3 Global Undervalued Small Caps With Insider Action To Watch

In the current global market landscape, small-cap stocks have faced mixed performance amid geopolitical tensions and fluctuating energy prices, with the Russell 2000 Index experiencing a slight decline. As investors navigate these uncertainties, identifying small-cap companies that demonstrate strong fundamentals and insider activity can offer potential opportunities for growth.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| CellaVision | 24.6x | 4.5x | 43.55% | ★★★★★★ |

| Eurocell | 11.3x | 0.3x | 48.83% | ★★★★★☆ |

| Centurion | 11.6x | 4.0x | 34.38% | ★★★★★☆ |

| Firan Technology Group | 39.4x | 2.9x | 21.15% | ★★★★☆☆ |

| Primaris Real Estate Investment Trust | 13.5x | 3.9x | 44.90% | ★★★★☆☆ |

| Nexus Industrial REIT | 10.2x | 3.4x | 5.45% | ★★★★☆☆ |

| Sagicor Financial | 32.0x | 0.6x | 35.04% | ★★★★☆☆ |

| Pizza Pizza Royalty | 14.3x | 10.9x | 32.15% | ★★★☆☆☆ |

| AB Dynamics | NA | 2.2x | 36.35% | ★★★☆☆☆ |

| Chinasoft International | 20.7x | 0.4x | -2540.30% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

Volex (AIM:VLX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Volex is a global manufacturer and supplier of complex assemblies for power products and cable assemblies, with a market cap of approximately £0.83 billion.

Operations: Volex generates revenue primarily through its operations, with a significant portion of costs attributed to the cost of goods sold (COGS). Over recent periods, the company has seen fluctuations in its gross profit margin, reaching 22.59% in the latest quarter. Operating expenses are a notable component of Volex's cost structure, contributing to overall financial performance.

PE: 18.8x

Volex, a company with sales of US$1.24 billion for the year ending March 31, 2026, has shown promising growth with net income rising to US$65.8 million from US$47.9 million the previous year. Basic earnings per share increased to US$0.352 from US$0.259, indicating improved profitability despite relying on external borrowing for funding. Insider confidence is evident as they have been actively purchasing shares recently, reflecting optimism in future prospects amidst an expected annual earnings growth of 11%.

- Click here to discover the nuances of Volex with our detailed analytical valuation report.

Assess Volex's past performance with our detailed historical performance reports.

Imdex (ASX:IMD)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Imdex is a company that manufactures and sells or rents products and software to the mining sector, with a market cap of A$1.03 billion.

Operations: Imdex generates revenue primarily from the manufacture and sale or rental of products and software to the mining sector, with a recent reported revenue of A$466.36 million. The company experienced a gross profit margin trend reaching 72.43% as of December 2025, indicating an increase over time. Operating expenses include significant allocations to general and administrative costs, which were A$142.16 million in the latest period analyzed.

PE: 38.4x

Imdex, a company characterized by its reliance on external borrowing, recently saw insider confidence as Anthony Wooles acquired 500,000 shares for A$1.96 million in April 2026. This significant purchase increased their holdings by 187%, indicating strong belief in the company's prospects. Despite higher risk funding sources, Imdex is positioned for potential growth with earnings projected to grow annually at 15.79%. Such insider activity may hint at optimism within the industry context.

- Click here and access our complete valuation analysis report to understand the dynamics of Imdex.

Explore historical data to track Imdex's performance over time in our Past section.

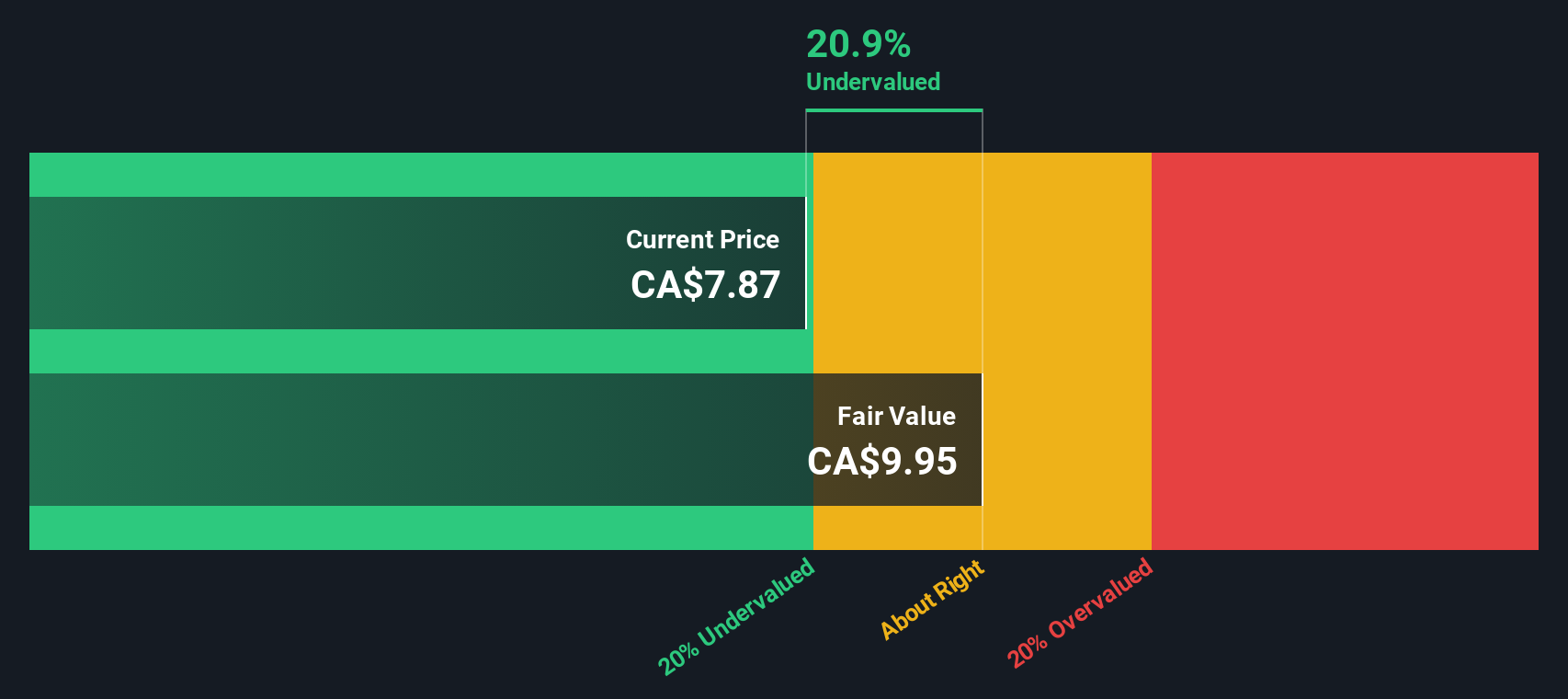

Nexus Industrial REIT (TSX:NXR.UN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Nexus Industrial REIT is a Canadian real estate investment trust focused on owning and managing a portfolio of industrial properties, with a market cap of CA$1.18 billion.

Operations: Nexus Industrial REIT generates revenue primarily from investment properties, with the latest reported revenue at CA$173.86 million. The company has shown a gross profit margin of 74.08% as of the most recent period, indicating a strong ability to manage costs relative to its revenues. Operating expenses are consistently managed, contributing to its financial performance over time.

PE: 10.2x

Nexus Industrial REIT, a smaller player in the real estate investment sector, recently saw insider confidence through share purchases, signaling potential value. With first-quarter sales rising to C$46.02 million from C$44.75 million last year and net income slightly dipping to C$32.18 million, the company shows resilience amid market fluctuations. The recent appointment of Curt Millar to the board adds strategic depth given his extensive experience in real estate finance. Despite relying on higher-risk external borrowing for funding, Nexus maintains a stable credit rating of BBB (low) with a stable trend from Morningstar DBRS for its $500 million debenture offering aimed at refinancing debt and general purposes. Looking ahead, earnings are projected to grow annually by 2.97%, suggesting cautious optimism for future prospects within this niche segment.

Summing It All Up

- Reveal the 132 hidden gems among our Undervalued Global Small Caps With Insider Buying screener with a single click here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com