Is TriCo Bancshares (TCBK) Fully Valued On Its $2b Takeover Deal?

TriCo Bancshares (TCBK) is back in focus after First Hawaiian, Inc. entered a definitive all stock agreement to acquire the California based bank in a transaction valued at about $2 billion.

See our latest analysis for TriCo Bancshares.

The takeover announcement has clearly reset expectations around TriCo Bancshares, with a 1-day share price return of 11.99% and a year-to-date share price return of 27.40% sitting alongside a 1-year total shareholder return of 43.90%. This points to strong, deal-driven momentum rather than a gradual rerating.

If this acquisition has you looking beyond a single regional bank, it could be a good moment to scan the market for other opportunities through the 18 top founder-led companies

TriCo Bancshares now trades close to the implied US$63.12 offer price, so the question shifts: Is there still enough potential upside and compensation for deal and market risk, or has most of the reward already been taken?

Price to Earnings of 14.9x: Is it justified?

TriCo Bancshares now finds itself in an unusual spot, with a pending all stock acquisition on the table and a P/E of 14.9x that sits between what peers and the broader US Banks industry are trading at.

The P/E ratio compares the current share price to the company’s earnings per share. For a bank like TriCo Bancshares it is a simple way to see how much investors are paying for each dollar of earnings. At 14.9x, the stock is described as good value relative to a peer average P/E of 28.3x. This suggests the market is not assigning the kind of premium that some similar companies carry, despite TCBK having high quality earnings, net profit margins of 31%, and consistent profit growth over the past 5 years.

However, that same 14.9x multiple is described as expensive when set against the wider US Banks industry average of 12.2x. It also sits above the estimated fair P/E of 11.5x that the SWS fair ratio model points to as a level the valuation could gravitate toward over time if sentiment cools or deal related enthusiasm fades.

Explore the SWS fair ratio for TriCo Bancshares

Result: Price-to-earnings of 14.9x (OVERVALUED).

However, TriCo Bancshares still faces deal risks, including potential regulatory hurdles and the possibility that any shift in market sentiment could narrow or erase the remaining merger upside.

Find out about the key risks to this TriCo Bancshares narrative.

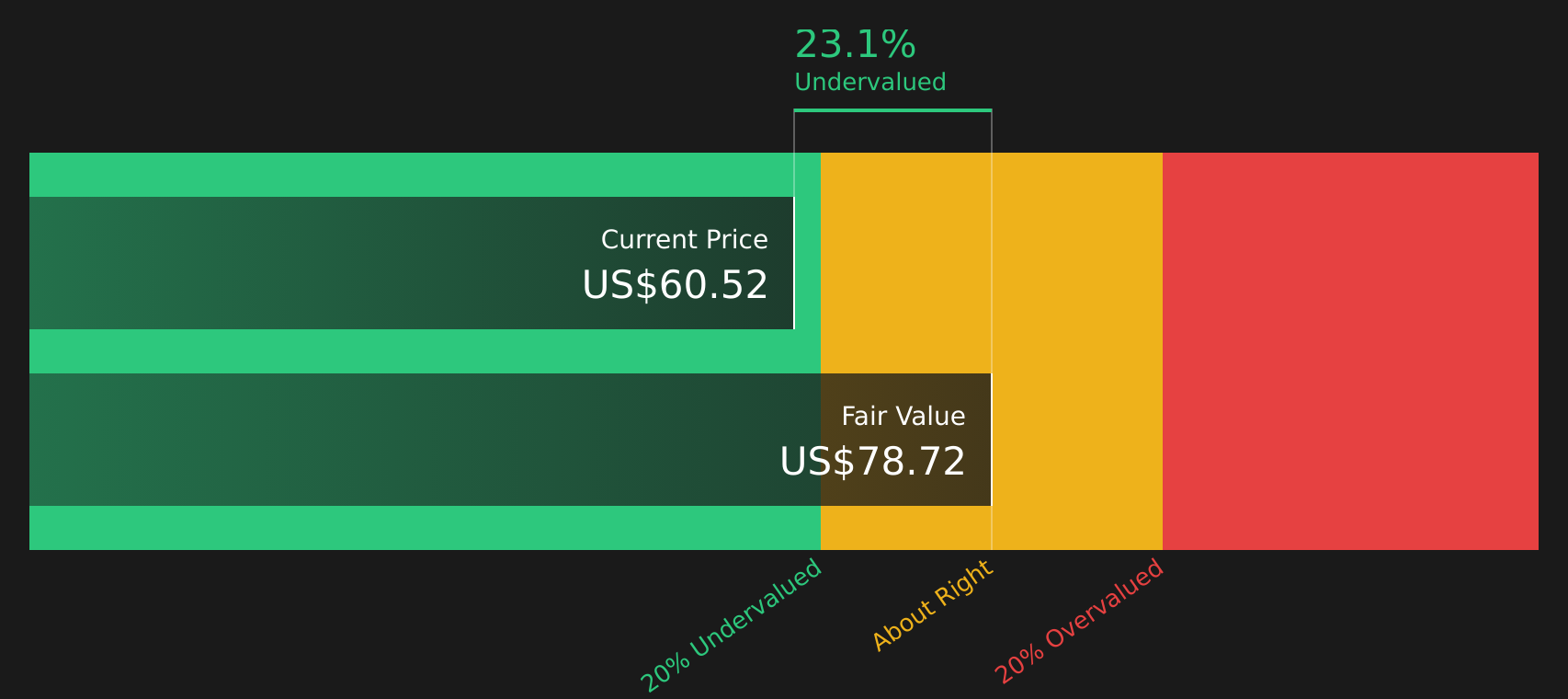

Another View: SWS DCF Model Suggests Undervaluation

The P/E discussion presents TriCo Bancshares as slightly expensive relative to the wider US Banks industry, but the SWS DCF model offers a different perspective. With TCBK at $60.07 and the model indicating a fair value of $77.87, the shares appear about 22.9% undervalued. That gap could reflect either potential upside or the risk that the cash flow assumptions are too optimistic, so which interpretation do you consider more realistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out TriCo Bancshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of deal risk and potential reward leaves you undecided, take a moment to review the positives and shape your own view on TriCo Bancshares using the 4 key rewards

Looking for more investment ideas beyond TriCo Bancshares?

If TriCo Bancshares has sharpened your focus, do not stop here. Use the Simply Wall Street Screener to surface fresh opportunities that match your style.

- Target generous income streams and stress test them using the 8 dividend fortresses.

- Hunt for quality companies that might be trading at a discount through the screener containing 20 high quality undiscovered gems.

- Prioritise resilience and sleep easier at night by filtering with the 80 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com