3 China Industrial Stocks Riding Strong Factory Output And AI Hardware Demand

China’s latest data paints a mixed picture, with slower Q2 GDP growth at 4.3%, weaker fixed asset investment, but firmer industrial output and a small rebound in retail sales. For investors watching Chinese industrial and manufacturing stocks, this combination of softer growth, stronger factories and the possibility of policy stimulus creates both risk and opportunity. This article looks at how that backdrop connects to China’s industrial sector and highlights 3 stocks from our Chinese Industrial and Manufacturing Sector screener that appear positively exposed to these trends for investors considering where to focus attention next.

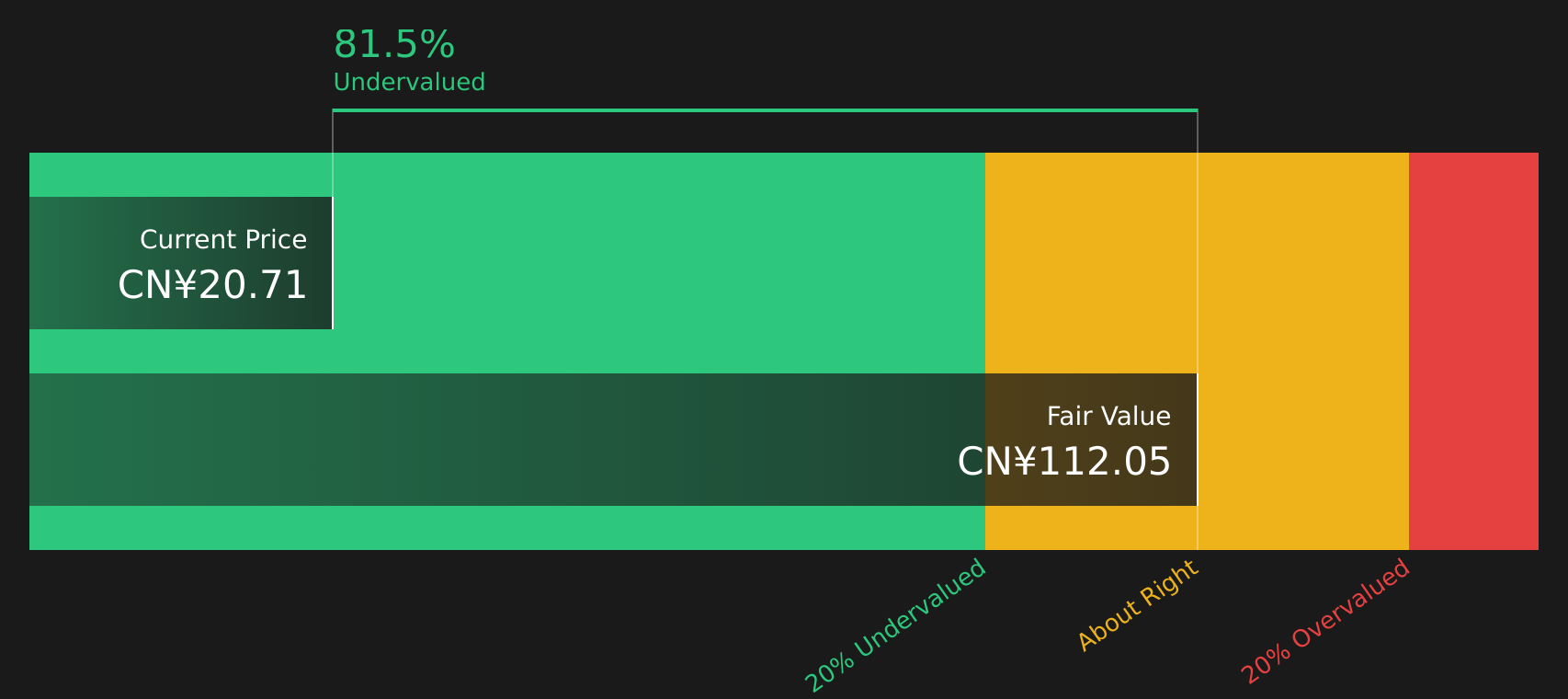

Zhejiang HangKe Technology (SHSE:688006)

Overview: Zhejiang HangKe Technology designs and sells lithium battery post processing systems used to test, age and manage pouch, prismatic, cylindrical and 3C lithium ion cells, along with software that coordinates testing and logistics. Its equipment sits at the final stage of the battery manufacturing line, helping producers ensure cells are safe, reliable and ready for use in electric vehicles and other rechargeable applications.

Market Cap: CN¥14.49b

Against a backdrop of softer GDP but firm industrial output, Zhejiang HangKe Technology sits in a part of China’s export machine that directly serves lithium battery and electronics producers, both linked to AI related hardware demand. The stock combines growth forecasts for revenue and earnings with a P/E below the peer average and a share price that is well below one estimate of fair value. This may appeal to investors looking for growth at a reasonable price. At the same time, funding relies heavily on external borrowing, the dividend record is uneven and recent share price swings have been sharp, so the balance of growth potential and higher financial and governance risk may warrant closer analysis.

Growth forecasts, a below peer P/E and a share price sitting well under one fair value estimate make Zhejiang HangKe Technology look mispriced, but the real twist sits inside the 4 key rewards and 2 important warning signs

Amlogic (Shanghai)Ltd (SHSE:688099)

Overview: Amlogic (Shanghai)Ltd is a fabless semiconductor designer that creates system on a chip and related chips used in smart TVs, AI enabled home devices, connected cars and other electronics across consumer, commercial and industrial settings in China and overseas.

Operations: Amlogic (Shanghai)Ltd generates essentially all of its CN¥7.16b in revenue from the research, production and sale of semiconductor integrated circuit chips.

Market Cap: CN¥41.29b

Amlogic (Shanghai)Ltd sits at the heart of China’s AI hardware and smart device supply chain, with industrial output tied closely to global demand for connected screens and AIoT gadgets. Forecasts point to strong earnings and revenue growth. Its P/E sits well below the broader semiconductor industry, which may appeal if you are looking for growth exposure at a more measured valuation. That said, returns on equity are modest, profits lean heavily on non cash items and funding is fully reliant on external borrowing, all areas that could matter if conditions tighten. With Q1 2026 revenue up but net income slightly lower and an earnings update due on August 20, 2026, the real question is whether current pricing truly reflects that mix of growth potential and governance risk.

Amlogic (Shanghai) Ltd sits at the intersection of AI hardware and smart devices, yet its P/E trails the wider chip sector and Q1 2026 earnings softened, so the full story may sit inside the 3 key rewards and 1 important major warning sign

Suzhou Maxwell Technologies (SZSE:300751)

Overview: Suzhou Maxwell Technologies designs and manufactures equipment used to produce high efficiency solar cells, along with OLED, mini and micro LED production systems and specialist laser cutting and wafer processing tools for electronics makers in China and across Southeast Asia.

Market Cap: CN¥65.81b

With China’s industrial output holding up and global demand for AI related hardware and electrification equipment shaping factory orders, Suzhou Maxwell Technologies gives you exposure to the machinery behind high efficiency solar and advanced display production. Forecasts for earnings and revenue growth, rising profit margins and an experienced management team all work in its favour, even if recent declines in sales and net income, an unstable dividend record, reliance on external borrowing and higher share price volatility mean the ride may not be smooth. For investors weighing this mix of potential growth, valuation and funding risk, the upcoming H1 2026 results on August 25 may be an important moment that the current share price does not yet fully reflect.

Solar machinery growth at Suzhou Maxwell Technologies is colliding with funding and earnings questions, so the real edge may lie in the overlooked details inside the 3 key rewards and 2 important warning signs

The three Chinese industrial and manufacturing stocks in this article are just a starting point. Our full Chinese Industrial and Manufacturing Sector screener surfaces 44 more companies that combine solid financial profiles with export and AI related factory stories that may be similarly compelling. Use Simply Wall St to identify and analyze the specific catalysts, financial health factors and narratives that matter most to you, so you can focus on the ideas in this sector that best align with your own convictions.

Take Control of Your Investment Journey

If Amlogic (Shanghai)Ltd or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Stocks?

Fresh ideas move first, and the strongest stories often gain momentum before the crowd notices. Do not let under the radar opportunities be caught flying past you, act now.

- Spot higher yield setups before they are bid up by others by scanning our hand picked 474 dividend fortresses built for income focused investors who also care about resilience.

- Track early AI momentum where profits already matter, not just promises, using a curated pool of 63 profitable AI stocks that aren't just burning cash that balance growth potential with real earnings today.

- Position ahead of potential infrastructure shifts by reviewing a filtered group of 34 power grid technology and infrastructure stocks focused on companies tied to grid upgrades while they are still under the radar for now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com