YesAsia Holdings And 2 Other Promising Asian Penny Stocks

Amidst renewed geopolitical tensions and fluctuating energy prices, Asian markets have been navigating a complex landscape that has impacted investor sentiment across various sectors. The term 'penny stocks' might feel like a relic of past market eras, but the potential they represent is as real as ever. These smaller or newer companies often offer affordability and growth potential when supported by strong financials, providing investors with opportunities to uncover hidden value in quality stocks.

Let's review some notable picks from our screened stocks.

YesAsia Holdings (SEHK:2209)

Simply Wall St Financial Health Rating: ★★★★★☆

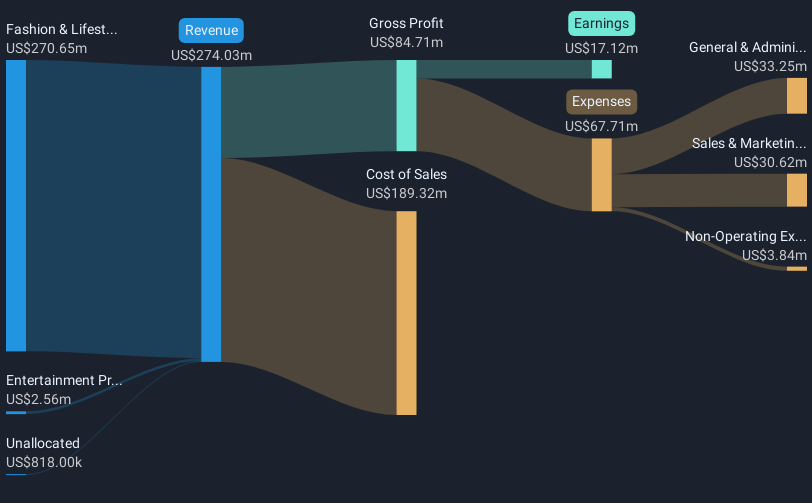

Overview: YesAsia Holdings Limited is an investment holding company involved in trading Asian fashion and lifestyle, beauty, cosmetics, accessories, and entertainment products with a market cap of HK$1.14 billion.

Operations: The company generates revenue through two main segments: B2B, contributing $148.89 million, and B2C, accounting for $349.33 million.

Market Cap: HK$1.14B

YesAsia Holdings, with a market cap of HK$1.14 billion, shows strong financial health and growth potential within the penny stock sector. The company has demonstrated robust earnings growth, averaging 40.9% annually over five years, although recent growth of 21.8% is slower than this average. Its EBIT covers interest payments 18.9 times over, and it maintains more cash than total debt, indicating sound debt management. Despite a slight decline in net profit margins from 5.5% to 4.6%, its price-to-earnings ratio of 6.3x suggests good value compared to the Hong Kong market average of 11.5x.

- Navigate through the intricacies of YesAsia Holdings with our comprehensive balance sheet health report here.

- Evaluate YesAsia Holdings' prospects by accessing our earnings growth report.

China Yongda Automobiles Services Holdings (SEHK:3669)

Simply Wall St Financial Health Rating: ★★★★★☆

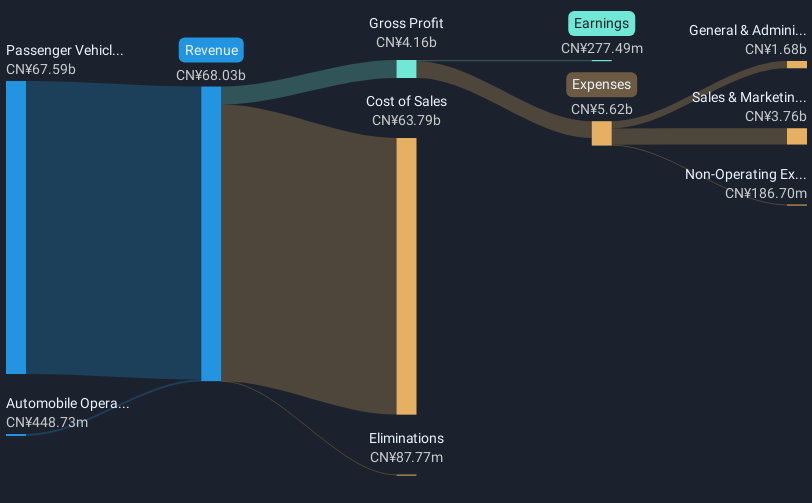

Overview: China Yongda Automobiles Services Holdings Limited is an investment holding company involved in the retail of passenger vehicles in the People’s Republic of China, with a market cap of HK$1.52 billion.

Operations: The company's revenue is primarily derived from Passenger Vehicle Sales and Services, generating CN¥54.27 billion, and Automobile Operating Lease Services, contributing CN¥372.11 million.

Market Cap: HK$1.52B

China Yongda Automobiles Services Holdings, with a market cap of HK$1.52 billion, operates in the passenger vehicle segment in China. Despite being unprofitable and facing increased losses over five years, its short-term assets surpass both short- and long-term liabilities, indicating solid liquidity management. The company’s debt-to-equity ratio has improved significantly from 83.3% to 35%, reflecting better financial leverage over time. However, its negative return on equity and inability to cover interest payments with EBIT highlight ongoing profitability challenges. Recent executive changes may impact strategic direction as Mr. Cai Yingjie resigned as Vice-chairman effective June 26, 2026.

- Click here and access our complete financial health analysis report to understand the dynamics of China Yongda Automobiles Services Holdings.

- Understand China Yongda Automobiles Services Holdings' earnings outlook by examining our growth report.

ZG Group (SEHK:6676)

Simply Wall St Financial Health Rating: ★★★★★☆

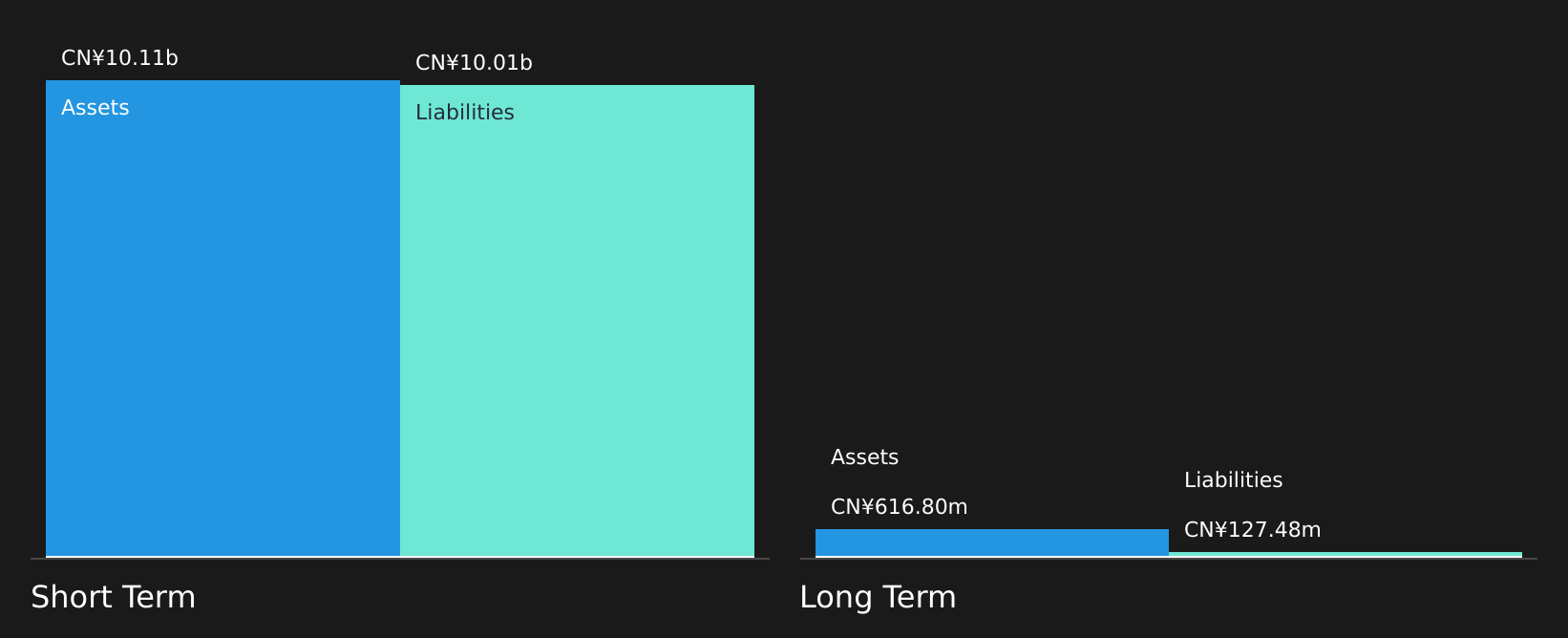

Overview: ZG Group operates a digital platform facilitating third-party steel transactions across Mainland China, the United Arab Emirates, Hong Kong, Malaysia, Korea, and internationally with a market cap of HK$653.09 million.

Operations: ZG Group's revenue is primarily derived from Transaction Services (CN¥635.06 million), Transaction Support Services (CN¥489.62 million), Overseas Transaction Business (CN¥1.02 billion), Non-steel Transaction Business (CN¥321.52 million), and Technology Subscription Services (CN¥30.72 million).

Market Cap: HK$653.09M

ZG Group, with a market cap of HK$653.09 million, operates a digital platform for steel transactions across several regions. Despite being unprofitable and experiencing increased losses over the past five years, the company maintains strong liquidity as short-term assets (CN¥10.1 billion) exceed both short- and long-term liabilities. Its net debt to equity ratio is satisfactory at 34.6%, indicating manageable leverage, while a positive free cash flow supports a cash runway exceeding three years. Recent proposed changes to its articles of association aim to align with regulatory updates, pending shareholder approval at the upcoming annual meeting.

- Jump into the full analysis health report here for a deeper understanding of ZG Group.

- Gain insights into ZG Group's historical outcomes by reviewing our past performance report.

Where To Now?

- Explore the 1,072 names from our Asian Penny Stocks screener here.

- Seeking Other Investments? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com