ASX Stocks Estimated To Be Trading Below Intrinsic Value In July 2026

The Australian stock market is experiencing a modest uptick, buoyed by positive developments in U.S. bank earnings and easing consumer prices, with the ASX poised for a 50-point advance. In this environment of cautious optimism and geopolitical tensions, identifying stocks trading below their intrinsic value can offer potential opportunities for investors seeking to capitalize on undervaluation amidst fluctuating economic conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Xero (ASX:XRO) | A$68.27 | A$133.95 | 49% |

| Symal Group (ASX:SYL) | A$2.80 | A$5.53 | 49.4% |

| Superloop (ASX:SLC) | A$3.10 | A$5.59 | 44.5% |

| PolyNovo (ASX:PNV) | A$1.00 | A$1.87 | 46.4% |

| NRW Holdings (ASX:NWH) | A$7.02 | A$13.63 | 48.5% |

| Navigator Global Investments (ASX:NGI) | A$2.42 | A$4.62 | 47.6% |

| Magellan Financial Group (ASX:MFG) | A$9.77 | A$17.13 | 43% |

| Kogan.com (ASX:KGN) | A$4.19 | A$7.41 | 43.4% |

| Frontier Digital Ventures (ASX:FDV) | A$0.35 | A$0.62 | 43.7% |

| Betr Entertainment (ASX:BBT) | A$0.175 | A$0.34 | 48.4% |

Let's explore several standout options from the results in the screener.

NRW Holdings (ASX:NWH)

Overview: NRW Holdings Limited offers diversified contract services to the resources and infrastructure sectors in Australia, with a market cap of A$3.23 billion.

Operations: NRW Holdings Limited's revenue segments include MET at A$1.08 billion, Civil at A$850.05 million, and Mining at A$1.50 billion.

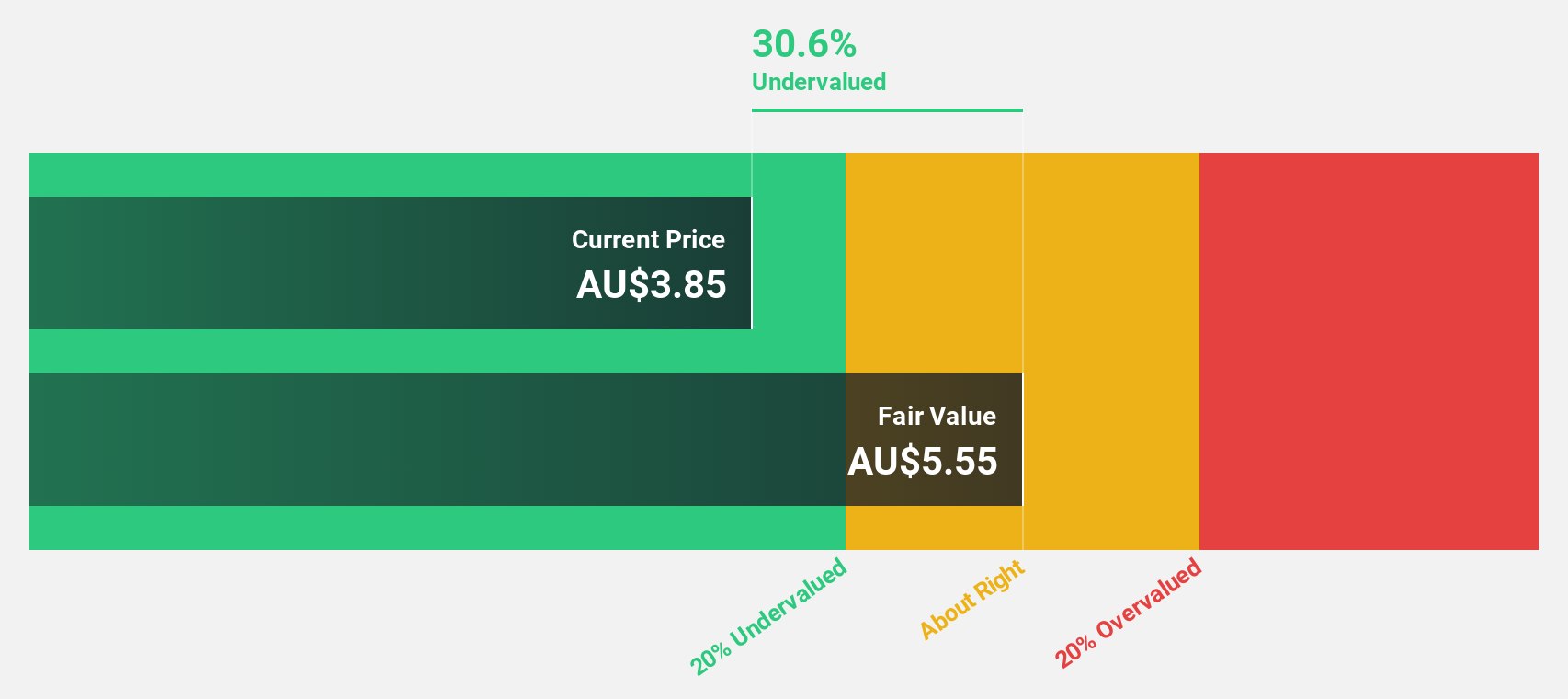

Estimated Discount To Fair Value: 48.5%

NRW Holdings is trading at A$7.02, significantly below its estimated future cash flow value of A$13.63, indicating potential undervaluation based on cash flows. Despite a drop in net profit margin from 3.7% to 1.4%, the company is forecasted to achieve substantial earnings growth of 23.44% per year over the next three years, outpacing the Australian market's expected growth rate of 11.4%. Revenue is also projected to grow at 7.4% annually, surpassing market expectations.

- Insights from our recent growth report point to a promising forecast for NRW Holdings' business outlook.

- Get an in-depth perspective on NRW Holdings' balance sheet by reading our health report here.

Southern Cross Electrical Engineering (ASX:SXE)

Overview: Southern Cross Electrical Engineering Limited, with a market cap of A$1.28 billion, offers electrical, instrumentation, communications, security, fire, and maintenance services and products across Australia.

Operations: The company generates revenue primarily from its Electrical, Security and Communication Services segment, which accounts for A$691.18 million.

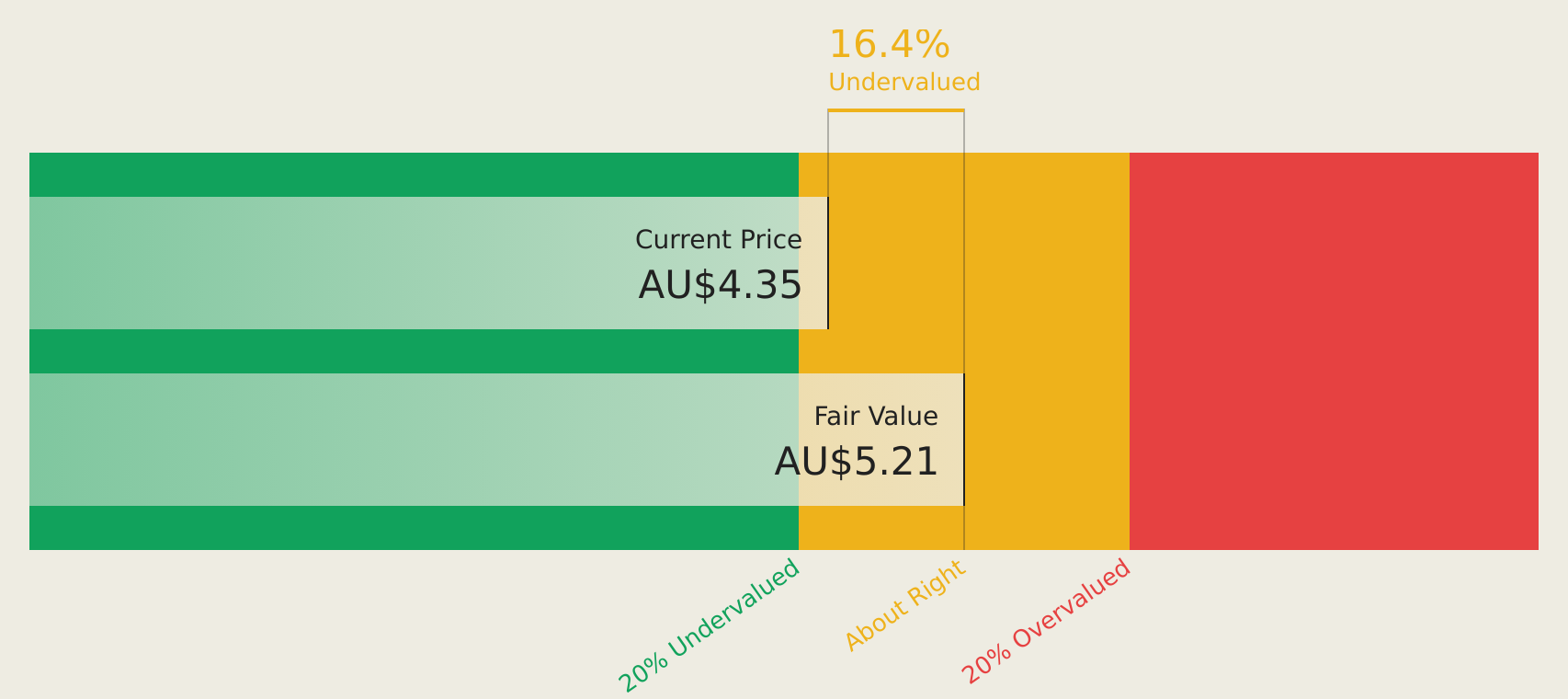

Estimated Discount To Fair Value: 19.7%

Southern Cross Electrical Engineering, with shares at A$4.8, trades below its estimated future cash flow value of A$5.98, presenting potential undervaluation based on cash flows. Despite a recent dip in net profit margin from 4.1% to 0.4%, earnings are forecasted for significant growth at 80.9% annually over the next three years, surpassing market averages. Recent follow-on equity offerings totaling A$165 million may impact financial stability and investor sentiment moving forward.

- Our expertly prepared growth report on Southern Cross Electrical Engineering implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of Southern Cross Electrical Engineering here with our thorough financial health report.

Symal Group (ASX:SYL)

Overview: Symal Group Limited operates in the civil construction industry in Australia, offering services such as construction contracting, equipment hires, material sales, recycling, and remediation, with a market cap of A$669.60 million.

Operations: The company's revenue segments consist of A$801.43 million from contracting services and A$187.79 million from plant and equipment.

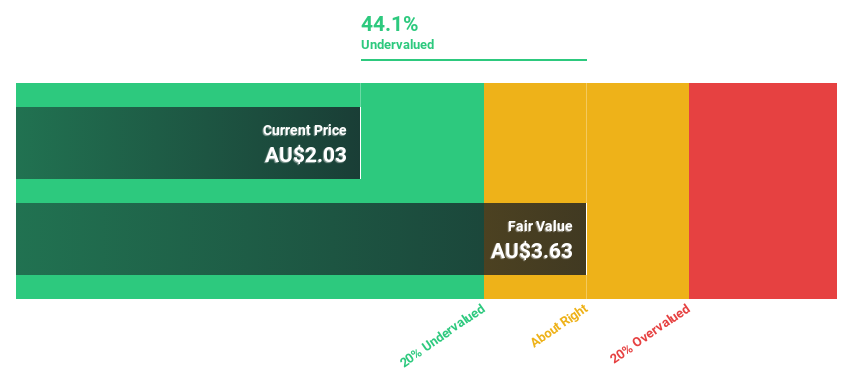

Estimated Discount To Fair Value: 49.4%

Symal Group, trading at A$2.8, is significantly undervalued based on discounted cash flow analysis with an estimated value of A$5.53. Earnings grew by 90.4% last year and are forecast to increase by 14.2% annually, outpacing the Australian market average growth rate of 11.4%. Recent executive changes include appointing Scott McQueen as CFO, who brings extensive financial expertise to support Symal's strategic growth initiatives and enhance long-term value creation for shareholders.

- The growth report we've compiled suggests that Symal Group's future prospects could be on the up.

- Take a closer look at Symal Group's balance sheet health here in our report.

Summing It All Up

- Dive into all 39 of the Undervalued ASX Stocks Based On Cash Flows we have identified here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com