Undervalued Asian Small Caps With Insider Action In July 2026

In July 2026, the Asian markets are navigating a landscape marked by geopolitical tensions and fluctuating energy prices, which have influenced investor sentiment across global indices. Despite these challenges, small-cap stocks in Asia present intriguing opportunities as investors look for potential growth amidst broader market volatility. Identifying promising small caps often involves examining insider actions and understanding how these companies might leverage current economic conditions to their advantage.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.1x | 0.9x | 30.82% | ★★★★★★ |

| FINEOS Corporation Holdings | 446.0x | 3.0x | 35.24% | ★★★★★★ |

| China XLX Fertiliser | 11.0x | 0.4x | 49.33% | ★★★★★☆ |

| Centurion | 12.2x | 4.2x | 32.25% | ★★★★★☆ |

| Paragon Care | NA | 0.1x | 30.97% | ★★★★★☆ |

| East West Banking | 2.9x | 0.7x | 33.90% | ★★★★☆☆ |

| DMCI Holdings | 6.4x | 0.9x | 47.63% | ★★★★☆☆ |

| BCI Minerals | NA | 311.3x | 21.64% | ★★★★☆☆ |

| ReadyTech Holdings | 162.4x | 1.6x | 40.44% | ★★★★☆☆ |

| Chinasoft International | 20.4x | 0.4x | -2587.61% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

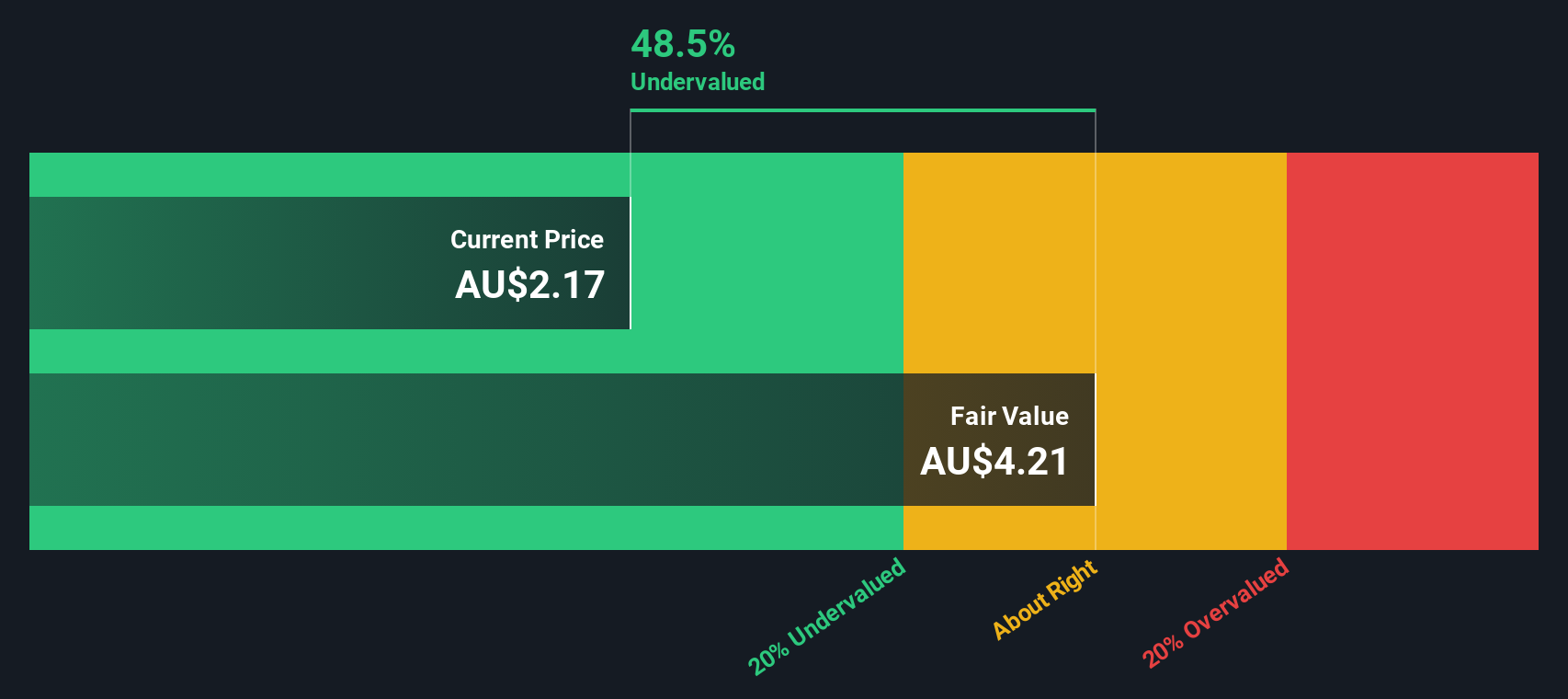

Navigator Global Investments (ASX:NGI)

Simply Wall St Value Rating: ★★★★★★

Overview: Navigator Global Investments is an asset management company primarily operating through its Lighthouse segment, with a market cap of approximately A$0.33 billion.

Operations: Lighthouse is the primary revenue stream, contributing significantly to the company's total income. The gross profit margin has shown variability, with a recent figure of 43.03%. Operating expenses have been a notable component of costs, including general and administrative expenses and non-operating expenses.

PE: 17.9x

Navigator Global Investments, a smaller player in the Asian market, recently filed a follow-on equity offering worth A$145 million. Despite lower profit margins at 34.6% compared to last year, earnings are projected to grow by 38% annually. The company relies entirely on external borrowing for funding, adding risk but also potential upside if managed well. Insider confidence is evident with recent share purchases, suggesting belief in future performance despite current challenges.

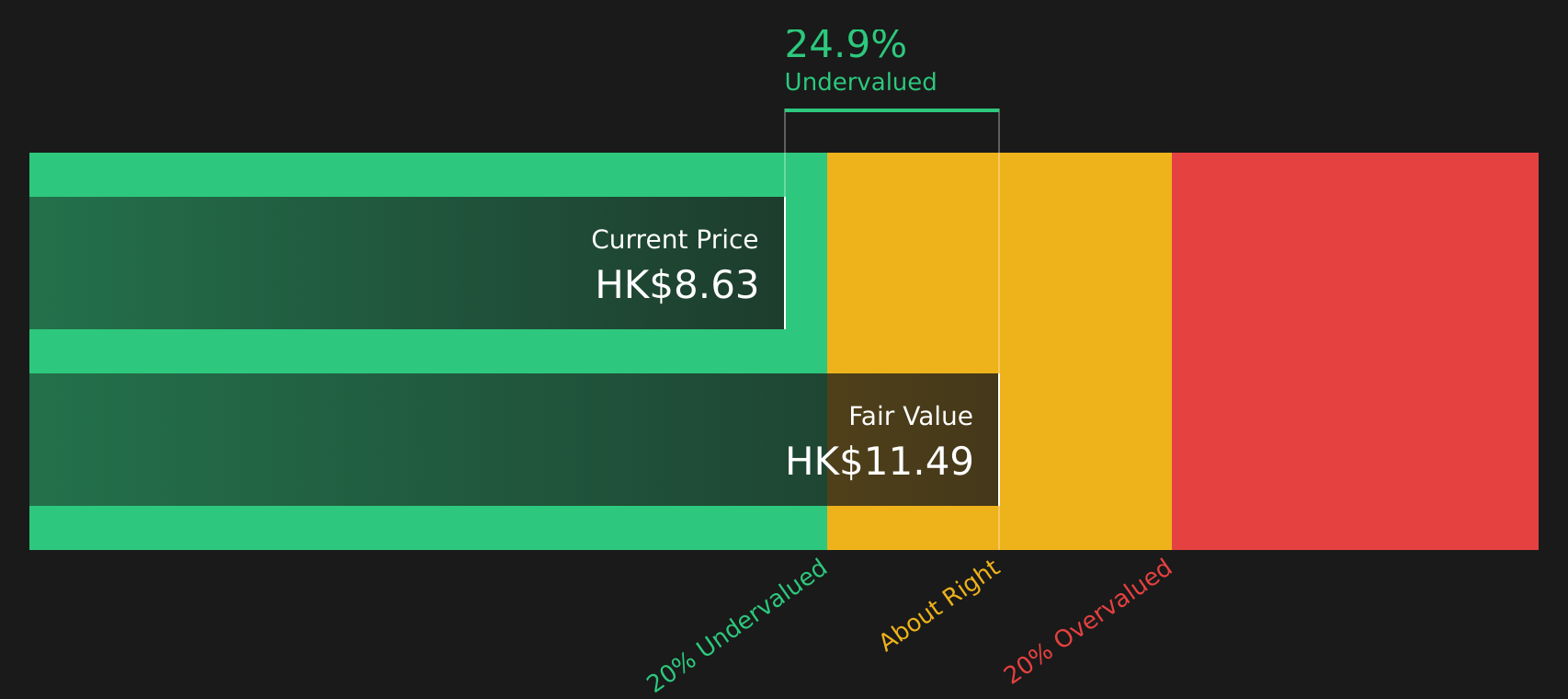

AEON Credit Service (Asia) (SEHK:900)

Simply Wall St Value Rating: ★★★★☆☆

Overview: AEON Credit Service (Asia) operates in the financial services sector, focusing on insurance, credit cards, and personal loans with a market capitalization of HK$5.88 billion.

Operations: The company generates revenue primarily from credit cards and personal loans, with credit cards contributing significantly more. Over time, the gross profit margin has consistently been at 100%, indicating that the cost of goods sold is not impacting the gross profit. Operating expenses are a notable component of costs, with general and administrative expenses being substantial. The net income margin has shown some variation but remains relatively stable around 35% in recent periods.

PE: 7.3x

AEON Credit Service (Asia) has caught attention with its recent earnings boost, reporting a net income of HK$136 million for Q1 2026, up from HK$109 million the previous year. The company benefits from insider confidence as insiders have been purchasing shares over the past few months. Despite relying solely on external borrowing for funding, which carries higher risk, AEON maintains a strategic lease agreement with AEON Stores that supports operational stability. With forecasted earnings growth of 8.75% annually and new board appointments enhancing governance, AEON's future prospects appear promising within its niche market segment in Asia.

- Navigate through the intricacies of AEON Credit Service (Asia) with our comprehensive valuation report here.

Learn about AEON Credit Service (Asia)'s historical performance.

Far East Orchard (SGX:O10)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Far East Orchard is engaged in property investment and development, hospitality operations and management services, as well as student accommodation, with a focus on expanding its real estate footprint across various sectors.

Operations: The company's revenue streams are diversified across hospitality operations, management services, property ownership, and student accommodation. Notably, the gross profit margin has shown a range from 23.16% to 50.58% over recent periods. Operating expenses primarily include general and administrative costs alongside sales and marketing expenditures.

PE: 10.1x

Far East Orchard, a smaller player in the lodging sector, is exploring expansion with a recent move to acquire a site in London for student accommodation. This aligns with their strategy to enhance their UK presence. Despite high-quality earnings, they rely solely on external borrowing, raising risk concerns. Revenue is projected to grow by 9.52% annually; however, earnings might decline by 4.5% over three years. Insider confidence remains evident through recent share purchases earlier this year, indicating potential value recognition within the company’s ranks.

- Click here and access our complete valuation analysis report to understand the dynamics of Far East Orchard.

Gain insights into Far East Orchard's past trends and performance with our Past report.

Key Takeaways

- Gain an insight into the universe of 52 Undervalued Asian Small Caps With Insider Buying by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com