Undiscovered Gems In Asia Highlighting Three Promising Stocks

In recent weeks, Asian markets have experienced mixed performance, with geopolitical tensions and fluctuations in energy prices influencing investor sentiment. Despite these challenges, the region continues to offer potential opportunities for growth, particularly within small-cap stocks that can thrive amid volatility. Identifying a promising stock often involves looking at companies with strong fundamentals and innovative strategies that align well with current market dynamics.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| DeHua TB New Decoration MaterialLtd | 0.63% | 1.50% | 2.14% | ★★★★★★ |

| Nippon Carbide Industries | 16.74% | 1.99% | -4.81% | ★★★★★★ |

| Base | NA | 11.66% | 17.63% | ★★★★★★ |

| Hyundai Home Shopping Network | 6.43% | 16.06% | -2.84% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.31% | 17.83% | 29.70% | ★★★★★☆ |

| Henan Lingrui Pharmaceutical | 7.45% | 9.15% | 18.27% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

| Regina Miracle International (Holdings) | 132.81% | 0.48% | -15.87% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

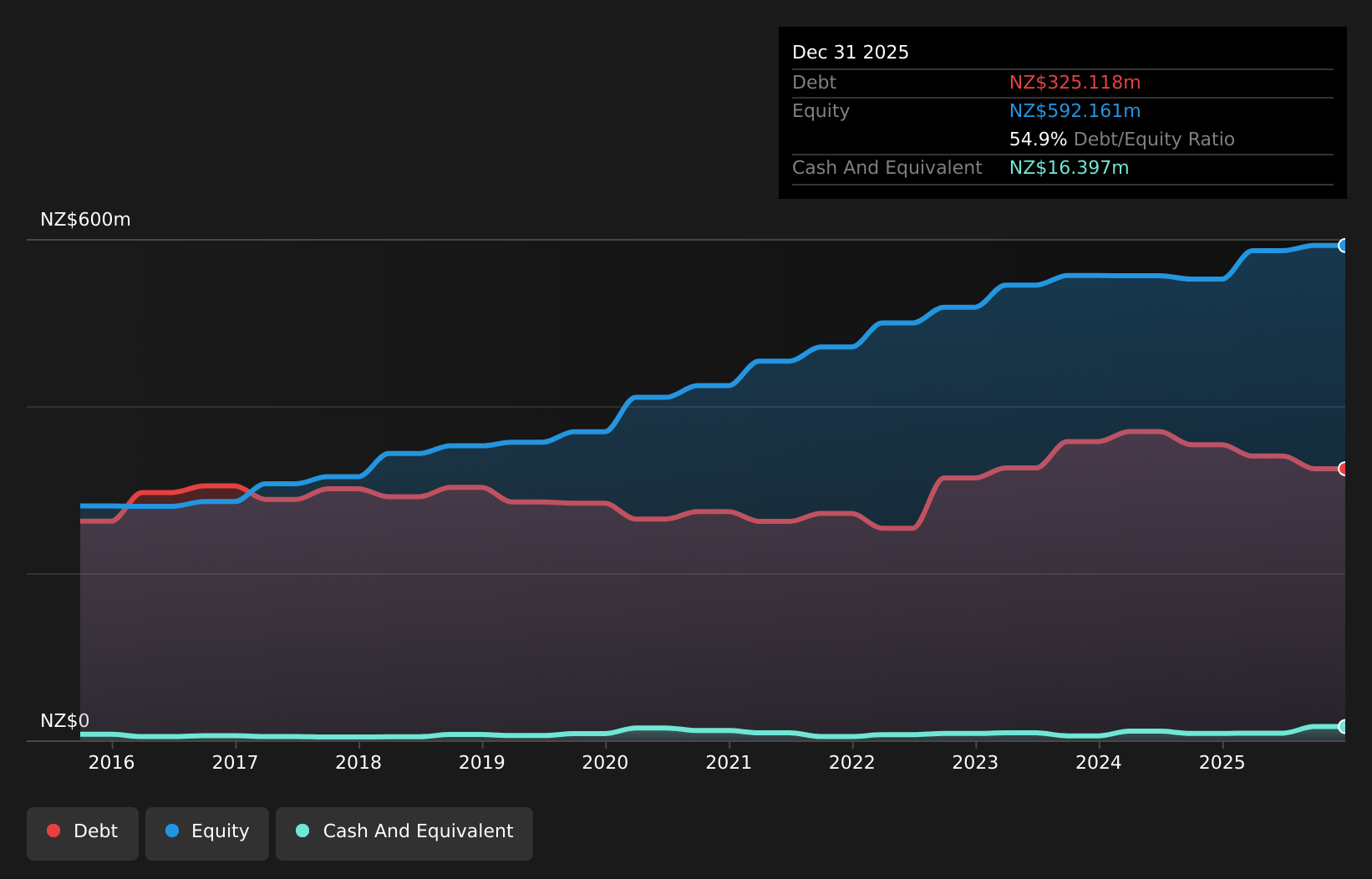

Delegat Group (NZSE:DGL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Delegat Group Limited, with a market cap of approximately NZ$434.86 million, is involved in the production, distribution, and sale of wine through its various subsidiaries.

Operations: Delegat Group generates its revenue primarily through Delegat Limited, contributing NZ$360.60 million, followed by Delegat USA, Inc. with NZ$161.87 million and Delegat Europe Limited at NZ$117.45 million.

Delegat Group, a notable player in the beverage industry, has been making waves with its impressive financial performance. Over the past year, earnings surged by 471%, outpacing the industry's modest 2.4% growth. The company trades at a compelling 38.6% below estimated fair value and maintains high-quality earnings despite a net debt to equity ratio of 52%. Interest payments are well-covered by EBIT at five times coverage. Recent guidance updates project an operating net profit after tax between A$60 million and A$62 million for 2026, buoyed by stronger sales and favorable exchange rates.

- Dive into the specifics of Delegat Group here with our thorough health report.

Review our historical performance report to gain insights into Delegat Group's's past performance.

San Miguel Food and Beverage (PSE:FB)

Simply Wall St Value Rating: ★★★★★★

Overview: San Miguel Food and Beverage, Inc. is involved in the manufacturing and marketing of processed meat products in the Philippines with a market capitalization of approximately ₱284.23 billion.

Operations: San Miguel Food and Beverage generates revenue from three main segments: Food at ₱199.59 billion, Spirits at ₱67.43 billion, and Beer and Non-Alcoholic Beverages at ₱155.18 billion. The company's net profit margin is a key indicator to watch in assessing its financial health and efficiency across these diverse revenue streams.

San Miguel Food and Beverage, a notable player in the food industry, showcases impressive growth with earnings expanding by 11.8% over the past year, outpacing the industry's -4.2%. The company's net income for Q1 2026 rose to PHP 7.84 billion from PHP 7.51 billion a year prior, reflecting robust financial health. Trading at a significant discount of 44.6% below estimated fair value, it's positioned attractively against peers. With a satisfactory net debt to equity ratio of 13.5% and strong interest coverage at 99x EBIT, San Miguel's financials suggest stability and potential for continued growth in earnings per share from PHP 1.33 up from PHP 1.27 last year.

- Unlock comprehensive insights into our analysis of San Miguel Food and Beverage stock in this health report.

Understand San Miguel Food and Beverage's track record by examining our Past report.

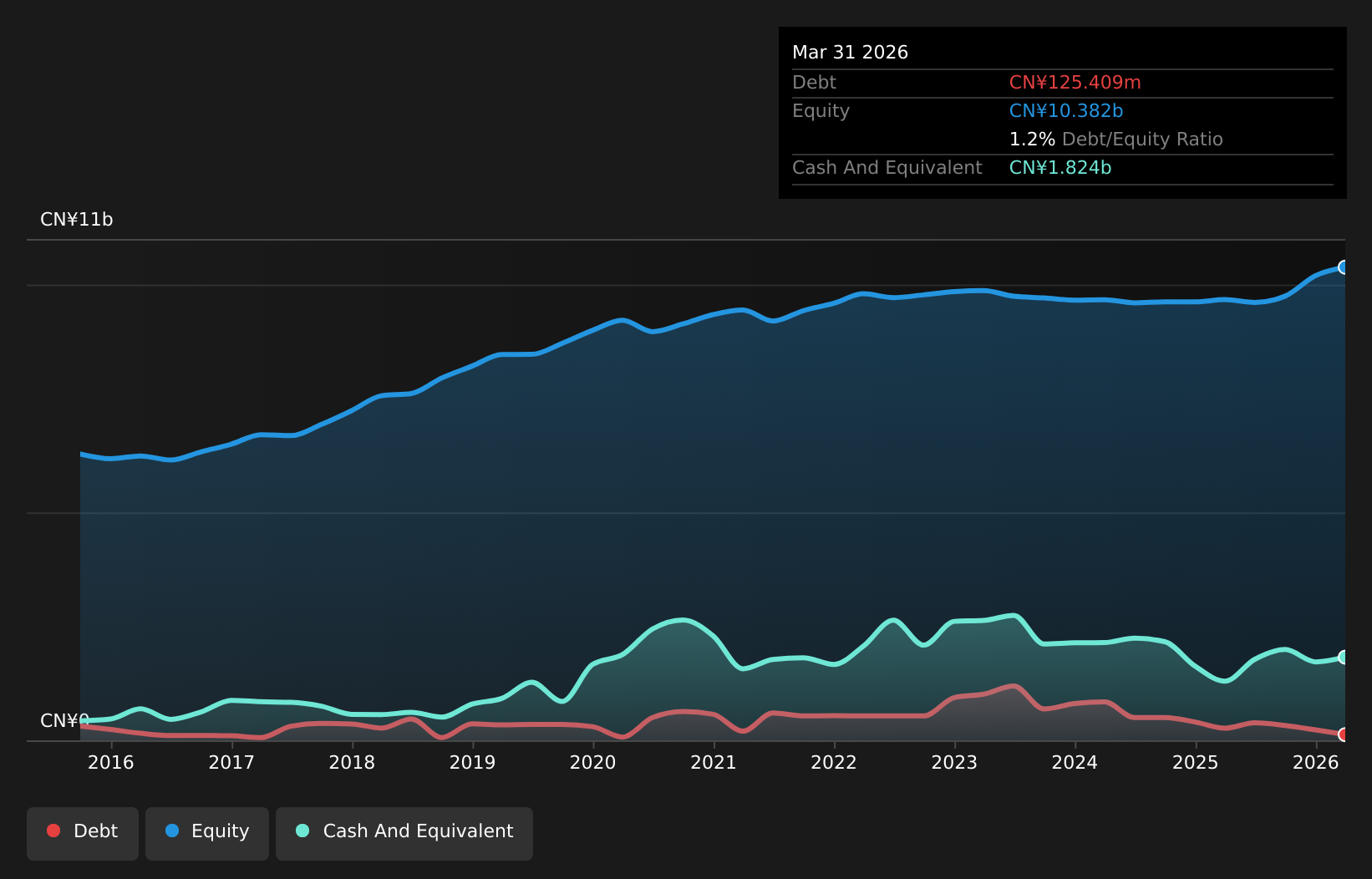

Zhejiang Runtu (SZSE:002440)

Simply Wall St Value Rating: ★★★★★★

Overview: Zhejiang Runtu Co., Ltd. is involved in the production and sale of dyes in China, with a market capitalization of CN¥12.49 billion.

Operations: Zhejiang Runtu generates revenue primarily from its specialty chemical segment, which accounts for CN¥5.76 billion. The company's market capitalization stands at CN¥12.49 billion.

Zhejiang Runtu has been making waves with its impressive earnings growth of 209.8% over the past year, outpacing the Chemicals industry average of 3.7%. Trading at a notable discount, it's valued at 61.9% below its estimated fair value, suggesting potential for investors seeking undervalued opportunities. The company has successfully reduced its debt to equity ratio from 2.1 to 1.2 over five years, indicating improved financial health and stability. Recent results show net income climbing to CNY 669 million from CNY 213 million last year, with basic earnings per share increasing to CNY 0.61 from CNY 0.19 previously, highlighting strong profitability momentum in this small cap stock's performance trajectory.

Seize The Opportunity

- Click here to access our complete index of 108 Asian Undiscovered Gems With Strong Fundamentals.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com