Top ASX Dividend Stocks For July 2026

As Australian shares experience a modest rise, buoyed by strong U.S. bank earnings and easing consumer prices, investors are increasingly optimistic about the Federal Reserve's potential pause on rate hikes. In this climate of cautious optimism and geopolitical tensions, dividend stocks stand out as a reliable choice for those seeking steady income amidst market fluctuations.

Top 10 Dividend Stocks In Australia

| Name | Dividend Yield | Dividend Rating |

| Sugar Terminals (NSX:SUG) | 9.62% | ★★★★★☆ |

| Steadfast Group (ASX:SDF) | 3.81% | ★★★★★☆ |

| Peet (ASX:PPC) | 7.43% | ★★★★★☆ |

| Objective (ASX:OCL) | 3.89% | ★★★★★☆ |

| MFF Capital Investments (ASX:MFF) | 3.85% | ★★★★★☆ |

| Kina Securities (ASX:KSL) | 8.55% | ★★★★★☆ |

| Jumbo Interactive (ASX:JIN) | 7.74% | ★★★★★☆ |

| Fiducian Group (ASX:FID) | 5.91% | ★★★★★☆ |

| EQT Holdings (ASX:EQT) | 6.06% | ★★★★★☆ |

| CTI Logistics (ASX:CLX) | 4.02% | ★★★★☆☆ |

Click here to see the full list of 31 stocks from our Top ASX Dividend Stocks screener.

Let's review some notable picks from our screened stocks.

CSL (ASX:CSL)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: CSL Limited is a global biopharmaceutical company involved in the research, development, manufacture, marketing, and distribution of products and vaccines across several countries including Australia and the United States, with a market cap of A$58.31 billion.

Operations: CSL Limited's revenue is primarily derived from three segments: CSL Behring (including CSL Intellectual Property) at $10.87 billion, CSL Vifor at $2.39 billion, and CSL Seqirus at $2.15 billion.

Dividend Yield: 3.4%

CSL's dividends have been stable and growing over the past decade, though its current yield of 3.43% is low compared to the top 25% of Australian dividend payers. The dividend is not well covered by earnings due to a high payout ratio, but it is supported by cash flows with a reasonable cash payout ratio of 56.3%. Recent leadership changes may impact strategic direction, with new appointments in key positions as CSL navigates revenue challenges.

- Dive into the specifics of CSL here with our thorough dividend report.

- Upon reviewing our latest valuation report, CSL's share price might be too pessimistic.

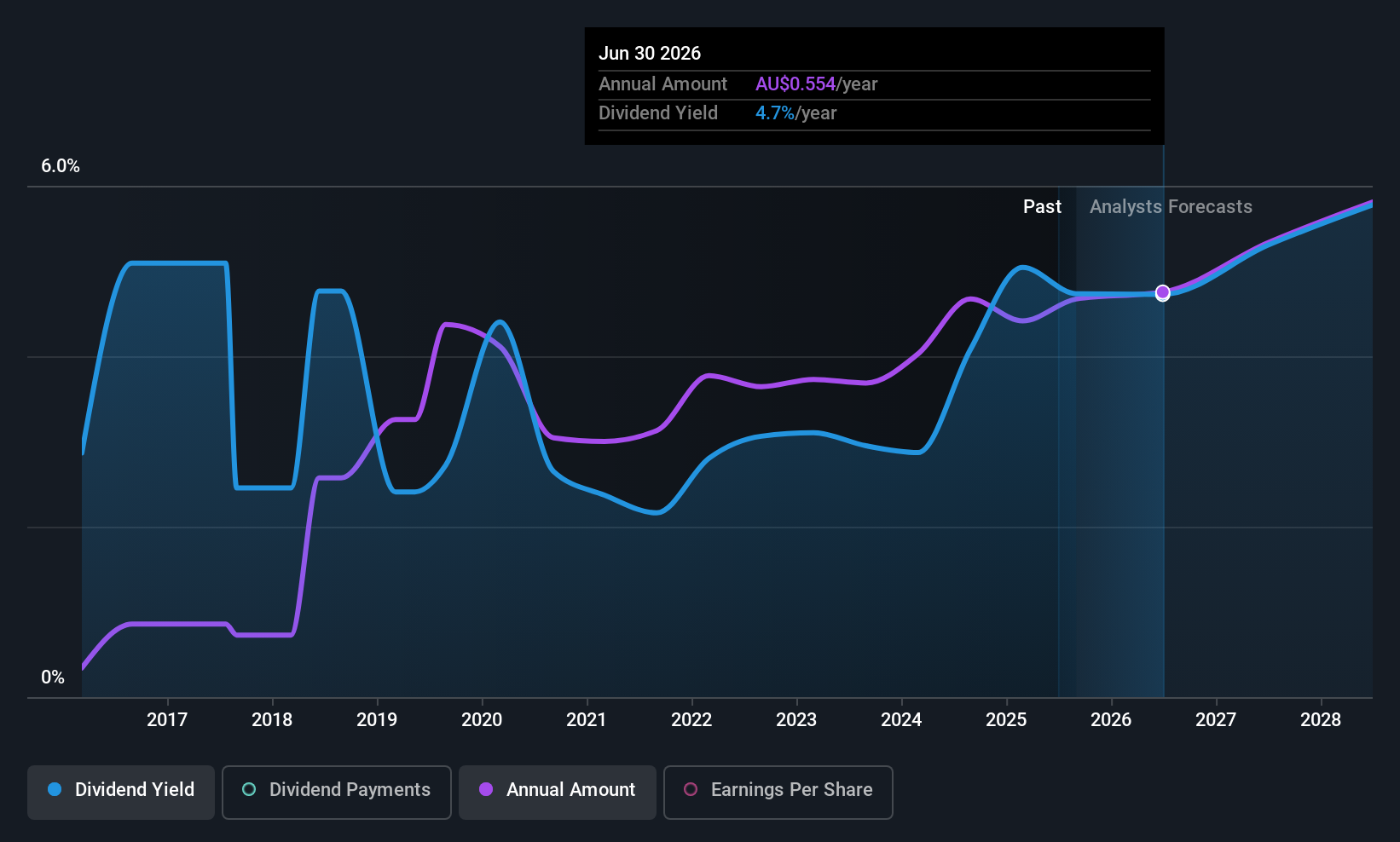

Jumbo Interactive (ASX:JIN)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Jumbo Interactive Limited operates as an online and mobile retailer of lottery tickets across Australia, the United Kingdom, Canada, Fiji, and internationally with a market cap of A$446 million.

Operations: Jumbo Interactive Limited's revenue segments include Managed Services at A$28.86 million, Lottery Retailing at A$110.74 million, and Software-As-A-Service (SaaS) at A$44.67 million.

Dividend Yield: 7.7%

Jumbo Interactive's dividend yield of 7.74% is among the top 25% in Australia, supported by a payout ratio of 70.4% and a cash payout ratio of 69.1%. Despite this coverage, its dividend history has been volatile over the past decade with notable drops exceeding 20%. Trading at A$73.2 million below estimated fair value, Jumbo offers potential value, though its dividends have shown unreliability in consistency and growth stability.

- Get an in-depth perspective on Jumbo Interactive's performance by reading our dividend report here.

- The valuation report we've compiled suggests that Jumbo Interactive's current price could be quite moderate.

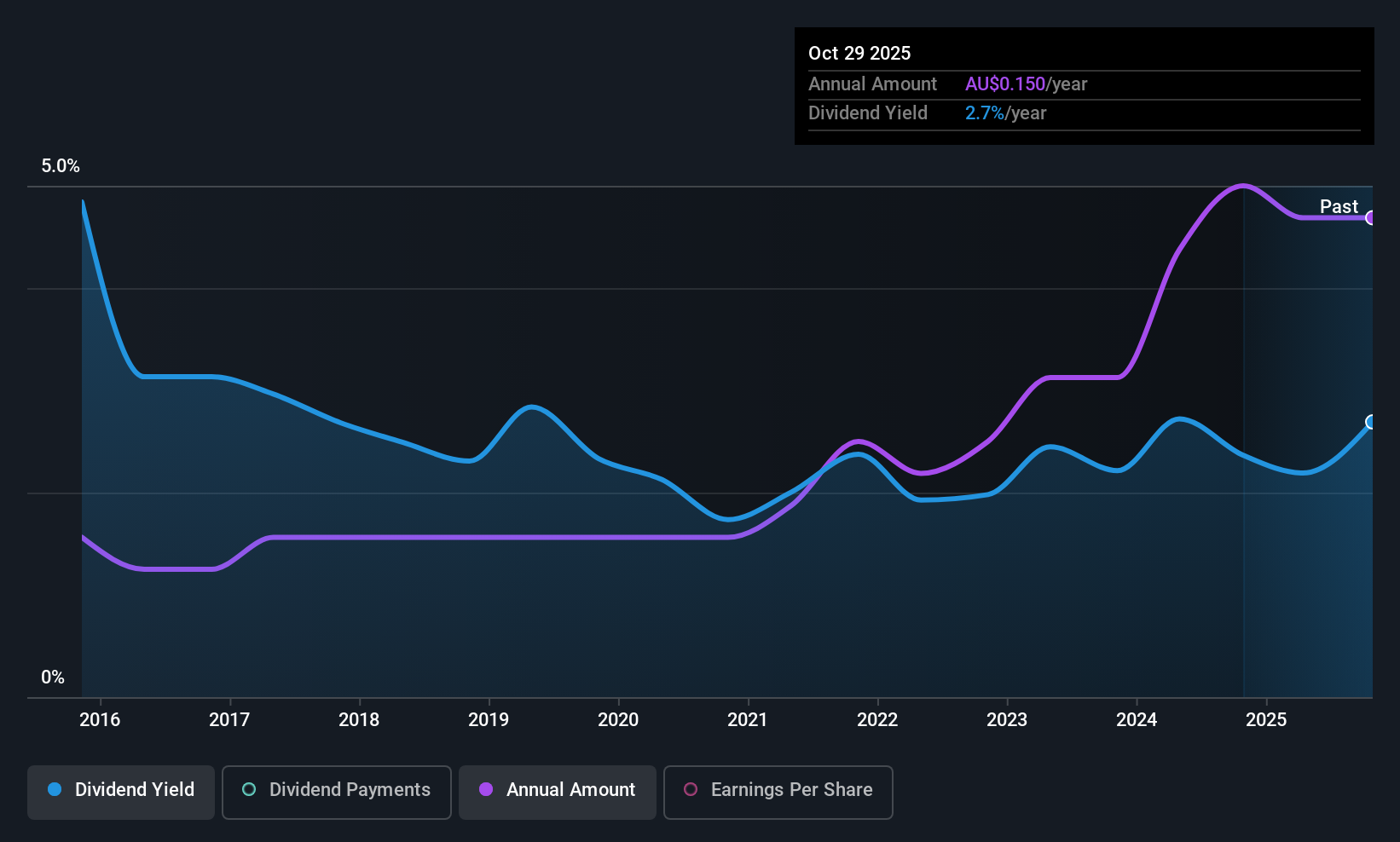

Waterco (ASX:WAT)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Waterco Limited manufactures, wholesales, and exports equipment and accessories for swimming pools, spa pools, spa baths, rural pumps, irrigation, and water treatment sectors across Australia, New Zealand, Asia, North America, and Europe with a market cap of A$175.22 million.

Operations: Waterco Limited's revenue from its Building Products segment amounts to A$253.41 million.

Dividend Yield: 3%

Waterco's dividend yield of 3% is modest compared to top Australian payers, with a payout ratio of 50.5% indicating earnings coverage and a cash payout ratio of 30.8% ensuring cash flow support. Despite this, its dividends have been volatile over the past decade with significant annual drops. Recent share buyback plans may influence future distributions, but historical instability in payments suggests caution for those seeking reliable income growth from dividends.

- Click here to discover the nuances of Waterco with our detailed analytical dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Waterco shares in the market.

Where To Now?

- Navigate through the entire inventory of 31 Top ASX Dividend Stocks here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com