3 Japanese Industrial Stocks With 50% Earnings Growth Flying Under The Radar

With inflation signals mixed across regions, central banks weighing their next move and energy prices swinging with every geopolitical headline, investors are looking for high quality growth stories that are not already crowded by big institutions. That is where the High-Quality Undiscovered Gems screener comes in. It targets smaller companies with solid fundamentals that many large funds have yet to notice. In this article, you will see three of the most compelling stocks from this screener, and how they may help you turn Wall Street’s blind spot into a differentiated, long term addition to your portfolio.

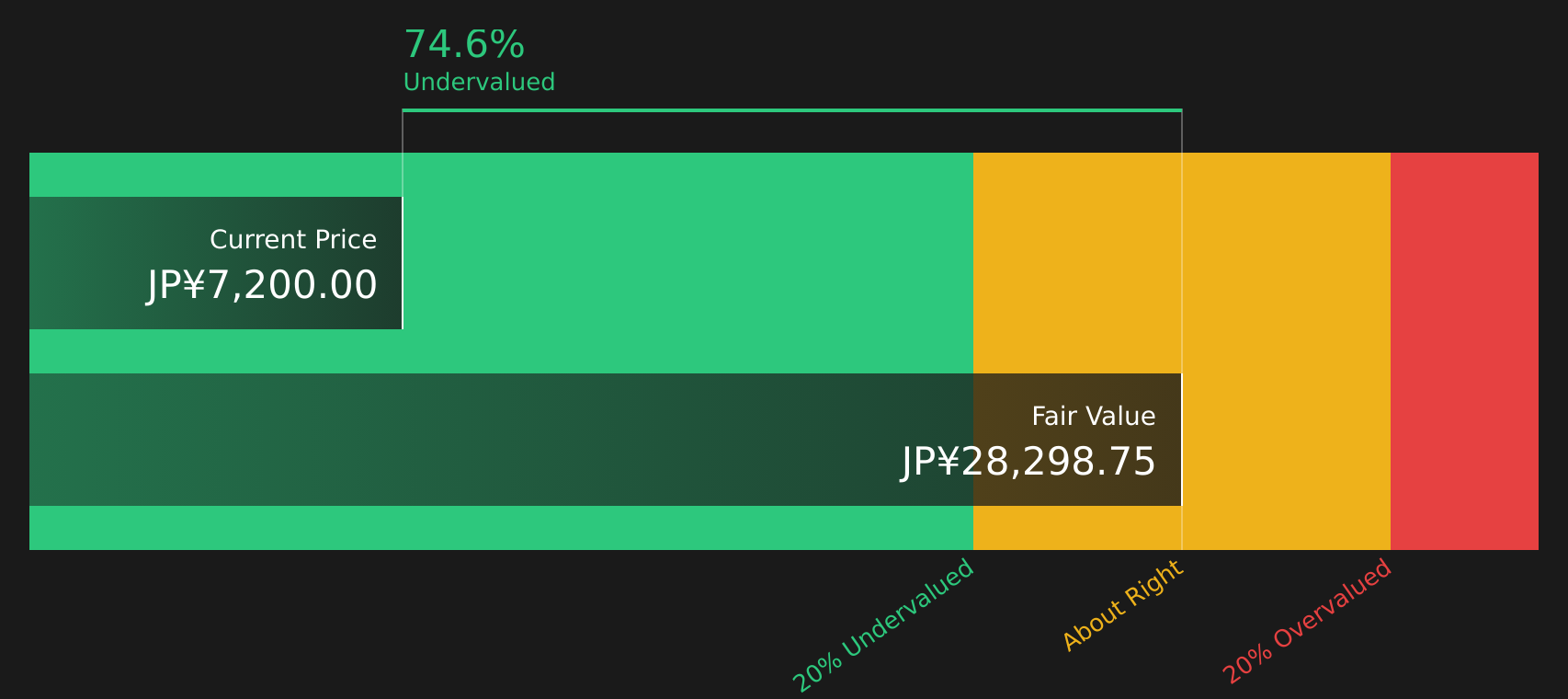

Tsugami (TSE:6101)

Overview: Tsugami is a Tokyo based manufacturer of high precision machine tools, such as CNC automatic lathes, machining centers and grinding machines, used by electronics, telecom and automotive customers across Japan and a wide range of overseas markets.

Operations: Tsugami generates most of its revenue from China at ¥111,039 million, with Japan contributing ¥27,704 million and India ¥6,848 million, alongside smaller amounts from South Korea and other regions, partly offset by a ¥19,043 million unallocated adjustment.

Market Cap: ¥344b

Tsugami stands out in this screener because it combines high quality earnings with meaningful scale in precision manufacturing, yet still looks underappreciated by the market. Earnings grew 53.6% in the past year, return on equity is a strong 22.8%, and net margin is 13%, which supports the case for a solid underlying business. At the same time, the stock has traded well below an estimate of its future cash flow value and has a higher than average P/E for the Machinery sector, which suggests that investors are still debating how to price its growth. In addition, the presence of a share buyback program, rising dividend guidance and some funding structure risks makes Tsugami a company that may merit closer attention.

Tsugami’s 53.6% earnings growth, 22.8% ROE and 13% margin suggest that the market may not have fully priced in the strength of the business. See how the 2 key rewards and 1 important major warning sign might reframe the whole story.

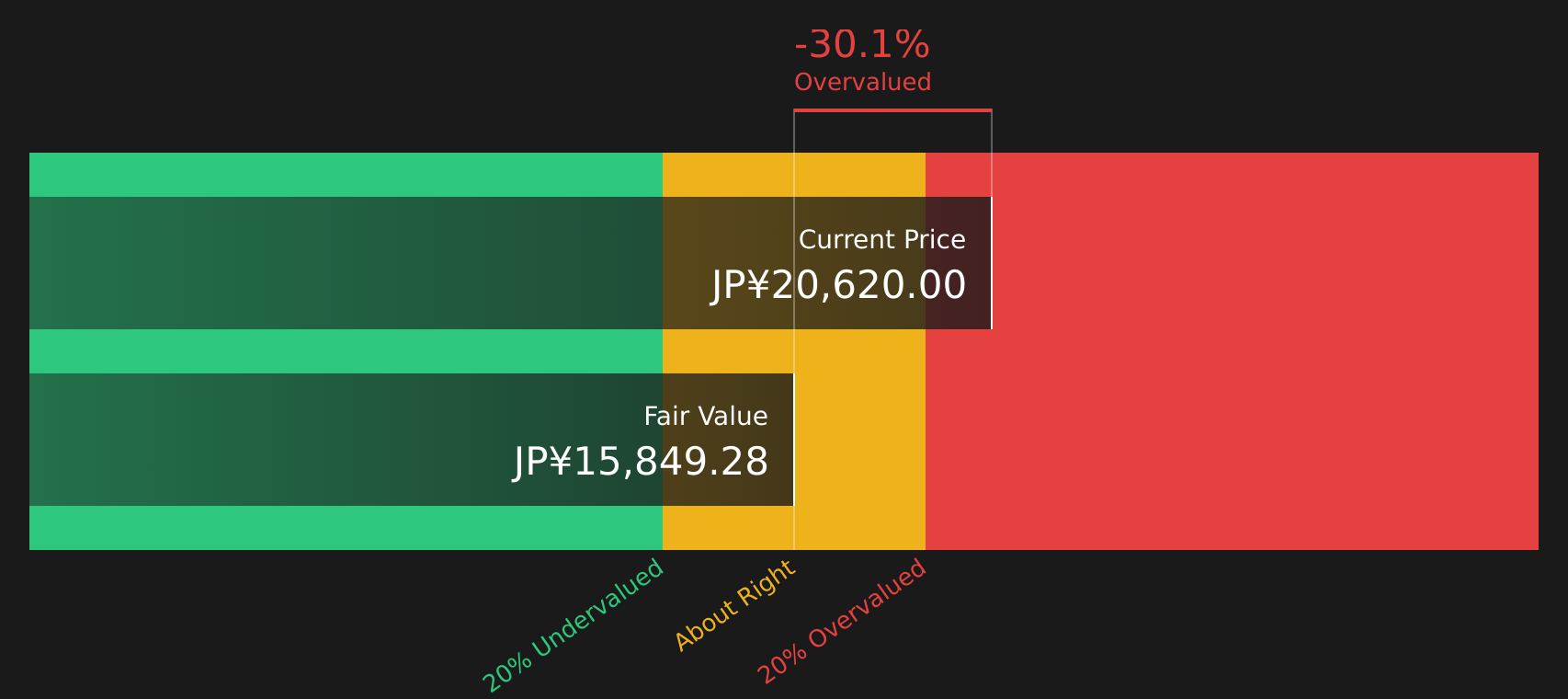

santec Holdings (TSE:6777)

Overview: santec Holdings is a Komaki based specialist in optical technology, supplying tunable lasers, filters, measurement instruments and imaging systems that help telecom networks, electronics makers and medical device companies test, monitor and analyze light based signals and components.

Market Cap: ¥247.0b

santec Holdings may interest you if you are looking for a smaller optical technology specialist with strong profitability and recent earnings growth of 51.3% over the past year, a 24.3% net margin and an ROE of 27.5%. That strength comes with trade offs, including a 33.4x P/E, a share price above an estimate of its future cash flow value and highly volatile trading. In addition, the balance sheet is fully funded by higher risk external borrowing and the management team is relatively new, while the broader board has long experience and recent refreshment. Together, these factors present santec as a high quality but finely balanced growth story that may warrant deeper research.

santec’s 51.3% earnings growth, 24.3% net margin and 27.5% ROE are hard to ignore, yet a 33.4x P/E and fully debt funded balance sheet raise sharp questions. Start with the 2 key rewards and 1 important major warning sign

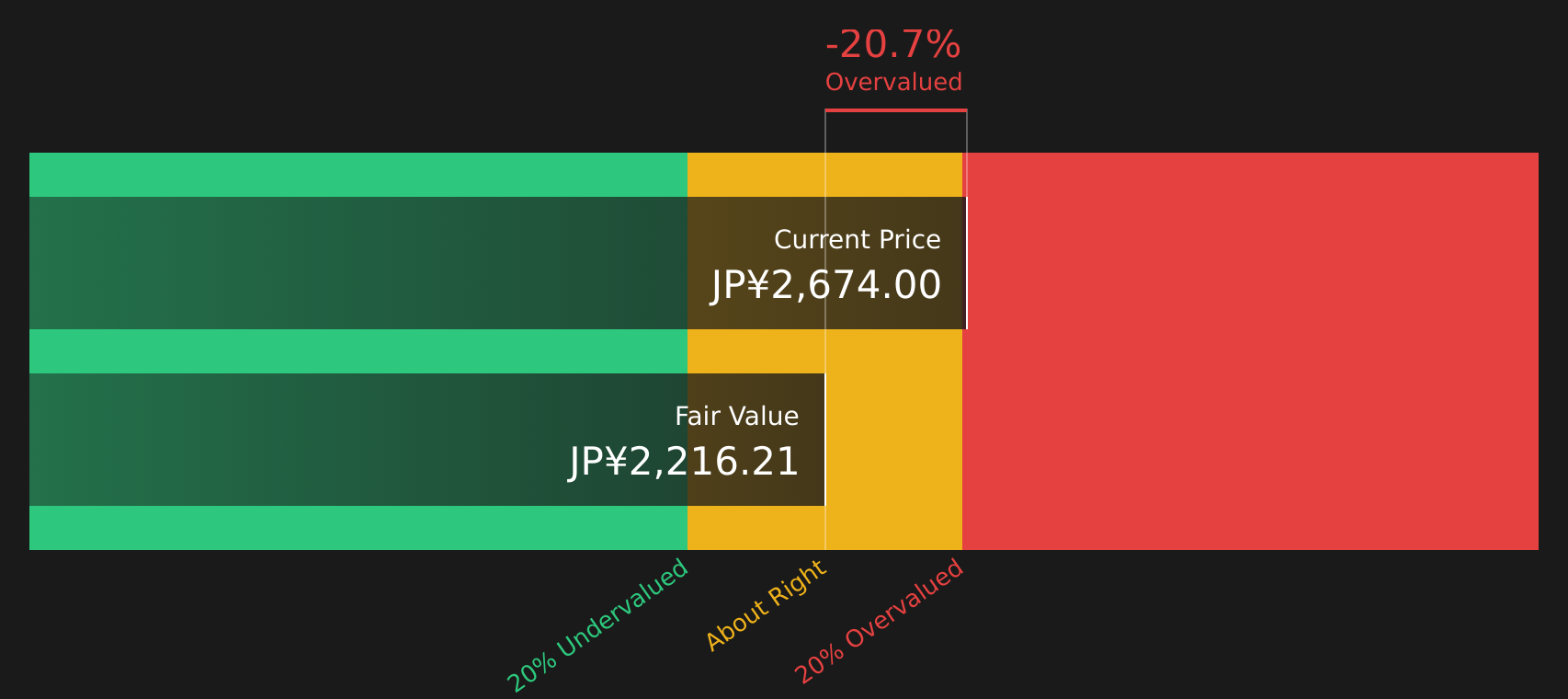

Dai-Dan (TSE:1980)

Overview: Dai-Dan is an Osaka based engineering contractor that designs and builds complex electrical, air conditioning, water hygiene and firefighting systems for buildings, while also supplying specialized solutions for hospitals, laboratories, clean rooms and energy efficient facilities across Japan.

Market Cap: ¥345.1b

Dai-Dan catches the eye because it combines 53.5% earnings growth, a 10.4% net margin and a high 20.3% ROE with a P/E that sits below both the broader Japanese market and an estimated fair multiple. However, the shares still trade above an estimate of future cash flows, which signals that opinion on value is split. Revenue and earnings growth over the past five years, plus raised guidance and a higher dividend outlook, point to a business that has been executing well on large construction projects. At the same time, a volatile share price, a funding structure that relies entirely on external borrowing and a relatively new, less experienced board introduce governance and balance sheet questions that investors may wish to understand before deciding how Dai-Dan fits into their own watchlist.

Dai-Dan’s strong 53.5% earnings growth and 20.3% ROE, along with a lower P/E than the wider market, hint that something in this story is mispriced, and the 3 key rewards and 2 important warning signs could reveal what investors are overlooking

The three stocks covered here are only a starting point, as the full High-Quality Undiscovered Gems screen on Simply Wall St surfaced 55 more companies with similarly strong fundamentals and underfollowed stories through the High-Quality Undiscovered Gems screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you. This can help you focus on the highest conviction opportunities that fit your own approach.

Take Control of Your Investment Journey

If Dai-Dan or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas do not stay under the radar for long, and the best setups can shift from breakout to overcooked fast. Scan these curated picks now and consider them early.

- Target dependable cash flows and resilience by reviewing a curated 43 dividend fortresses designed for investors who want income potential without ignoring balance sheet strength.

- Spot under-the-radar opportunities in the energy transition by scanning a focused group of 89 nuclear energy infrastructure stocks that could be positioned to benefit if infrastructure momentum builds.

- Explore the technology backbone of AI by assessing carefully selected 52 AI infrastructure stocks supporting data centers, chips and power systems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com