How Investors Are Reacting To Philip Morris International (PM) Winning FDA Modified Risk Status For ZYN

- Philip Morris International recently received U.S. Food and Drug Administration authorization to commercialize its ZYN smoke-free nicotine pouches as modified risk tobacco products, the first nicotine pouch brand to gain this designation, after submitting extensive scientific evidence that switching completely from cigarettes to ZYN reduces exposure to harmful chemicals linked to major smoking-related diseases.

- This decision gives Philip Morris International a unique regulatory position in the U.S. nicotine pouch category, strengthening its push to shift adult smokers toward smoke-free alternatives while highlighting the FDA’s willingness to differentiate between combustible and oral nicotine products.

- We’ll now examine how ZYN’s modified risk authorization may influence Philip Morris International’s smoke-free growth outlook and overall investment narrative.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

Philip Morris International Investment Narrative Recap

To own Philip Morris International, you need to believe its shift from cigarettes to smoke free products can support earnings while managing regulatory and tax pressures. The FDA’s modified risk authorization for ZYN reinforces PMI’s smoke free narrative, but it does not remove key near term risks such as potential slowdowns in smoke free adoption or new restrictions in the EU that could weigh on revenue and margins.

The upcoming July 22, 2026 webcast on second quarter and first half results is especially relevant here, as management will likely discuss early commercial learnings around ZYN’s modified risk status, progress across the broader smoke free portfolio, and how these developments fit with existing EPS guidance. For investors watching catalysts, this update could help clarify whether smoke free momentum is offsetting structural declines in combustibles and ongoing currency and illicit trade headwinds.

Yet beneath the positive headlines, investors should also be aware that tighter future regulations on smoke free products could...

Read the full narrative on Philip Morris International (it's free!)

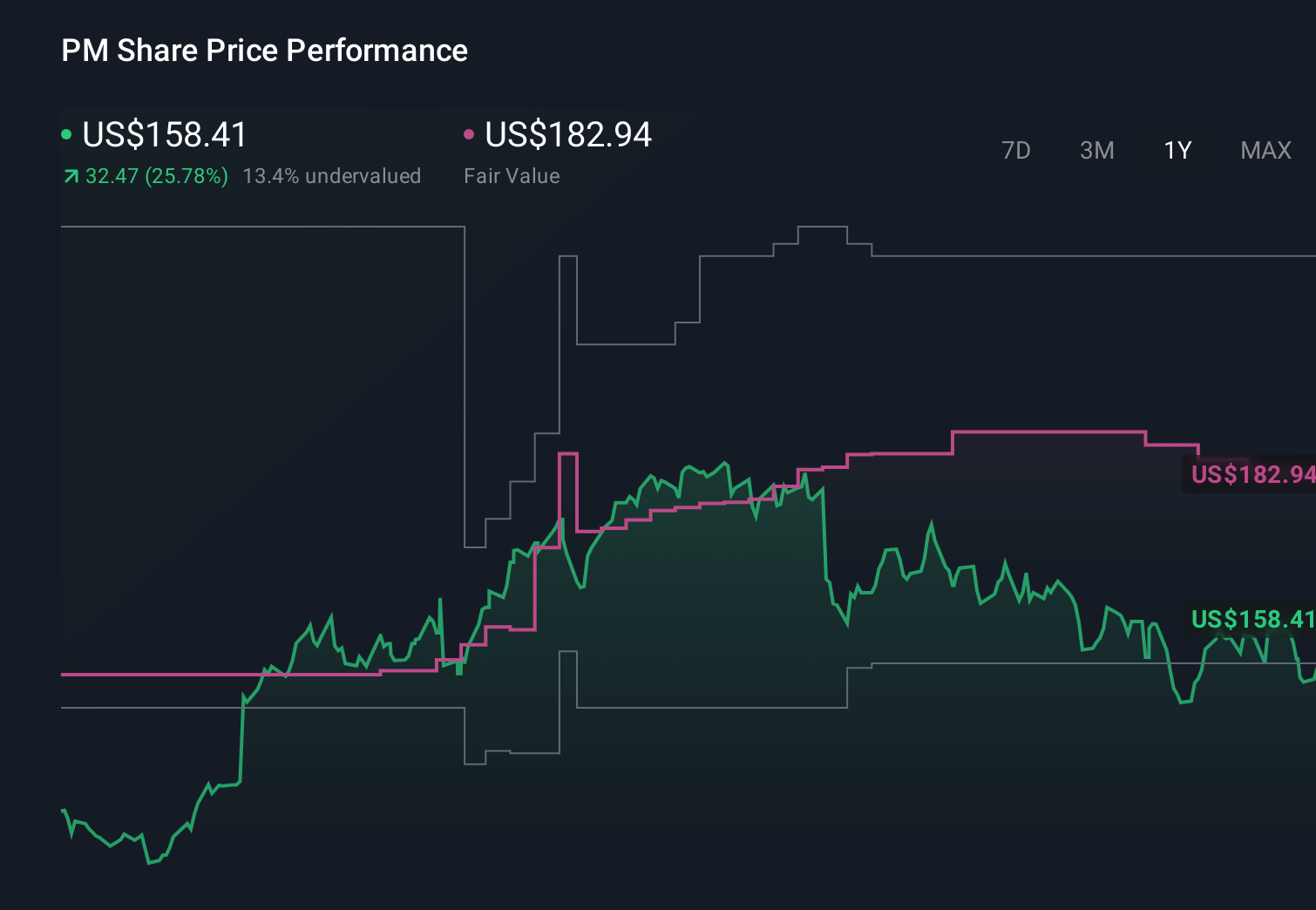

Philip Morris International's narrative projects $49.6 billion revenue and $15.3 billion earnings by 2029. This requires 6.1% yearly revenue growth and a $4.2 billion earnings increase from $11.1 billion today.

Uncover how Philip Morris International's forecasts yield a $193.14 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Before this FDA decision, the most optimistic analysts already expected revenue to reach about US$54,000,000,000 and earnings US$16,200,000,000 by 2029, so you may see their bullish view on faster smoke free growth and heavier regulatory risks either reinforced or challenged as new data emerge, reminding you that reasonable investors can look at the same stock and reach very different conclusions.

Explore 7 other fair value estimates on Philip Morris International - why the stock might be worth as much as 16% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Philip Morris International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com