July 2026's European Undervalued Small Caps With Insider Buying

As geopolitical tensions and energy market volatility continue to impact the European markets, key indices such as the STOXX Europe 600 have faced downward pressure, with notable declines in major stock indexes like Germany's DAX and France's CAC 40. Despite these challenges, moderating inflation rates in countries like Germany and robust consumer spending in regions such as the Netherlands provide a mixed economic backdrop for small-cap stocks. In this environment, identifying promising small-cap opportunities involves looking at companies with strong fundamentals that can navigate current uncertainties while potentially benefiting from insider buying trends.

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| CellaVision | 24.6x | 4.5x | 43.55% | ★★★★★★ |

| Eurocell | 11.3x | 0.3x | 48.83% | ★★★★★☆ |

| Nederman Holding | 17.1x | 0.8x | 36.15% | ★★★★★☆ |

| NoHo Partners Oyj | 16.5x | 0.4x | 35.12% | ★★★★★☆ |

| Close Brothers Group | NA | 0.9x | 41.99% | ★★★★★☆ |

| NCC | 193.8x | 0.3x | 19.73% | ★★★★☆☆ |

| Bilia | 16.2x | 0.3x | 42.00% | ★★★★☆☆ |

| AB Dynamics | NA | 2.2x | 36.35% | ★★★☆☆☆ |

| CVS Group | 52.3x | 1.2x | 47.39% | ★★★☆☆☆ |

| TT Electronics | NA | 0.4x | -4.80% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

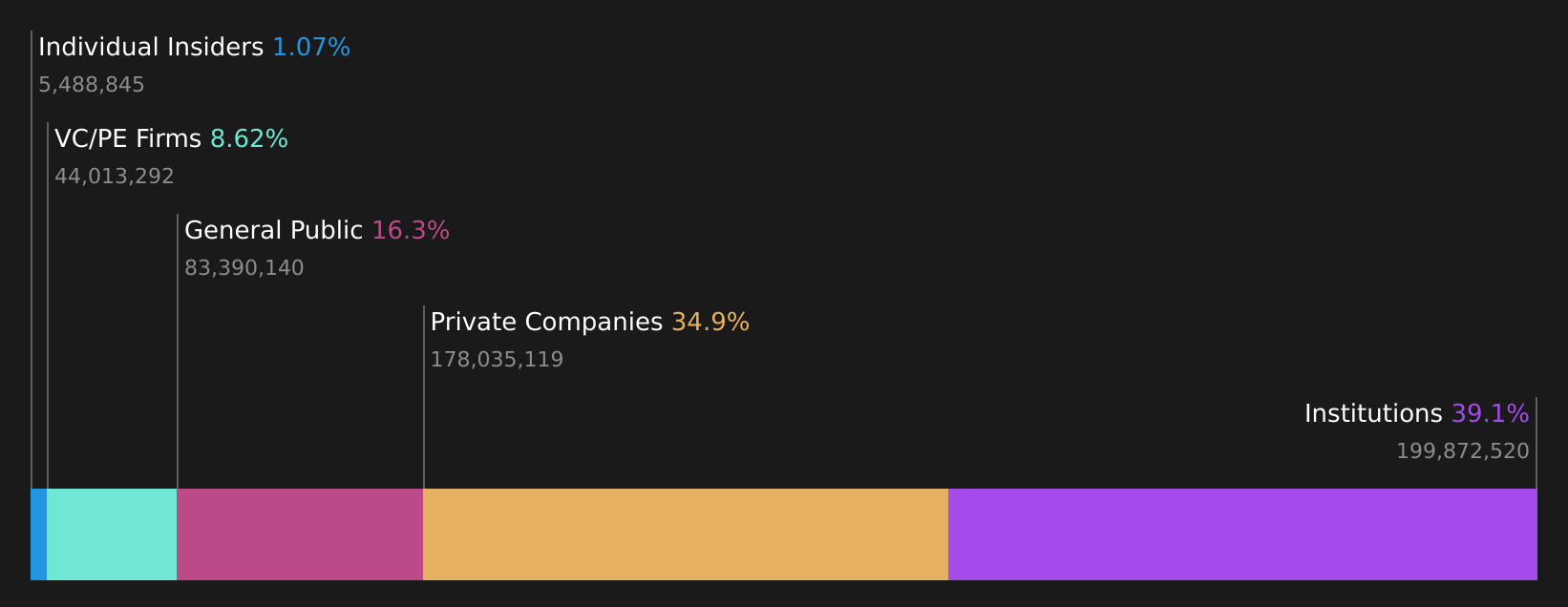

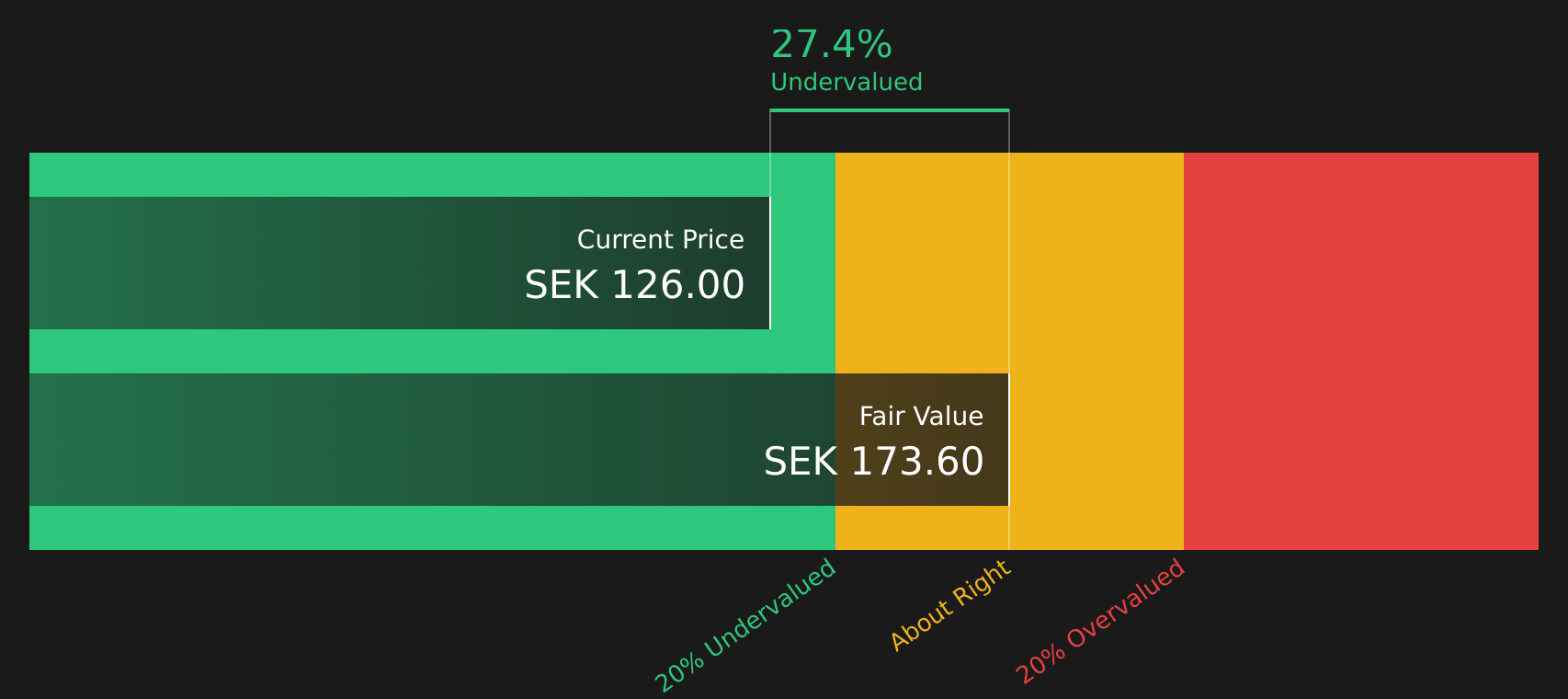

Logistea (OM:LOGI B)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Logistea is a company engaged in the development and management of logistics and industrial properties, with a market capitalization of approximately SEK 2.45 billion.

Operations: Logistea's revenue streams are primarily driven by its operational activities, with a significant focus on maintaining efficient cost management. Over the analyzed periods, the company's gross profit margin has shown notable improvement, reaching 90.30% as of June 2026. This increase in gross profit margin indicates effective control over cost of goods sold relative to revenue generation. Operating expenses have been consistently managed, contributing to the overall profitability and financial health of the company.

PE: 8.2x

Logistea, a European property company, is expanding its portfolio with recent acquisitions in Finland, including properties valued at SEK 145 million and SEK 114 million. Their Q2 earnings showed revenue growth from SEK 263 million to SEK 321 million year-over-year, though net income declined to SEK 106 million. Insider confidence is reflected by a purchase of 35,000 shares by an insider for approximately US$469K in June. Despite relying on external borrowing for funding and forecasted earnings decline of 9.2% annually over three years, Logistea's strategic expansions and refinancing efforts—saving about SEK 45 million annually—indicate potential resilience amidst financial challenges.

- Click to explore a detailed breakdown of our findings in Logistea's valuation report.

Examine Logistea's past performance report to understand how it has performed in the past.

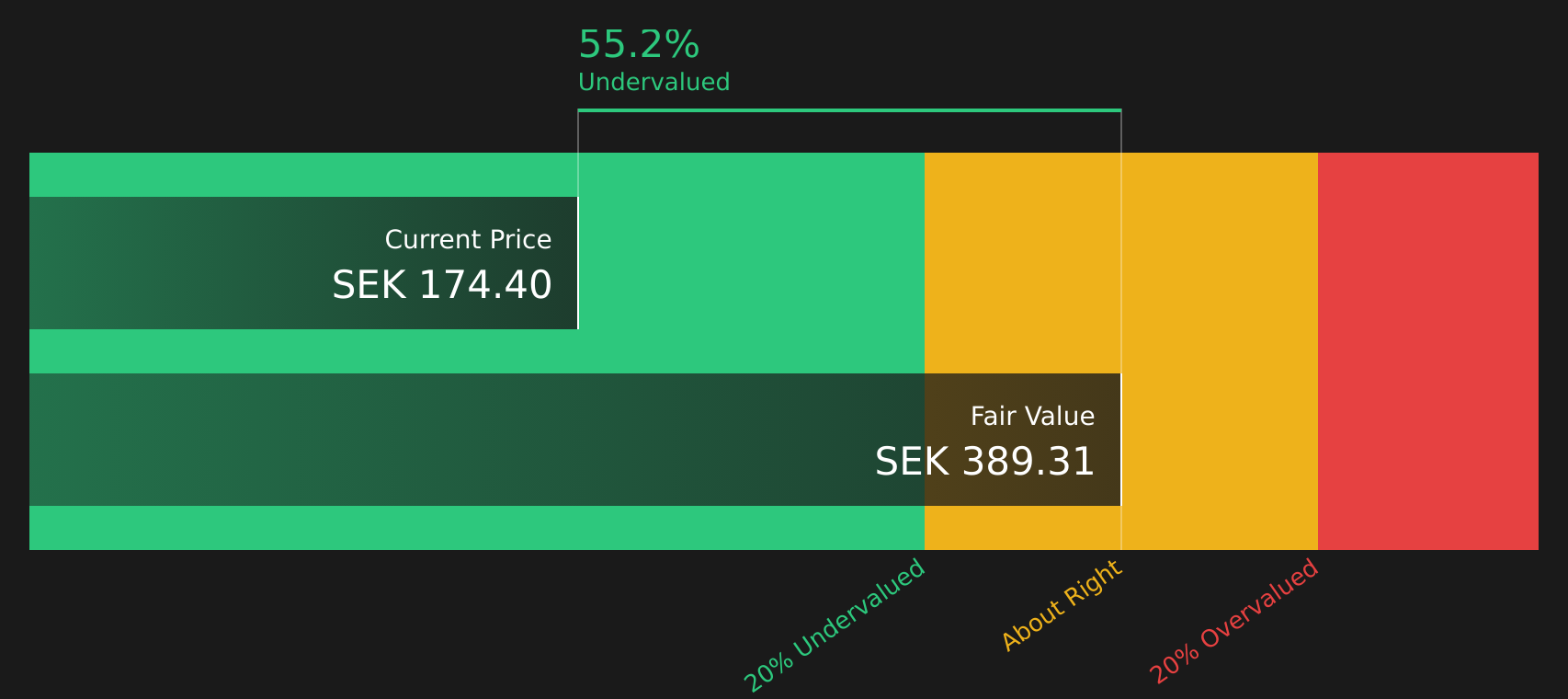

Nederman Holding (OM:NMAN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Nederman Holding specializes in providing solutions for industrial air filtration and environmental technology, with a market cap of approximately SEK 4.48 billion.

Operations: Nederman Holding's revenue streams are primarily derived from Extraction & Filtration Technology, which contributes SEK 2.61 billion, followed by Process Technology at SEK 1.60 billion. The company has seen fluctuations in its gross profit margin, with a recent figure of 39.71%. Operating expenses are significant, with Sales & Marketing being the largest component, reaching SEK 1.13 billion recently.

PE: 17.1x

Nederman Holding, a company focusing on industrial air filtration, shows potential as an undervalued European small cap. Despite recent challenges with declining sales and net income in Q1 2026, insider confidence is evident with Tomas Hagström's purchase of 4,414 shares valued at SEK 518,144 between April and June. The company's earnings are projected to grow by 18.22% annually. However, reliance on external borrowing for funding poses risks. Recent leadership changes may influence future strategic directions positively.

- Click here and access our complete valuation analysis report to understand the dynamics of Nederman Holding.

Understand Nederman Holding's track record by examining our Past report.

RaySearch Laboratories (OM:RAY B)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: RaySearch Laboratories is a healthcare technology company specializing in the development of advanced software solutions for radiation therapy, with a market capitalization of approximately SEK 3.51 billion.

Operations: The company generates revenue primarily from healthcare software, with a notable gross profit margin of 92.41% as of March 2026. Operating expenses are significant, driven by sales and marketing, research and development, and general administrative costs.

PE: 35.4x

RaySearch Laboratories, a European company known for its advanced oncology software solutions, is gaining attention in the investment community as a potentially undervalued player. Recent insider confidence was demonstrated by Gunther Marder purchasing 12,115 shares worth SEK 2.75 million in early July 2026. This move suggests belief in the company's future prospects amidst ongoing product innovations and strategic client expansions across Asia and Europe. Earnings are forecast to grow at over 21% annually, although reliance on external borrowing poses higher risk factors. Recent releases like RayCare v2026 and RayIntelligence v2026 highlight their commitment to improving cancer care efficiency through enhanced interoperability and data-driven insights.

- Delve into the full analysis valuation report here for a deeper understanding of RaySearch Laboratories.

Evaluate RaySearch Laboratories' historical performance by accessing our past performance report.

Taking Advantage

- Take a closer look at our Undervalued European Small Caps With Insider Buying list of 58 companies by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com