3 Global Growth Companies With High Insider Ownership Expecting Up To 92% Earnings Growth

In the current global market landscape, marked by mixed performances across major indices and heightened geopolitical tensions impacting energy prices, growth stocks have notably outpaced their value counterparts. This environment highlights the importance of identifying companies with strong growth potential and high insider ownership, as these factors can indicate confidence in a company's future prospects despite broader market volatility.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Taotao Vehicles (SZSE:301345) | 27.9% | 31.5% |

| Shanghai Biren Technology (SEHK:6082) | 11% | 116.9% |

| Meitu (SEHK:1357) | 22.8% | 31.4% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| KebNi (OM:KEBNI B) | 11.8% | 90.9% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

| Fulin Precision (SZSE:300432) | 10.4% | 60.7% |

| CD Projekt (WSE:CDR) | 35.2% | 29.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

Let's explore several standout options from the results in the screener.

Eugene TechnologyLtd (KOSDAQ:A084370)

Simply Wall St Growth Rating: ★★★★★★

Overview: Eugene Technology Co., Ltd. manufactures and sells semiconductor equipment and parts both in South Korea and internationally, with a market cap of ₩3.33 trillion.

Operations: Eugene Technology Co., Ltd. generates revenue through the production and distribution of semiconductor equipment and parts across domestic and international markets.

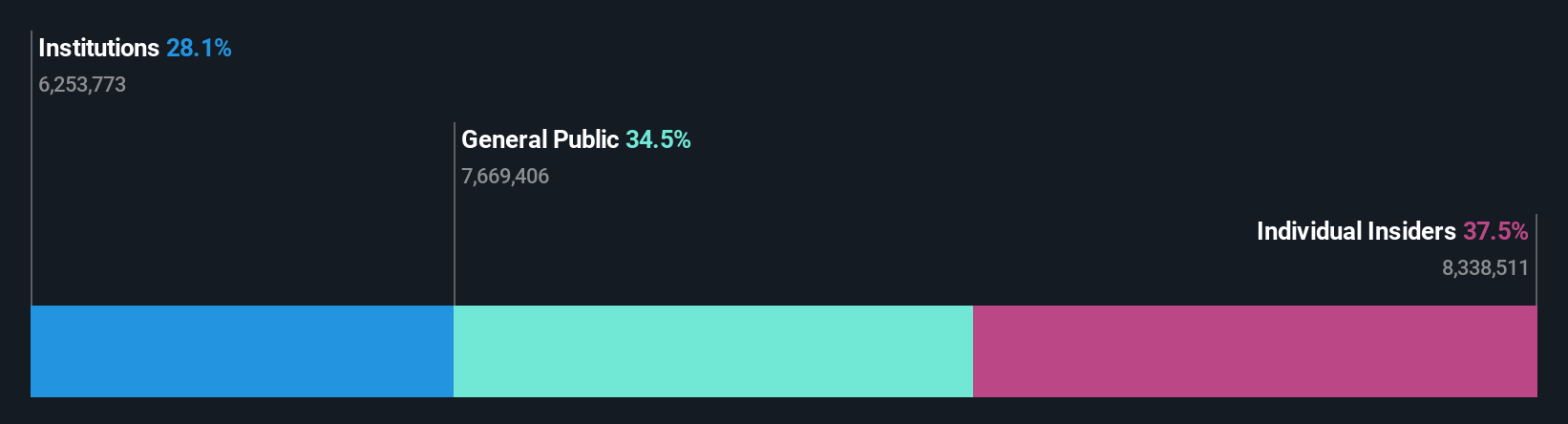

Insider Ownership: 36.7%

Earnings Growth Forecast: 34.1% p.a.

Eugene Technology Ltd. demonstrates strong growth potential, with revenue expected to grow 27.7% annually and earnings projected to increase by 34.05% per year, surpassing the Korean market averages. Despite a volatile share price recently, the company's first-quarter net income surged significantly to KRW 21.75 billion from KRW 7.53 billion a year ago, indicating robust financial performance amidst high insider ownership that aligns management interests with shareholders'.

- Get an in-depth perspective on Eugene TechnologyLtd's performance by reading our analyst estimates report here.

- The analysis detailed in our Eugene TechnologyLtd valuation report hints at an inflated share price compared to its estimated value.

ROBOTIS (KOSDAQ:A108490)

Simply Wall St Growth Rating: ★★★★★☆

Overview: ROBOTIS Co., Ltd. offers robotic solutions in South Korea and has a market cap of ₩2.86 trillion.

Operations: The company generates revenue from various segments, with no specific amounts detailed in the provided text.

Insider Ownership: 23.8%

Earnings Growth Forecast: 92.1% p.a.

ROBOTIS faces challenges with a significant first-quarter net loss of KRW 10.06 billion, contrasting sharply with last year's profit. Despite this, the company is forecasted to achieve profitability within three years and boasts an expected annual revenue growth of 63.9%, outpacing the Korean market average significantly. High insider ownership may align management interests with shareholders', but recent share price volatility and low future return on equity (10.6%) present potential concerns for investors.

- Navigate through the intricacies of ROBOTIS with our comprehensive analyst estimates report here.

- Upon reviewing our latest valuation report, ROBOTIS' share price might be too optimistic.

Korea Circuit (KOSE:A007810)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Korea Circuit Co., Ltd. is involved in the production and sale of printed circuit boards globally, with a market cap of ₩1.69 trillion.

Operations: The company's revenue primarily stems from its printed circuit board manufacturing segment, which generated ₩1.58 trillion.

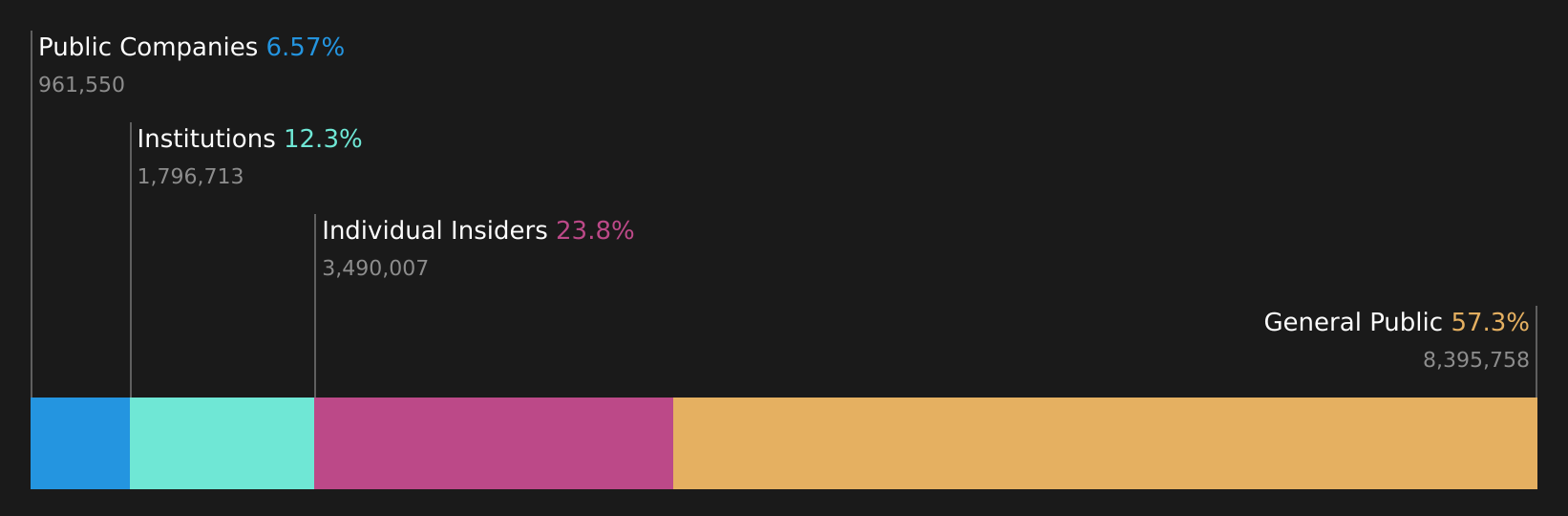

Insider Ownership: 12.4%

Earnings Growth Forecast: 37.8% p.a.

Korea Circuit's earnings are projected to grow significantly at 37.85% annually, outpacing the Korean market's average. Despite recent share price volatility, it is trading at a substantial discount to its estimated fair value. Revenue growth of 14.5% per year is slower than the market average but remains robust. High insider ownership could align management interests with shareholders', although no recent insider trading activity has been reported in the last three months.

- Click here and access our complete growth analysis report to understand the dynamics of Korea Circuit.

- Insights from our recent valuation report point to the potential undervaluation of Korea Circuit shares in the market.

Where To Now?

- Embark on your investment journey to our 700 Fast Growing Global Companies With High Insider Ownership selection here.

- Searching for a Fresh Perspective? The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com