Great-West Lifeco (TSX:GWO) Could Be 17% Overvalued On Retirement Platform Expansion

Great-West Lifeco (TSX:GWO) recently announced an expansion of its retirement administration platform, a move that directly targets workplace plans and employer relationships that matter for long-term savings flows.

See our latest analysis for Great-West Lifeco.

At a share price of CA$91.25, Great-West Lifeco has logged a 30-day share price return of 9.43% and a year-to-date share price return of 35.99%. Its 1-year total shareholder return of 83.17% and 5-year total shareholder return of 220.07% point to strong, sustained momentum that recent platform expansion news may be helping to reinforce.

If this kind of compounding story has your attention, it could be a good moment to broaden your radar and check out 3 top founder-led companies

After such a strong run and fresh optimism around the retirement platform expansion, the real tension for Great-West Lifeco now is simple: does the current price still leave enough upside to justify the risks you are taking?

Most Popular Narrative: 17.4% Overvalued

Compared with Great-West Lifeco's last close at CA$91.25, the most followed narrative lands on a fair value of CA$77.75, framing current enthusiasm as richer than its modelled worth based on a 6.35% discount rate.

Expansion of fee-based, capital-light wealth and asset management businesses (such as Empower) provides more stable, recurring earnings and higher return on equity, leading to more predictable and higher-quality earnings growth.

Significant runway for revenue growth exists from capturing "money in motion" through rollovers/crossovers and increased product penetration among Empower's large participant base, which is likely to boost both asset-based and participant-based fee income.

Want to understand why this valuation leans richer despite those long-run fee and margin ambitions? The narrative hinges on a tight balance of revenue growth, profit margin resilience, and future earnings multiples that are anything but generic.

Result: Fair Value of CA$77.75 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, investors in Great-West Lifeco still need to weigh demographic outflows from retiring participants and fee compression in workplace plans, either of which could put pressure on fee-based revenue.

Find out about the key risks to this Great-West Lifeco narrative.

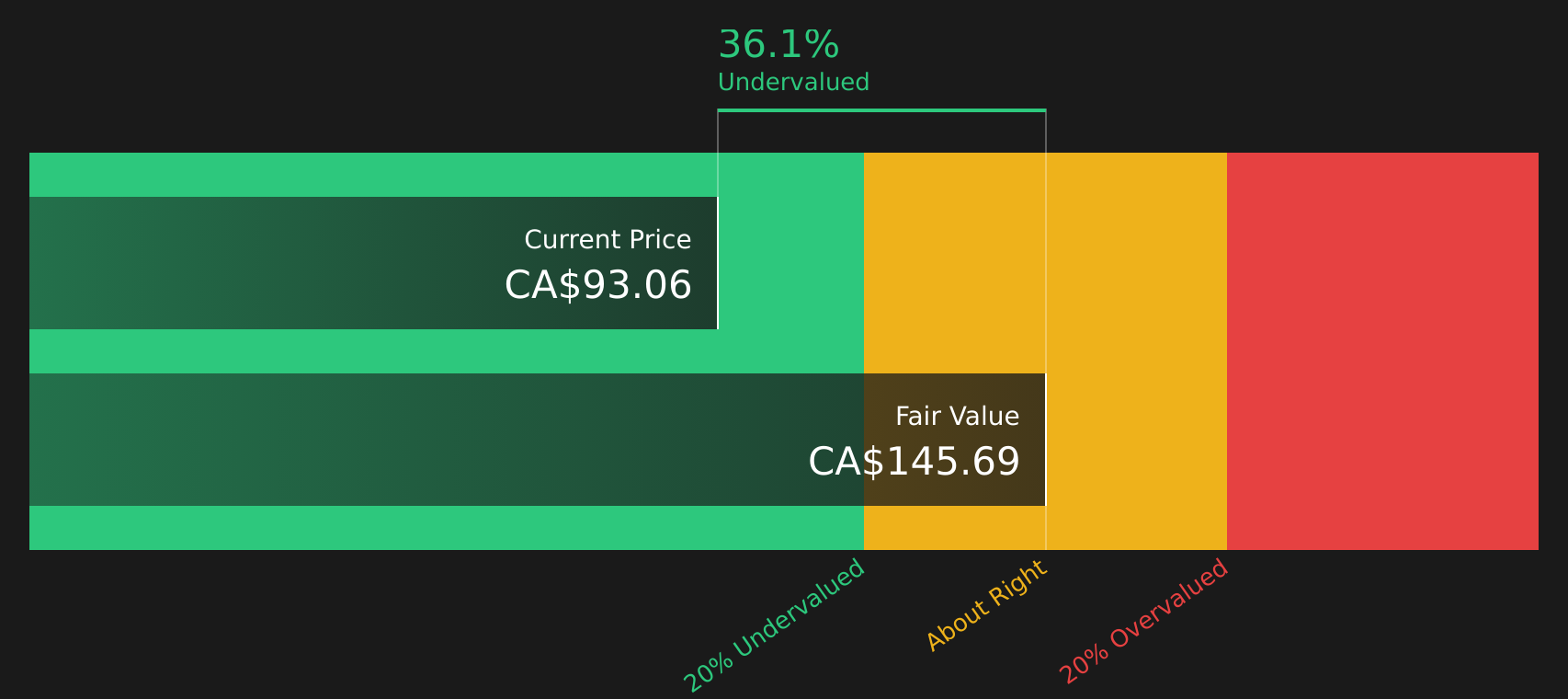

Another View: Great-West Lifeco Through a Cash Flow Lens

While the analyst narrative frames Great-West Lifeco as 17.4% overvalued at CA$91.25 versus a CA$77.75 target, the SWS DCF model comes to a very different conclusion. It indicates the stock is trading below an estimated future cash flow value of CA$146.49. That sort of gap raises a simple question: which set of assumptions do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Great-West Lifeco for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 5 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of optimism and caution around Great-West Lifeco leaves you undecided, consider taking action while the data is fresh and weigh the 4 key rewards

Looking for more investment ideas beyond Great-West Lifeco?

Great-West Lifeco may be on your radar now, but the next opportunity could be sitting in plain sight, waiting for you to act before everyone else.

- Target undervalued opportunities that combine quality and price by scanning companies through the 5 high quality undervalued stocks.

- Strengthen your income stream by hunting for dependable high-yield payers using the 6 dividend fortresses.

- Reduce portfolio surprises by focusing on companies with sturdier finances via the solid balance sheet and fundamentals stocks screener (12 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com