European Value Stock Picks For July 2026

As geopolitical tensions and energy market volatility weigh on European equities, the pan-European STOXX Europe 600 Index recently saw a decline of 1.79%. In this environment, investors are increasingly seeking undervalued stocks that may offer potential for growth as markets adjust to these economic pressures. Identifying such stocks involves looking for companies with strong fundamentals that may be temporarily overlooked by the market due to broader economic uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Troax Group (OM:TROAX) | SEK96.90 | SEK188.97 | 48.7% |

| New Wave Group (OM:NEWA B) | SEK92.65 | SEK180.13 | 48.6% |

| Murapol (WSE:MUR) | PLN37.95 | PLN75.68 | 49.9% |

| Micro Systemation (OM:MSAB B) | SEK83.00 | SEK160.39 | 48.3% |

| Jerónimo Martins SGPS (ENXTLS:JMT) | €16.44 | €31.80 | 48.3% |

| Gabriel Holding (CPSE:GABR) | DKK268.00 | DKK517.93 | 48.3% |

| Execus (BIT:EXEC) | €1.05 | €2.07 | 49.4% |

| Casta Diva Group (BIT:CDG) | €3.06 | €6.03 | 49.3% |

| BHG Group (OM:BHG) | SEK22.06 | SEK42.53 | 48.1% |

| AKVA group (OB:AKVA) | NOK126.50 | NOK243.39 | 48% |

We're going to check out a few of the best picks from our screener tool.

Acerinox (BME:ACX)

Overview: Acerinox, S.A., along with its subsidiaries, manufactures and distributes stainless steel and high-performance alloys globally, with a market cap of €4.11 billion.

Operations: The company generates revenue from two primary segments: €4.06 billion from its Stainless Steel Business and €1.62 billion from High Performance Alloys.

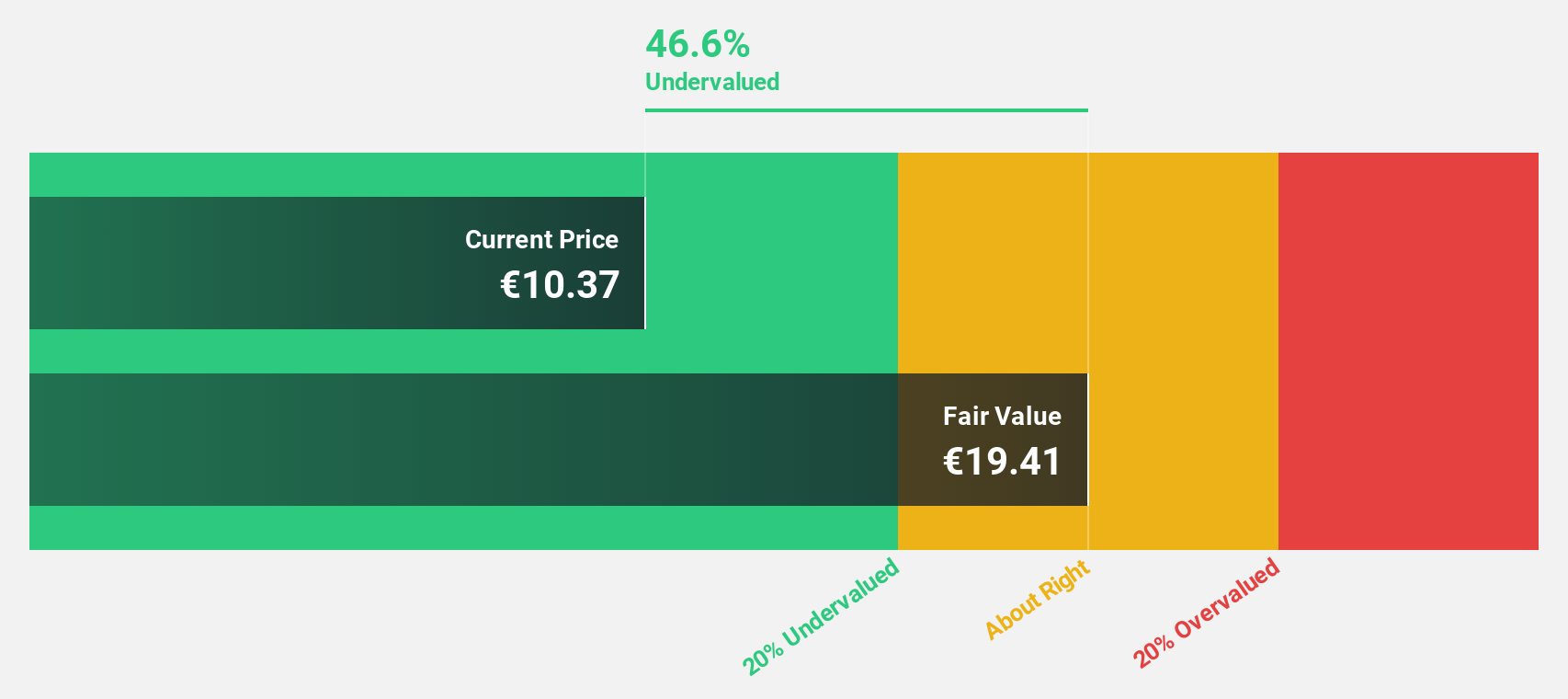

Estimated Discount To Fair Value: 22.6%

Acerinox is trading at €16.48, significantly below its estimated future cash flow value of €21.29, indicating undervaluation. Despite recent earnings showing a decline in sales to €1.38 billion and net income to €5 million, the company's earnings are forecasted to grow 39.13% annually over the next three years, becoming profitable with above-average market growth expectations. However, its dividend yield of 3.76% isn't well covered by earnings or free cash flows.

- The analysis detailed in our Acerinox growth report hints at robust future financial performance.

- Navigate through the intricacies of Acerinox with our comprehensive financial health report here.

Melexis (ENXTBR:MELE)

Overview: Melexis NV designs, develops, tests, and markets advanced integrated semiconductor devices mainly for the automotive industry across various regions including Europe, the Middle East, Africa, the Asia Pacific, and North and Latin America with a market cap of €2.93 billion.

Operations: The company's revenue primarily comes from the development and sale of integrated circuits, amounting to €843.46 million.

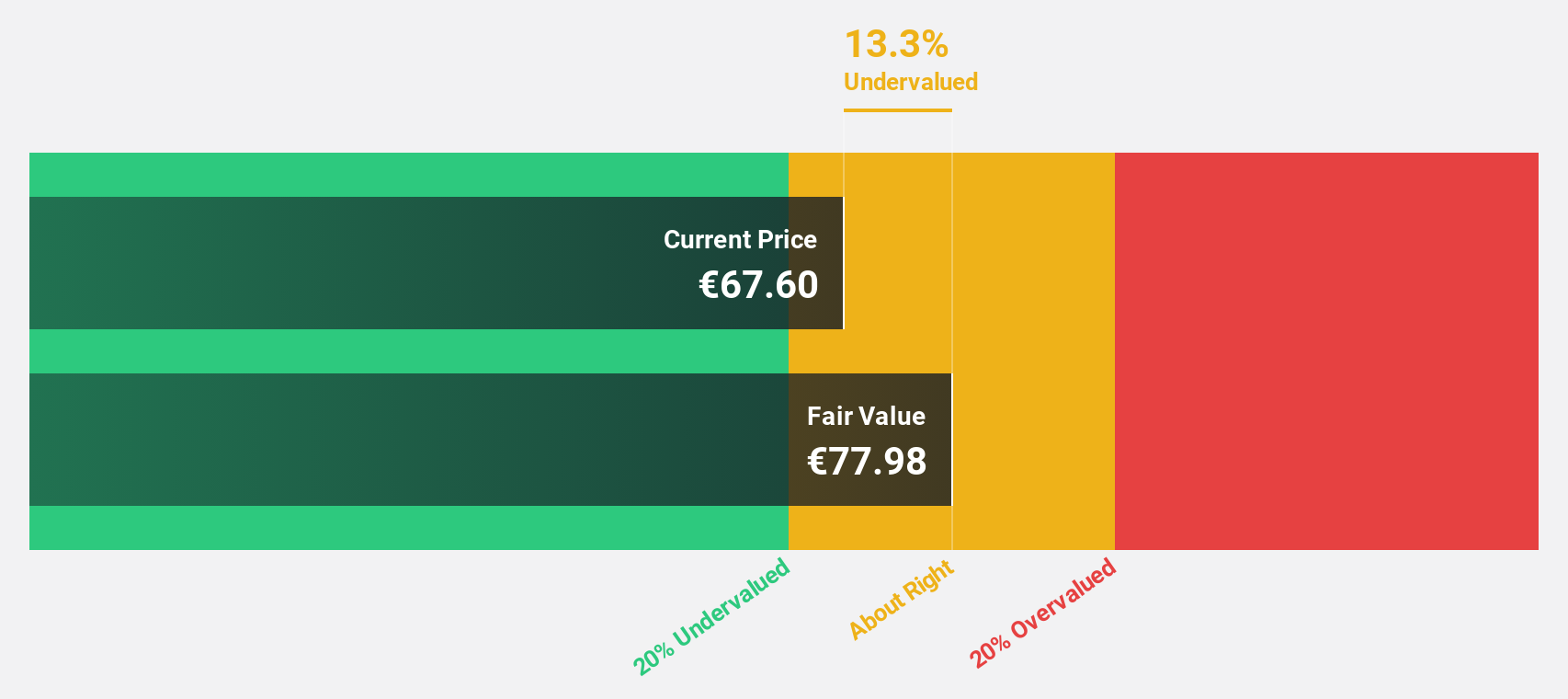

Estimated Discount To Fair Value: 19.1%

Melexis, trading at €74.35, is undervalued based on its estimated future cash flow value of €91.92. Despite a high debt level and recent earnings showing a slight decline in net income to €23.09 million, its earnings are forecasted to grow 17.62% annually, outpacing the Belgian market's growth rate of 13.7%. However, the dividend yield of 4.98% isn't well covered by earnings, and share price volatility remains high over the past three months.

- Our expertly prepared growth report on Melexis implies its future financial outlook may be stronger than recent results.

- Delve into the full analysis health report here for a deeper understanding of Melexis.

AB SKF (OM:SKF B)

Overview: AB SKF (publ) is a global company that designs, manufactures, and sells bearings and units, seals, lubrication systems, condition monitoring products, and services with a market cap of approximately SEK117.89 billion.

Operations: The company's revenue segments include Automotive, contributing SEK25.26 billion, and Segment Adjustment, accounting for SEK64.23 billion.

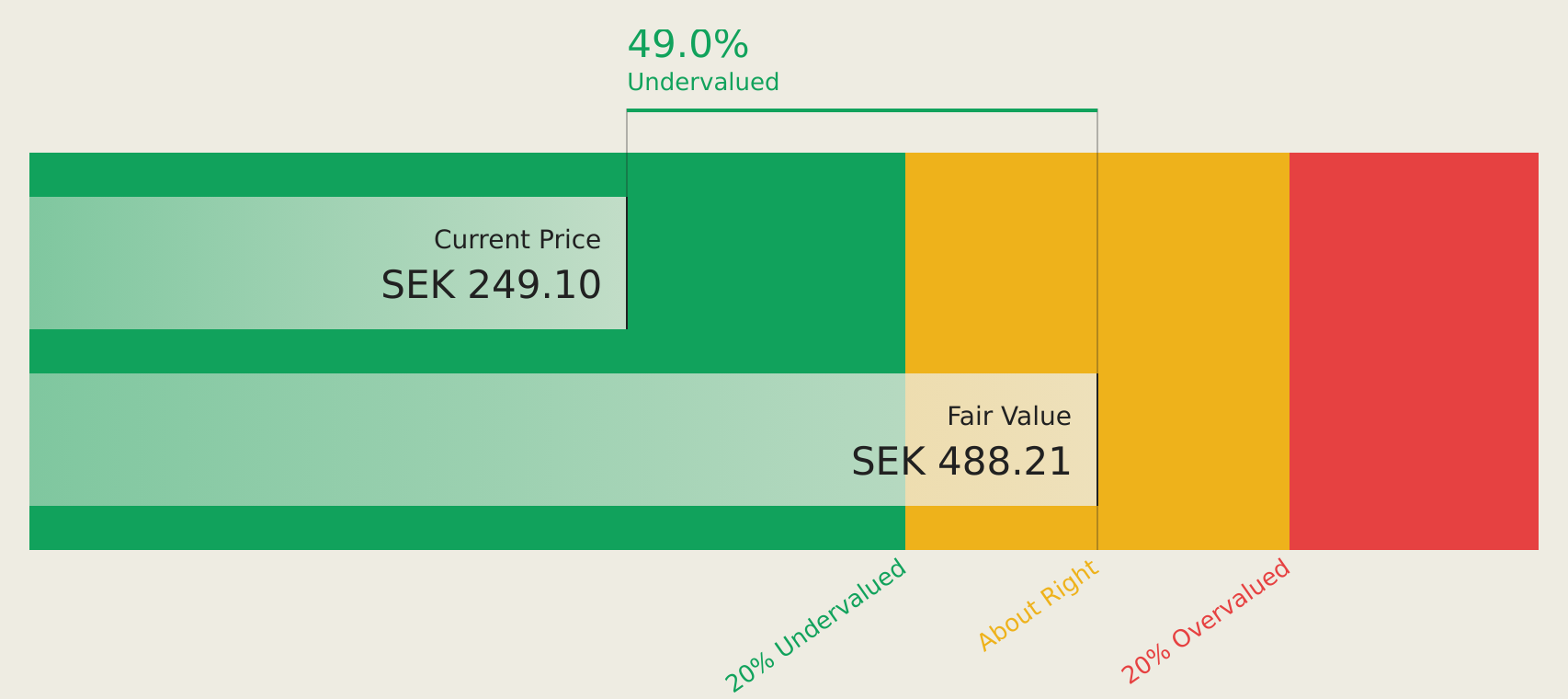

Estimated Discount To Fair Value: 47.3%

AB SKF, trading at SEK 258.9, is undervalued relative to its estimated future cash flow value of SEK 491.57. The company has entered a strategic venture with Leaderdrive in China, targeting the high-growth humanoid robotics market, which could enhance cash flows. Despite recent drops in profit margins and removal from the OMX Nordic 40 Index, forecasted earnings growth of over 20% annually suggests potential for recovery and improved valuation metrics.

- Insights from our recent growth report point to a promising forecast for AB SKF's business outlook.

- Get an in-depth perspective on AB SKF's balance sheet by reading our health report here.

Taking Advantage

- Investigate our full lineup of 192 Undervalued European Stocks Based On Cash Flows right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com