Is Norion Bank (OM:NORION) Undervalued Following Earnings Positioning Ahead Of July 14?

Norion Bank (OM:NORION) heads into its H1 2026 earnings call on July 14, with investor attention fixed on how fresh numbers align with adjusted 2026 and 2027 profit expectations.

See our latest analysis for Norion Bank.

Norion Bank’s recent 1-day share price return of 0.95% and 7-day share price return of 3.40% suggest investors are positioning ahead of the earnings call, even as the year-to-date share price return is down 5.47% and the 3-year total shareholder return of 88.22% points to a much stronger longer-term picture.

If you are looking beyond Norion Bank for what could be next in financials and credit-focused lenders, consider broadening your search and check out 106 top founder-led companies

After Norion Bank’s recent bounce and with the stock still trading below the average analyst target and some intrinsic value estimates, where does a reasonable fair value range really sit as you weigh the current discount?

Price-to-Earnings of 9.1x: Is it justified?

On a P/E of 9.1x at a last close of SEK63.90, Norion Bank is priced below both its peer group and a fair-value P/E estimate implied by fundamentals.

The P/E ratio compares the company’s share price to its earnings per share. For banks like Norion Bank it gives a quick sense of what investors are paying for each unit of current profit.

According to the statements, Norion Bank is described as trading at good value compared to peers and the broader European banks sector, with its 9.1x P/E sitting below the 13.4x peer average and the 12x European banks average. The same data set also points to a fair P/E closer to 10.5x, which is higher than where the stock sits today and highlights a valuation level the market could potentially move toward if earnings forecasts and quality hold up.

Explore the SWS fair ratio for Norion Bank.

Result: Price-to-Earnings of 9.1x (UNDERVALUED)

However, Norion Bank’s credit focused model and exposure to real estate and consumer lending mean any spike in impairments or funding costs could quickly challenge the valuation story.

Find out about the key risks to this Norion Bank narrative.

Another view on Norion Bank’s valuation

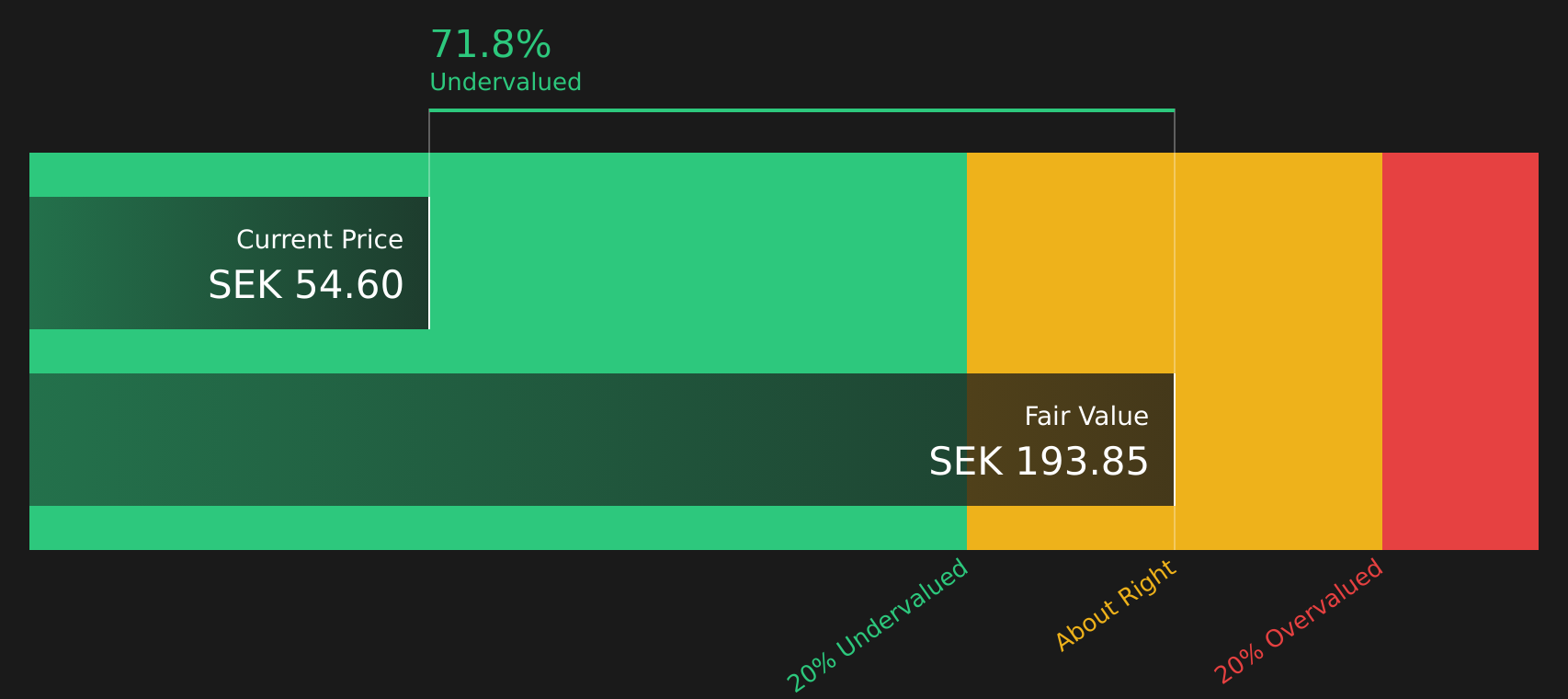

While Norion Bank looks cheap on a 9.1x P/E, the SWS DCF model paints an even stronger picture, with an estimated future cash flow value of SEK197 per share versus a current price of SEK63.90, suggesting the stock screens as heavily undervalued. The real question is how much weight you want to put on that long term cash flow path.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Norion Bank for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 218 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across Norion Bank’s valuation and outlook, now is the time to review the data firsthand and decide how comfortable you are with the trade off between risk and potential reward. To weigh those factors in more detail, start by reviewing the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Norion Bank?

If Norion Bank has sharpened your focus on valuation and quality, do not stop here. Use the Simply Wall Street Screener to surface fresh opportunities right now.

- Target reliable compounding potential by focusing on companies with strong cash flows trading below intrinsic value using the 218 high quality undervalued stocks.

- Strengthen your income stream by zeroing in on established businesses offering robust payouts through the 472 dividend fortresses.

- Guard your capital and seek smoother portfolio returns by filtering for companies with resilient profiles via the 296 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com