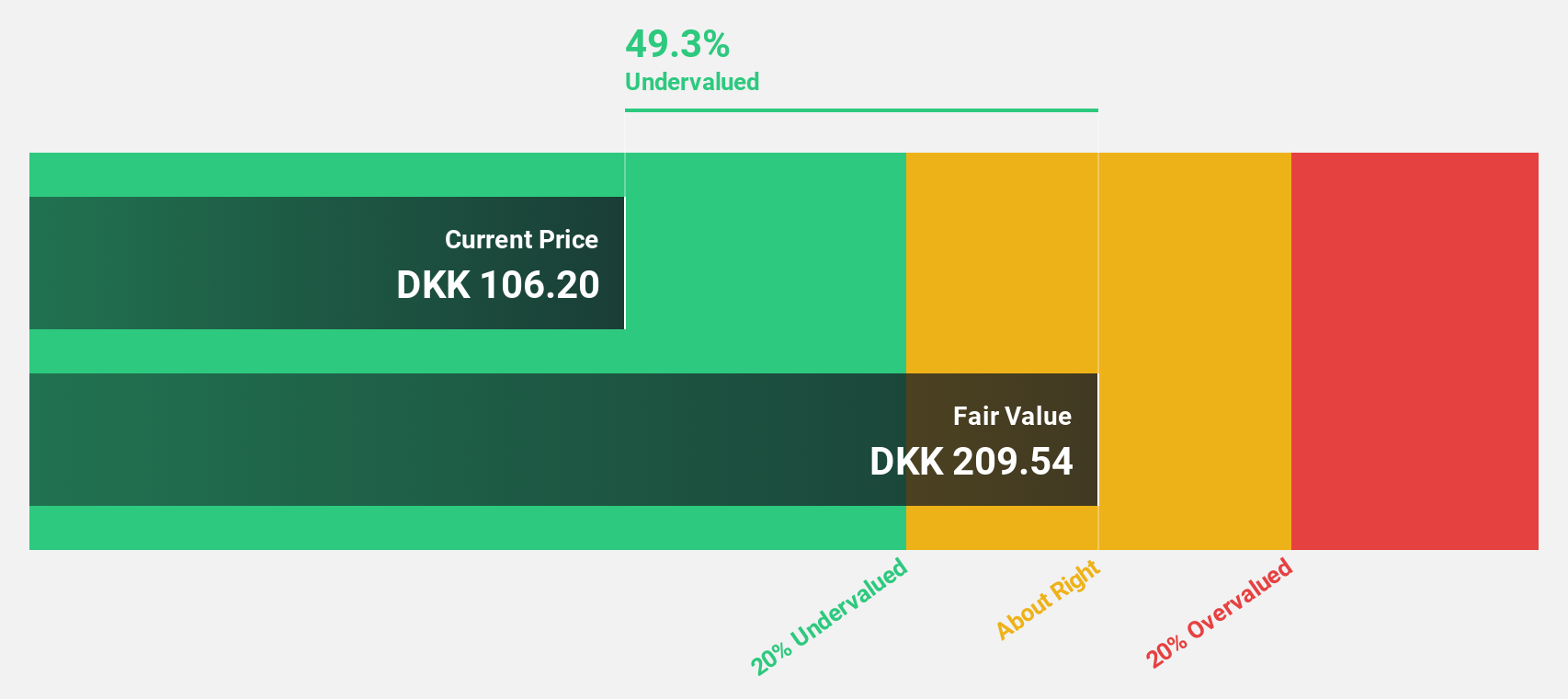

| Netcompany Group (CPSE:NETC) | DKK309.00 | DKK606.27 | 49% |

| Micro Systemation (OM:MSAB B) | SEK82.20 | SEK160.16 | 48.7% |

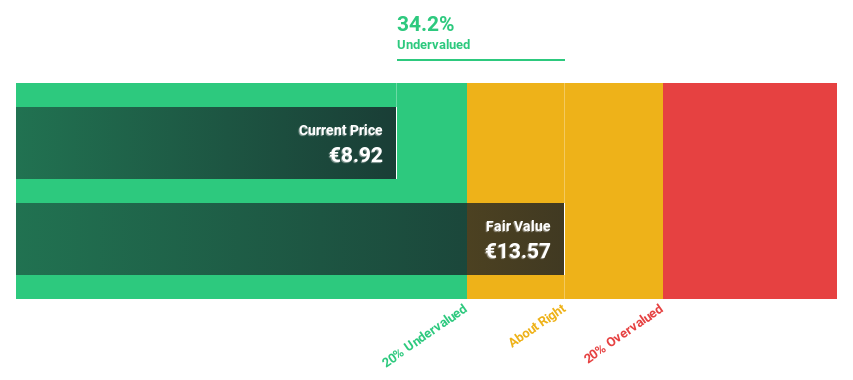

| Koskisen Oyj (HLSE:KOSKI) | €8.58 | €17.14 | 49.9% |

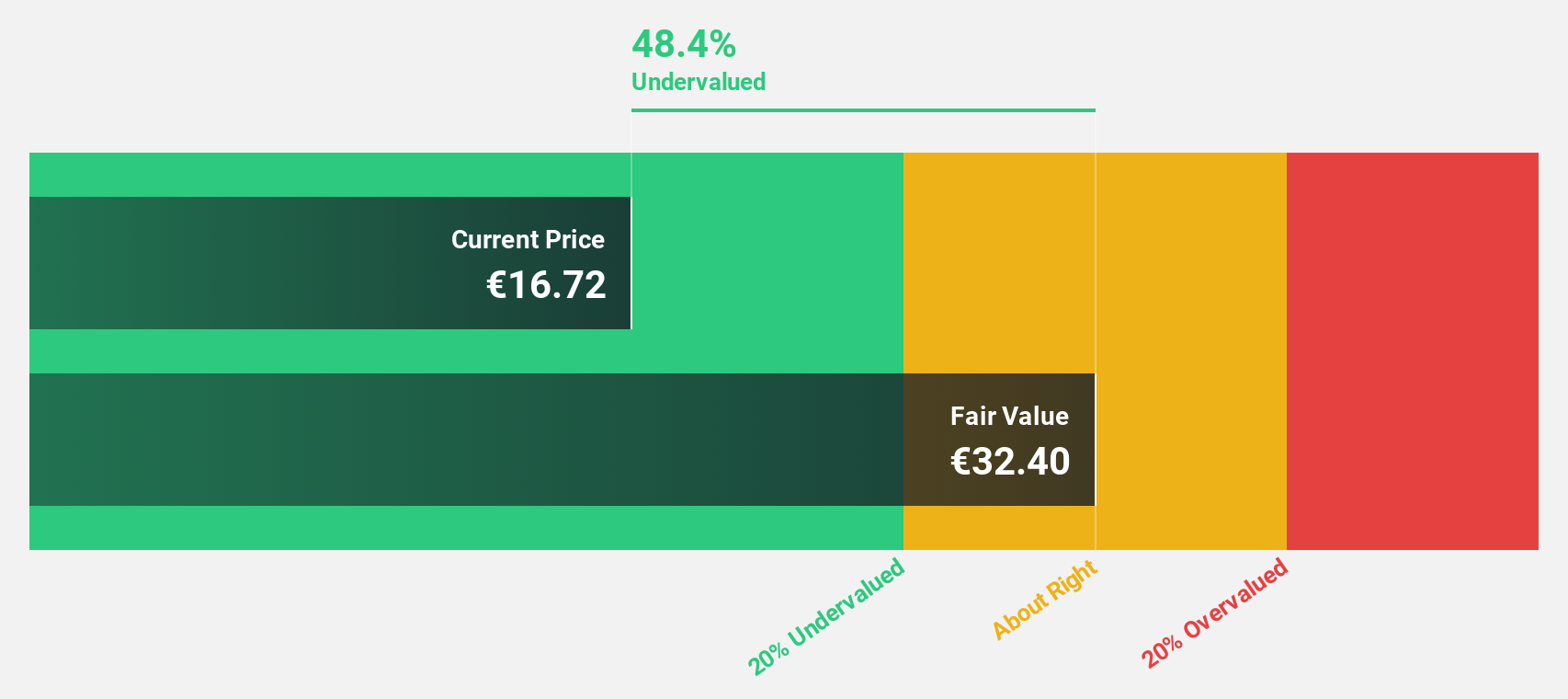

| Jerónimo Martins SGPS (ENXTLS:JMT) | €16.22 | €31.72 | 48.9% |

| Hiab Oyj (HLSE:HIAB) | €53.75 | €106.73 | 49.6% |

| Dustin Group (OM:DUST) | SEK1.844 | SEK3.56 | 48.2% |

| Casta Diva Group (BIT:CDG) | €3.09 | €6.06 | 49% |

Here's a peek at a few of the choices from the screener.

Vestas Wind Systems (CPSE:VWS)

Overview: Vestas Wind Systems A/S is involved in the design, manufacture, installation, and servicing of wind turbines across the United States, Denmark, and internationally with a market cap of DKK175.18 billion.

Operations: Vestas generates revenue primarily from two segments: Service, which accounts for €3.69 billion, and Power Solutions, contributing €15.64 billion.

Estimated Discount To Fair Value: 21.5%

Vestas Wind Systems is trading at 21.5% below its estimated fair value, with shares undervalued by over 20% based on discounted cash flow analysis. Despite slower revenue growth forecasts of 7.3% annually, earnings are expected to grow at a robust rate of 18.2%, outpacing the Danish market's average. Recent earnings reports show significant improvement, with Q1 net income rising to €82 million from €5 million year-over-year, supporting its strong cash flow position.

- Our comprehensive growth report raises the possibility that Vestas Wind Systems is poised for substantial financial growth.

- Get an in-depth perspective on Vestas Wind Systems' balance sheet by reading our health report here.

Metso Oyj (HLSE:METSO)

Overview: Metso Oyj operates in the aggregates, minerals processing, and metals refining industries across various global regions, offering technologies and services with a market cap of €12.74 billion.

Operations: The company's revenue is primarily derived from its Minerals segment, which generated €4.02 billion, and its Aggregates segment, contributing €1.26 billion.

Estimated Discount To Fair Value: 27.9%

Metso Oyj is trading at 27.9% below its estimated fair value of €21.33, indicating a significant undervaluation based on discounted cash flow analysis. The company's earnings are projected to grow at 13.7% annually, surpassing the Finnish market's average growth rate of 13.5%. Recent Q1 results showed sales rising to €1.25 billion and net income increasing to €124 million, reinforcing its solid cash flow standing amidst moderate revenue growth forecasts of 6.8% per year.

- Our earnings growth report unveils the potential for significant increases in Metso Oyj's future results.

- Take a closer look at Metso Oyj's balance sheet health here in our report.

Delivery Hero (XTRA:DHER)

Overview: Delivery Hero SE offers online food ordering, quick commerce, and delivery services with a market cap of €11.60 billion.

Operations: The company's revenue segments include €4.42 billion from Asia, €2.49 billion from Europe, €1.06 billion from the Americas, and €4.03 billion from MENA (Middle East and North Africa), along with €3.19 billion generated through Integrated Verticals.

Estimated Discount To Fair Value: 40.4%

Delivery Hero is trading at 40.4% below its estimated fair value of €64.07, highlighting its undervaluation based on discounted cash flow analysis. Despite recent volatility, the company's earnings have grown 10% annually over five years and are forecast to grow significantly at 96.5% per year, with revenue expected to increase by 9% annually. Uber's proposed acquisition for €8.2 billion underscores strategic interest in Delivery Hero's potential amidst ongoing portfolio reviews and asset sales like Woowa Brothers Corp.

- Our growth report here indicates Delivery Hero may be poised for an improving outlook.

- Unlock comprehensive insights into our analysis of Delivery Hero stock in this financial health report.

Where To Now?

- Unlock more gems! Our Undervalued European Stocks Based On Cash Flows screener has unearthed 198 more companies for you to explore.Click here to unveil our expertly curated list of 201 Undervalued European Stocks Based On Cash Flows.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com