Asian Growth Companies With Insider Ownership Up To 16%

Amidst the backdrop of geopolitical tensions and fluctuating energy markets, Asia's stock indices have shown mixed performance, with technology sectors often leading gains due to advancements in AI and semiconductor industries. In this environment, growth companies with significant insider ownership can be particularly appealing as they may indicate confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Taotao Vehicles (SZSE:301345) | 27.9% | 31.5% |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 73.1% |

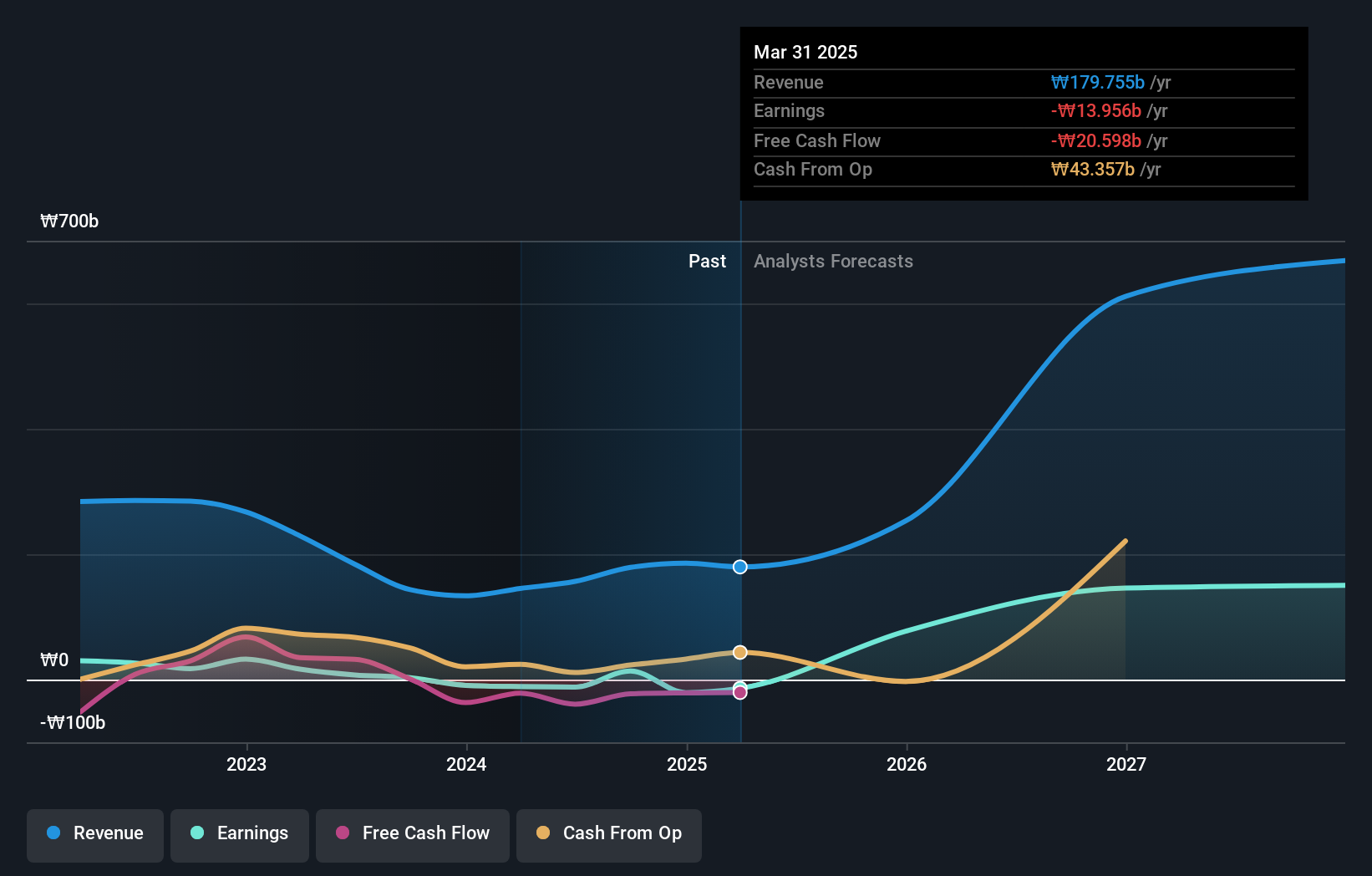

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 110.6% |

| SEERS (KOSDAQ:A458870) | 33.2% | 41.5% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| Jiangxi Fushine Pharmaceutical (SZSE:300497) | 21.1% | 55.9% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Great Microwave Technology (SHSE:688270) | 29.5% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

We'll examine a selection from our screener results.

Techwing (KOSDAQ:A089030)

Simply Wall St Growth Rating: ★★★★★★

Overview: Techwing, Inc. develops, manufactures, sells, and services semiconductor inspection equipment both in South Korea and internationally with a market cap of ₩1.73 trillion.

Operations: Techwing's revenue is derived from the development, manufacturing, sales, and servicing of semiconductor inspection equipment in both domestic and international markets.

Insider Ownership: 14.3%

Techwing's earnings are forecast to grow significantly, outpacing the Korean market. Despite trading at 47.3% below its estimated fair value, it faces challenges with volatile share prices and interest payments not well covered by earnings. Recent financial results show a net loss increase, but growth prospects in the semiconductor test market remain promising. The company's substantial insider ownership aligns interests with shareholders as it navigates these opportunities and challenges.

- Unlock comprehensive insights into our analysis of Techwing stock in this growth report.

- Insights from our recent valuation report point to the potential undervaluation of Techwing shares in the market.

Shanjin International Gold (SZSE:000975)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanjin International Gold Co., Ltd. engages in the exploration, mining, and trading of precious and non-ferrous metal ores in China, with a market capitalization of CN¥55.17 billion.

Operations: The company generates revenue through its activities in the exploration, extraction, and trading of precious and non-ferrous metal ores within China.

Insider Ownership: 12%

Shanjin International Gold's earnings grew by 55.3% last year and are forecast to increase significantly over the next three years, outpacing the Chinese market. The stock trades at a substantial discount to its estimated fair value. Despite an unstable dividend track record, recent earnings show strong performance with net income reaching CNY 1.39 billion for Q1 2026, up from CNY 693.83 million a year ago, indicating robust growth potential amidst insider ownership stability.

- Click here and access our complete growth analysis report to understand the dynamics of Shanjin International Gold.

- Our valuation report here indicates Shanjin International Gold may be undervalued.

Shandong Dawn PolymerLtd (SZSE:002838)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shandong Dawn Polymer Co., Ltd. is engaged in the development, production, sale, and servicing of thermoplastic elastomers, modified plastics, master batches, and other products both in China and internationally with a market cap of CN¥16.40 billion.

Operations: Shandong Dawn Polymer Co., Ltd. generates revenue through its activities in thermoplastic elastomers, modified plastics, and master batches across domestic and international markets.

Insider Ownership: 16.3%

Shandong Dawn Polymer Ltd. demonstrates strong growth potential with earnings expected to grow significantly at 35% annually, outpacing the Chinese market. Recent financial results show robust performance, with Q1 2026 net income reaching CNY 119.09 million, up from CNY 44.28 million a year ago. Despite recent cancellations of asset acquisition plans and private placements, insider ownership remains stable, supporting confidence in its projected revenue growth of over 20% per year amidst market challenges.

- Take a closer look at Shandong Dawn PolymerLtd's potential here in our earnings growth report.

- Our expertly prepared valuation report Shandong Dawn PolymerLtd implies its share price may be too high.

Summing It All Up

- Navigate through the entire inventory of 480 Fast Growing Asian Companies With High Insider Ownership here.

- Curious About Other Options? Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com