BAE Systems Stock And 2 UK Cash Flow Picks Trading Below Fair Value

With inflation trends mixed across regions, energy prices swinging on geopolitics, and central banks rethinking their next moves, many investors are looking for stocks where the cash flow story and the market price do not fully match. The Undervalued Stocks Based On Cash Flows screener focuses on companies that SWS DCF valuation flags as trading below fair value, with cash flow potential front and center. That can appeal to investors who prioritize what a business can earn rather than short term sentiment. In this article you will see 3 stocks from this screener that currently stand out.

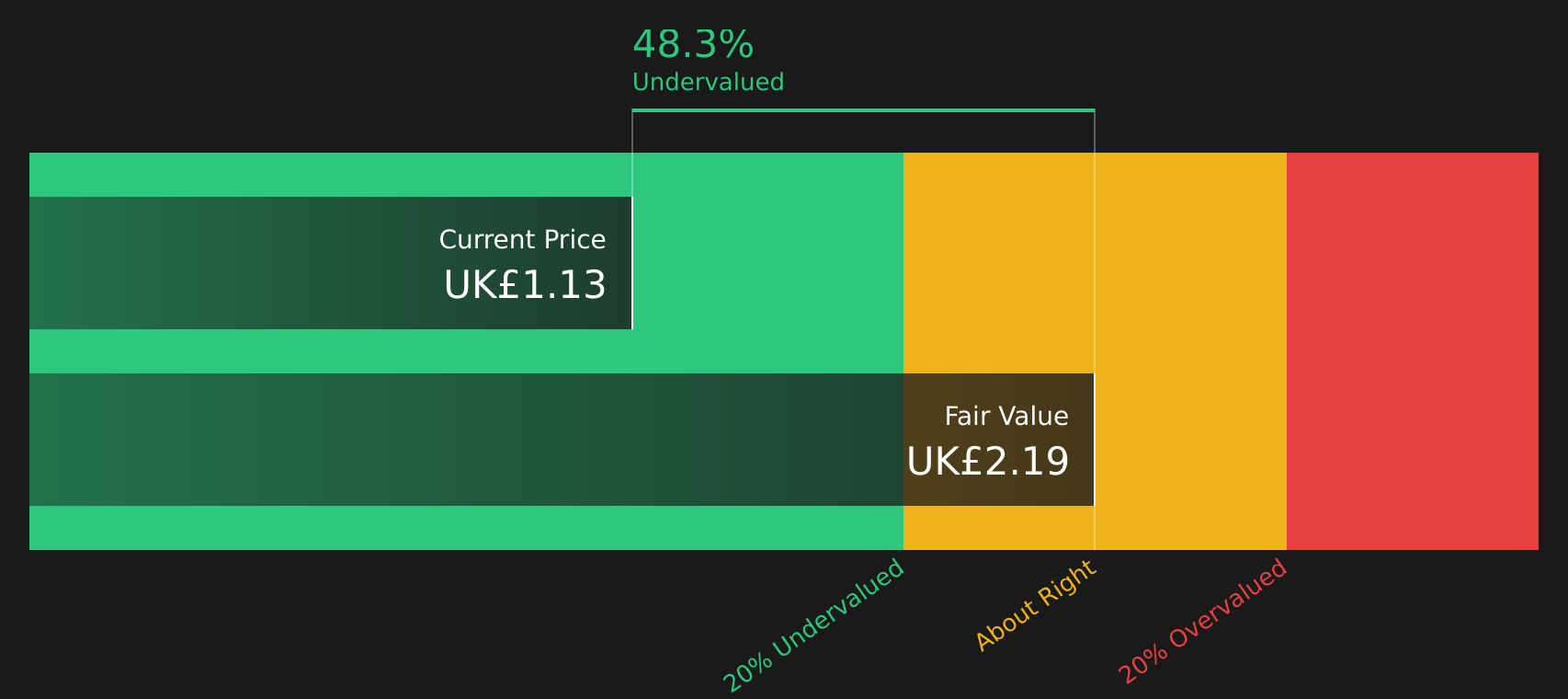

Eurocell (LSE:ECEL)

Overview: Eurocell is a UK based manufacturer and distributor of PVC and related building products, supplying windows, doors, roofline, cladding, roofing, and outdoor living materials to trade installers, builders, and homeowners, with an in house recycling operation that feeds back into its product range.

Operations: Eurocell generates most of its revenue from Building Plastics (£210.5m) and Profiles (£208.2m), with Alunet contributing £46.7m and inter segment revenue of £61.9m, largely in the United Kingdom (£401.3m) and a small contribution from the Republic of Ireland (£2.2m).

Market Cap: £108.5m

Eurocell appears in this cash flow focused screener because it combines a broad building products footprint with earnings that analysts expect to grow strongly. The stock trades on a P/E below sector averages and below Simply Wall St’s DCF estimate of fair value. The Alunet acquisition, branch expansion and ERP upgrade are all aimed at improving efficiency and widening the product set, but they come with execution risk, cost inflation pressure and exposure to weak consumer confidence in repair, maintenance and improvement markets. Investors also need to weigh an unstable dividend record and external borrowing against management and board experience and a new CFO hire that could sharpen capital allocation and financial discipline.

Eurocell’s earnings story, valuation gap and execution risks are all pulling in different directions, and the missing piece is how those cash flows really stack up against expectations, so it is worth reviewing the analyst forecasts for Eurocell to see what might be hiding behind the headline outlook.

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is an asset manager that focuses on infrastructure, private equity, venture capital and listed funds, giving investors exposure to renewable energy projects, social and digital infrastructure, and smaller growth companies across the UK, Europe and Australia. It raises and manages capital for both institutional and retail clients, typically taking meaningful stakes in businesses and real assets.

Operations: Foresight Group Holdings generates most of its revenue from Real Assets (£114.8m) and Private Equity (£50.1m), with the United Kingdom contributing £126.4m and Australia £25.7m, alongside smaller revenues from several European markets and Luxembourg.

Market Cap: £508.6m

Foresight Group Holdings stands out on this cash flow focused screen because it combines profitability with an asset base that analysts see as only partly tapped, particularly in renewable energy and infrastructure where market share is still low. Revenue and earnings are forecast to grow, margins are already high, and the company is returning capital through ongoing share buybacks while also investing in higher fee products. At the same time, reliance on performance fees, concentrated exposure to UK and European policy around green energy, and funding entirely from external borrowing mean earnings can be sensitive if fundraising or returns slow. For investors who want to understand how those growth ambitions, risks and buybacks fit together, the current set up at Foresight Group Holdings raises some important questions.

Foresight Group Holdings has accelerating ambitions in renewables, infrastructure and higher fee products, yet the full picture of its earnings power is easy to underestimate, so it is worth reviewing the analyst forecasts for Foresight Group Holdings to see what might be quietly reshaping the story.

BAE Systems (LSE:BA.)

Overview: BAE Systems is a global defense, aerospace, and security company that supplies everything from fighter jets, submarines, and combat vehicles to electronic warfare systems, munitions, and cyber security services for governments and armed forces around the world.

Operations: BAE Systems generates revenue across Electronic Systems (£7.5b), Air (£7.4b), Maritime (£6.6b), Platforms & Services (£5.0b), and Cyber & Intelligence (£2.4b), with intra group revenue of £0.6b.

Market Cap: £52.5b

BAE Systems catches the eye in a cash flow focused screen because it combines a £75b order backlog and exposure to areas like drones, munitions, electronic warfare, and space systems with earnings that analysts expect to grow faster than the wider UK market. Recent contracts across the US Army, Space Force, and allied air forces show how its technology is embedded in long term programs. However, there are real questions around dependence on large government contracts, ESG pushback, and supply chain and capacity bottlenecks that could slow the conversion of that backlog into cash. For investors, the tension between growth expectations, valuation, and these risks is exactly where the opportunity or the disappointment is likely to sit.

BAE Systems’ swelling order book and cash generation potential could be masking a very different earnings path than headlines suggest, so it is worth reviewing the analyst forecasts for BAE Systems to see what the backlog might really be signaling.

These three stocks are just the starting point. The full Undervalued Stocks Based On Cash Flows screen surfaces 33 more companies where discounted cash flow and current pricing point to equally compelling stories in the Undervalued Stocks Based On Cash Flows screener. Use Simply Wall St to identify and analyze the specific cash flow catalysts, valuation gaps and risk factors that matter most to you, so you can focus on the highest conviction opportunities in this group.

Take Control of Your Investment Journey

If Eurocell or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Today?

Some of the sharpest breakouts start quietly while attention sits elsewhere. By the time momentum is flying, the best entry points can be difficult to find, so consider acting early.

- Spot strong income ideas before yields start dropping by reviewing the hand picked group of companies in the 3 dividend fortresses.

- Target high conviction growth stories with solid balance sheets by scanning the curated 10 high quality undiscovered gems that are under the radar for now.

- Position ahead of potential infrastructure momentum by checking the focused shortlist of 34 power grid technology and infrastructure stocks that could be pivotal while it still matters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com