Three Undiscovered Gems in the United Kingdom with Strong Potential

The UK's FTSE 100 and FTSE 250 indices have recently faced downward pressure, influenced by weak trade data from China that highlights ongoing global economic challenges. In such a climate, identifying promising small-cap stocks with resilient business models and growth potential can be key to navigating market uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| ME Group International | 14.10% | 2.44% | 18.95% | ★★★★★★ |

| Keystone Law Group | NA | 13.09% | 13.27% | ★★★★★★ |

| Serabi Gold | NA | 22.72% | 54.70% | ★★★★★★ |

| AltynGold | 27.47% | 28.92% | 35.78% | ★★★★★★ |

| Yü Group | 10.53% | 36.12% | 50.56% | ★★★★★☆ |

| Integrated Diagnostics Holdings | 39.06% | 13.94% | 2.66% | ★★★★★☆ |

| PayPoint | 182.83% | 21.49% | 0.42% | ★★★★★☆ |

| Pinewood Technologies Group | 0.10% | -49.74% | -0.64% | ★★★★★☆ |

| Halyk Bank of Kazakhstan | 71.50% | 20.70% | 20.84% | ★★★★☆☆ |

| Distribution Finance Capital Holdings | 12.97% | 42.17% | 59.43% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

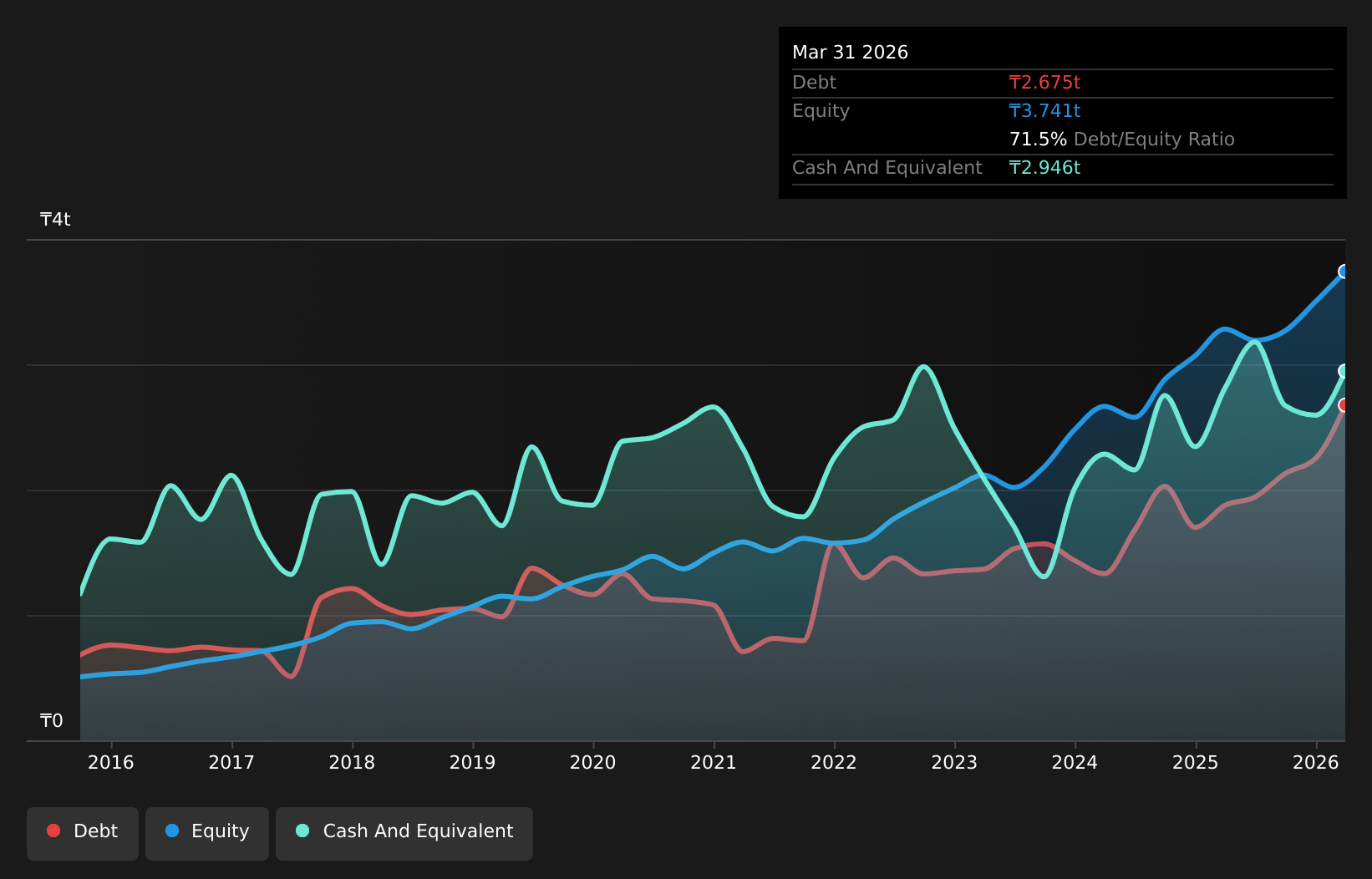

Halyk Bank of Kazakhstan (LSE:HSBK)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Halyk Bank of Kazakhstan Joint Stock Company operates as a leading financial institution offering corporate and retail banking services across Kazakhstan, Kyrgyzstan, Georgia, and Uzbekistan with a market capitalization of approximately $8.44 billion.

Operations: Halyk Bank's primary revenue streams are corporate banking, generating KZT 751.43 million, followed by investment banking at KZT 329.65 million. Retail banking and SME banking also contribute significantly with revenues of KZT 154.13 million and KZT 194.15 million, respectively.

Halyk Bank of Kazakhstan, with total assets of KZT21,195.6 billion and equity at KZT3,740.9 billion, presents an intriguing investment case despite its high bad loans ratio of 8.3%. The bank trades at a significant discount to its estimated fair value by 64%, offering potential upside for investors seeking undervalued opportunities. While earnings have grown impressively by 20.8% annually over the past five years, future growth is projected to slow to around 4.71% per year amid regulatory challenges and fintech competition impacting margins. Nonetheless, Halyk's strong market position in retail loans and deposits alongside robust digital initiatives could support long-term stability amidst these pressures.

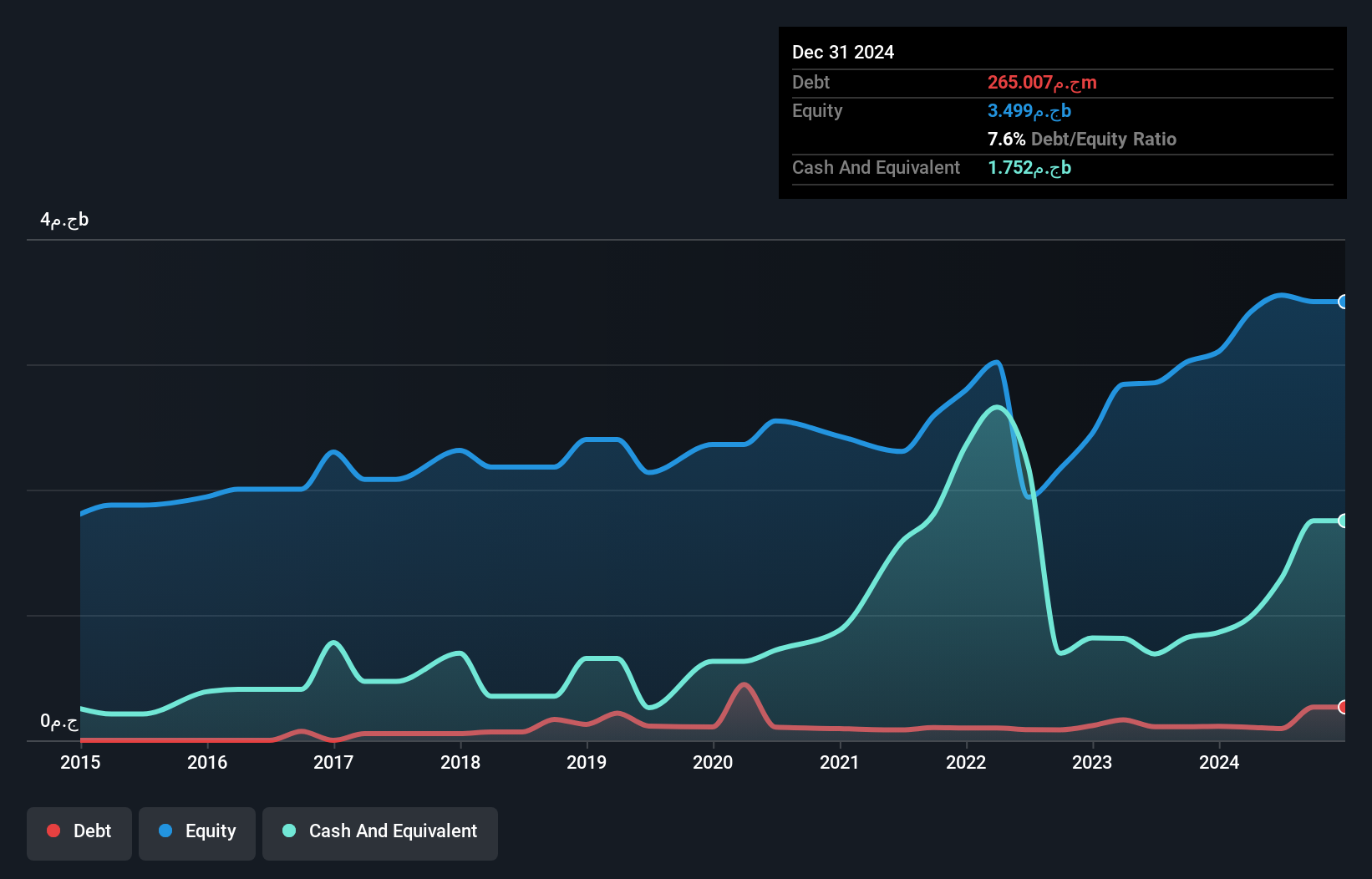

Integrated Diagnostics Holdings (LSE:IDHC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Integrated Diagnostics Holdings plc is a consumer healthcare company that offers medical diagnostics services to patients, with a market capitalization of $301.13 million.

Operations: The company's revenue is primarily derived from two segments: the Walk-In Segment, contributing EGP 2.74 billion, and the Contract Segment, generating EGP 5.60 billion.

Integrated Diagnostics Holdings (IDH) is carving a niche in the healthcare sector, showing robust growth with earnings surging 58% last year, outpacing the industry average of 4.6%. The company is strategically expanding its operations, adding 43 branches in Egypt and boosting radiology services in Saudi Arabia. Despite a debt-to-equity ratio increase from 3.7 to 39.1 over five years, IDH's interest payments are impressively covered at 337 times by EBIT. Trading at a significant discount of about 63% below estimated fair value, IDH continues to offer potential upside with strategic acquisitions and market expansion plans underway.

PayPoint (LSE:PAY)

Simply Wall St Value Rating: ★★★★★☆

Overview: PayPoint plc is a company that provides payments and banking, shopping, and e-commerce services and products in the United Kingdom and New Zealand, with a market capitalization of £354.14 million.

Operations: PayPoint generates revenue primarily from its Love2shop and Pay Point segments, with contributions of £158.23 million and £178.78 million, respectively.

PayPoint's recent performance highlights its promising position in the evolving digital payments landscape, with earnings jumping to £39.33 million from £19.19 million last year and basic EPS rising to £0.591 from £0.266. The company has repurchased 3,032,216 shares for £17.1 million recently, part of a larger buyback initiative totaling 6,923,483 shares for £45 million since June 2024. Trading at a significant discount of 44% below estimated fair value and boasting a reduced debt-to-equity ratio from 260% to 182%, PayPoint shows strong financial health despite challenges like declining traditional retail networks and increasing competition in digital payments.

Turning Ideas Into Actions

- Click this link to deep-dive into the 10 companies within our UK Undiscovered Gems With Strong Fundamentals screener.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com