Undiscovered Gems in Global Markets July 2026

As global markets navigate through the complexities of Middle East tensions and fluctuating energy prices, investors have witnessed mixed performances across major indices, with small-cap stocks like those in the Russell 2000 experiencing a slight decline. Amidst this backdrop, identifying undiscovered gems in the market involves looking for companies that can thrive despite geopolitical uncertainties and demonstrate resilience through innovative strategies or niche market positions.

Top 10 Undiscovered Gems With Strong Fundamentals Globally

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| Transcend Information | NA | 4.45% | 25.56% | ★★★★★★ |

| Nippon Carbide Industries | 16.74% | 1.99% | -4.81% | ★★★★★★ |

| Base | NA | 11.66% | 17.63% | ★★★★★★ |

| GROUPE SFPI | 18.02% | 4.25% | -29.76% | ★★★★★★ |

| Flügger group | 16.02% | -0.54% | -12.69% | ★★★★★☆ |

| Fourth Milling | NA | 8.33% | 16.85% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

| Regina Miracle International (Holdings) | 132.81% | 0.48% | -15.87% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

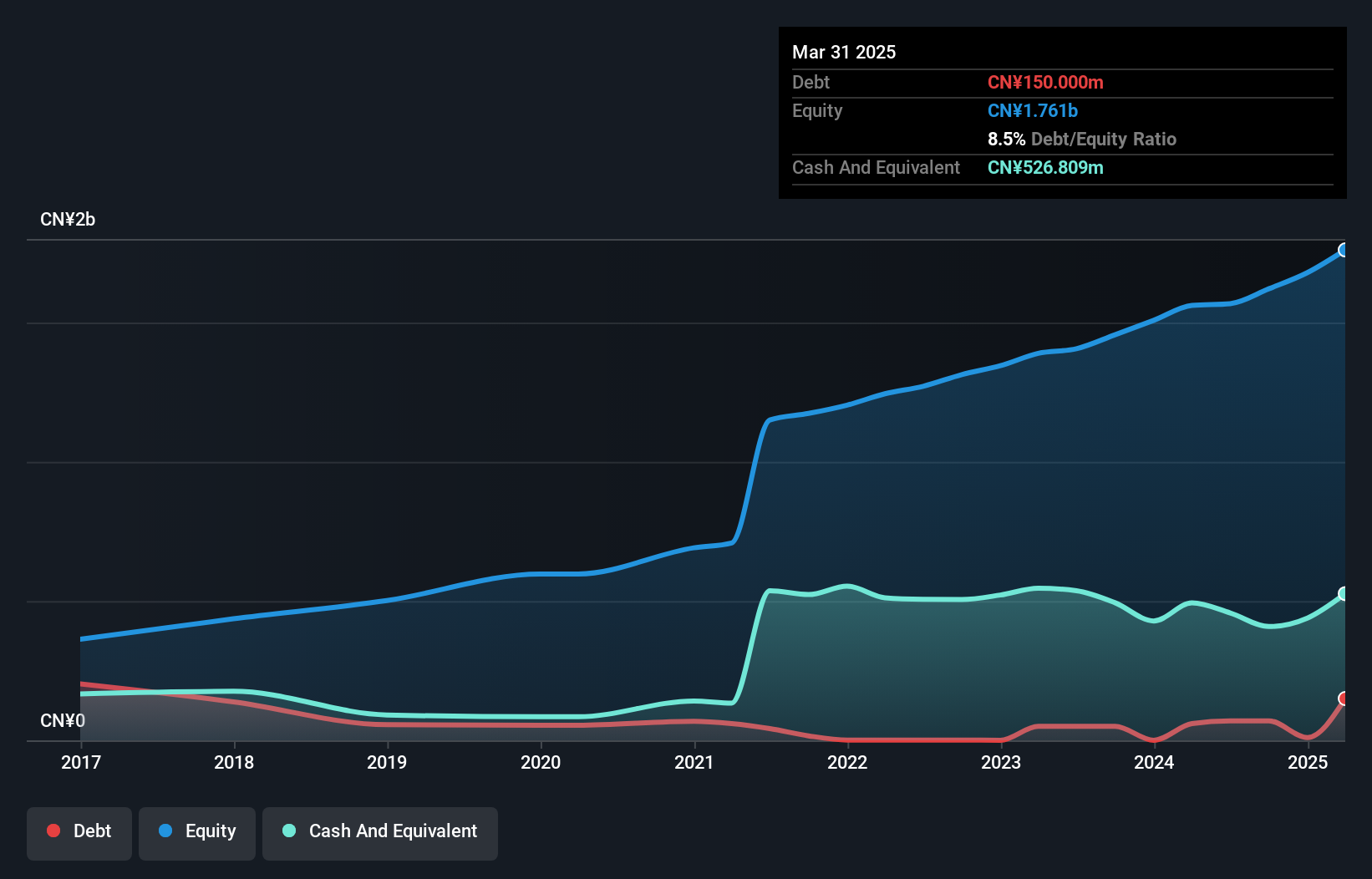

Shandong Bailong Chuangyuan Bio-Tech (SHSE:605016)

Simply Wall St Value Rating: ★★★★★☆

Overview: Shandong Bailong Chuangyuan Bio-Tech Co., Ltd. operates in the biotechnology sector and has a market cap of approximately CN¥9.67 billion.

Operations: Bailong Chuangyuan generates revenue primarily through its biotechnology products. The company has a market cap of approximately CN¥9.67 billion.

Shandong Bailong Chuangyuan Bio-Tech has been making waves with its recent performance, showing a net income of CNY 120.59 million for the first quarter of 2026, up from CNY 81.42 million the previous year. This growth is supported by sales reaching CNY 392.61 million compared to last year's CNY 313.3 million, highlighting robust operational momentum. Despite an increased debt-to-equity ratio from 8.5% to 22.2% over five years, the company seems well-positioned financially with more cash than total debt and trades at nearly a quarter below estimated fair value, suggesting potential upside in valuation terms.

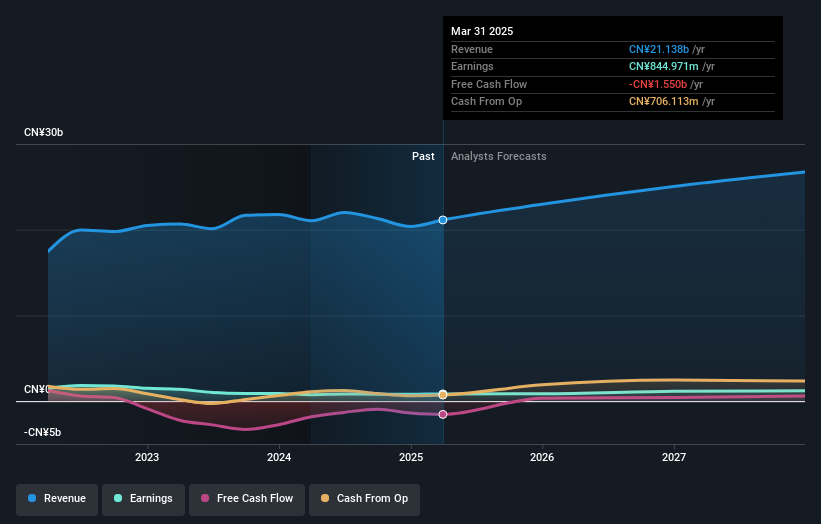

Chengdu Wintrue Holding (SZSE:002539)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Chengdu Wintrue Holding Co., Ltd. focuses on the research, development, production, and sale of compound fertilizers with a market cap of CN¥12.28 billion.

Operations: The company generates revenue primarily from the sale of compound fertilizers. It has a market capitalization of CN¥12.28 billion.

Chengdu Wintrue Holding, a smaller player in its field, is catching attention with its robust financials. The company reported a net income of CNY 827.08 million for 2025, up from CNY 804.47 million the previous year, alongside sales growth to CNY 21.37 billion from CNY 20.34 billion. Despite a high net debt to equity ratio of 111%, their interest payments are comfortably covered by EBIT at seven times coverage, indicating strong operational performance. With basic earnings per share rising to CNY 0.69 from CNY 0.67 and trading significantly below estimated fair value, Chengdu Wintrue seems poised for potential growth amidst industry peers.

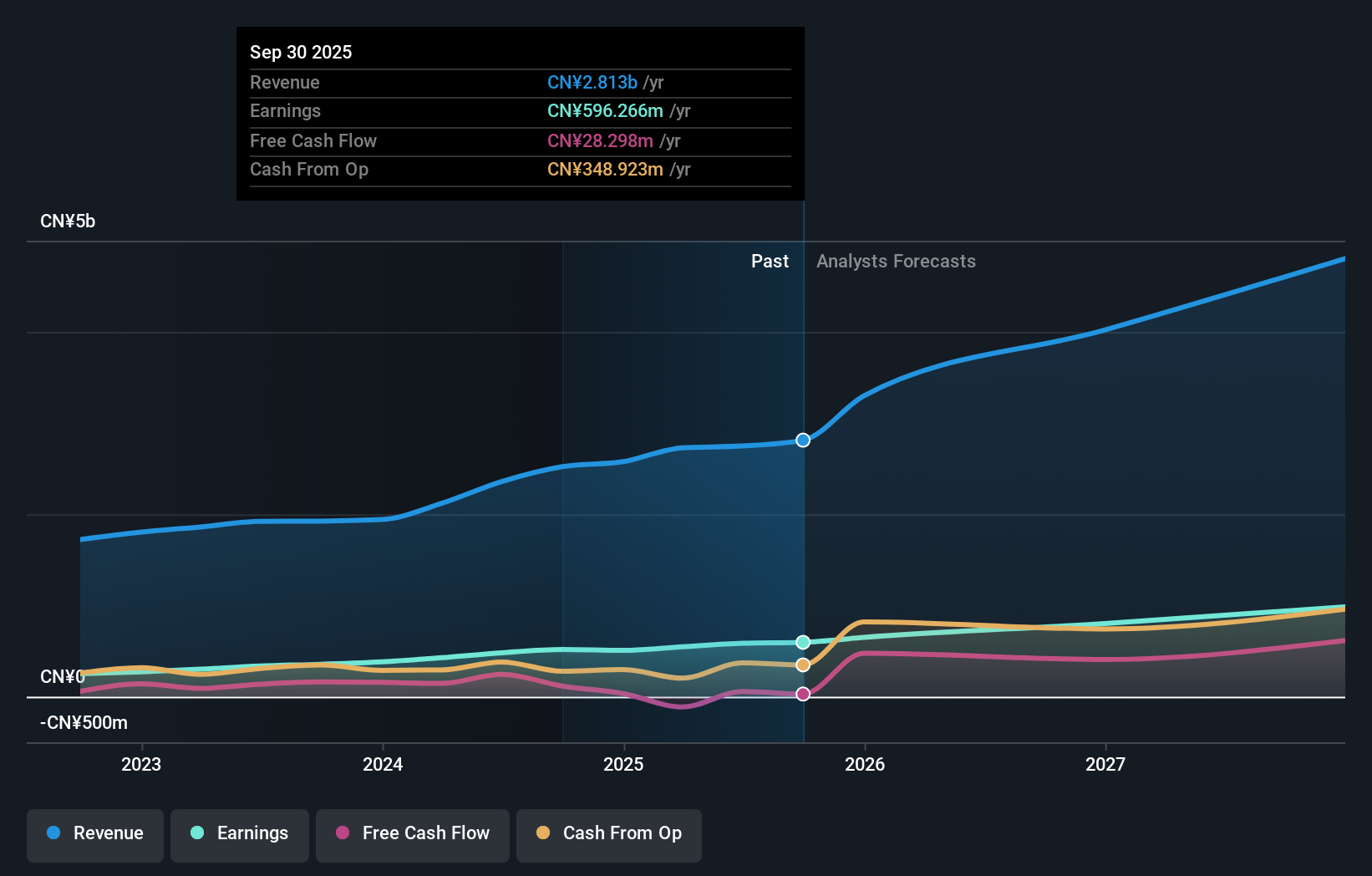

Zhejiang Jolly PharmaceuticalLTD (SZSE:300181)

Simply Wall St Value Rating: ★★★★★☆

Overview: Zhejiang Jolly Pharmaceutical Co., LTD focuses on the research, production, and marketing of Chinese medicinal products both domestically and internationally, with a market cap of CN¥9.33 billion.

Operations: Zhejiang Jolly Pharmaceutical generates revenue primarily from the sale of Chinese medicinal products. The company's cost structure includes production and marketing expenses, which influence its net profit margin.

Zhejiang Jolly Pharmaceutical, a relatively smaller player in the pharmaceutical sector, has shown promising growth with earnings up 19% over the past year, outpacing the industry's -1.6%. The company reported net income of CNY 631.93 million for 2025, an increase from CNY 507.77 million the previous year, and basic earnings per share rose to CNY 0.92 from CNY 0.73. Its debt situation seems manageable with a net debt to equity ratio at a satisfactory level of 0.7%, and interest payments are well covered by EBIT at an impressive 65.7 times coverage, indicating robust financial health and potential for continued performance improvement in its niche market space.

Key Takeaways

- Click here to access our complete index of 151 Global Undiscovered Gems With Strong Fundamentals.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com