SBI Shinsei Bank (TSE:8303) Could Be 18% Undervalued As Dividend Reset Raises Questions

SBI Shinsei Bank (TSE:8303) is back in focus after announcing a lower year-end dividend for the fiscal year ended March 2026, citing a prior two-for-one stock split and confirming a sizeable share buyback program.

See our latest analysis for SBI Shinsei Bank.

At a share price of ¥1,449.0, SBI Shinsei Bank has seen short-term share price returns drift, with the 90 day share price return down 13.05% and the year to date share price return down 17.15%, while the 3 year total shareholder return is down 93.84% and the 5 year total shareholder return is down 88.06%. This points to sentiment that remains cautious despite the new mix of dividends and buybacks.

If this kind of capital return reset has you reassessing your options, it could be a good moment to broaden your watchlist with the 12 top founder-led companies

SBI Shinsei Bank now pairs a reduced headline dividend with a sizeable buyback and a long run of weak shareholder returns. At ¥1,449, does the current valuation still leave more upside than downside for new buyers?

Preferred P/E of 11.3x for SBI Shinsei Bank: Is it justified?

SBI Shinsei Bank trades on a P/E of 11.3x, which sits below both its peer group and the wider JP banks industry, even after a long stretch of weak shareholder returns.

The P/E multiple compares the current share price to earnings per share and is a simple way of seeing how much investors are paying for each unit of profit. For a bank like SBI Shinsei Bank, it effectively reflects how the market is weighing its earnings profile against sector peers that often face similar regulatory and interest rate conditions.

Here, the stock is described as good value on several fronts. Its 11.3x P/E is below the JP Banks industry average of 15.7x, and also below the peer average of 16.2x. In addition, it is assessed as good value versus an estimated fair P/E of 13.5x, which is a level the market could potentially move toward if sentiment and earnings expectations aligned more closely with that fair ratio assessment.

Compared with industry and peer benchmarks, SBI Shinsei Bank’s lower P/E suggests the market is pricing its earnings at a discount to similar banks, despite assessments that it is trading at good value relative to both those groups and to the estimated fair P/E level. Explore the SWS fair ratio for SBI Shinsei Bank

Result: Price-to-earnings of 11.3x (UNDERVALUED)

However, SBI Shinsei Bank still faces questions about its declining annual revenue and the long period of weak shareholder returns, which could keep sentiment cautious.

Find out about the key risks to this SBI Shinsei Bank narrative.

Another View on SBI Shinsei Bank’s Value

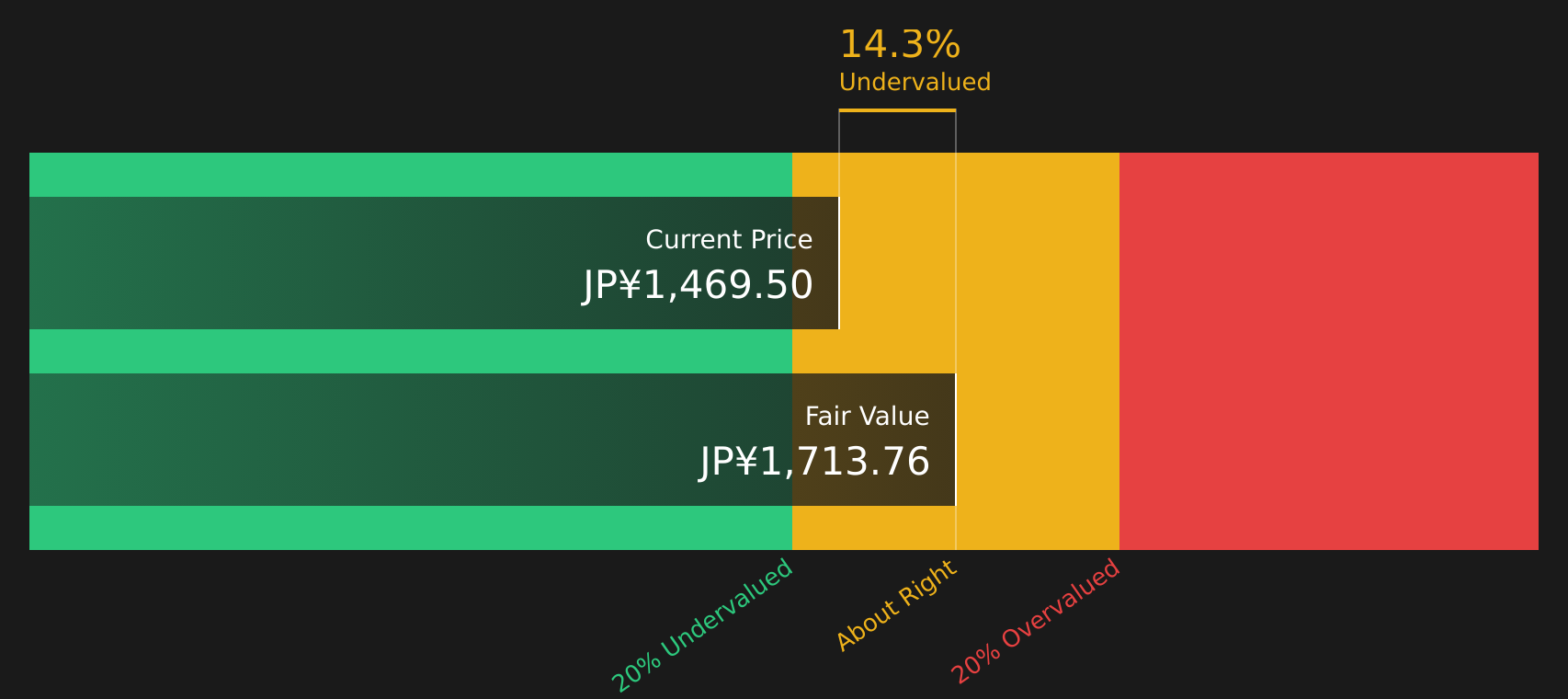

While the P/E comparison paints SBI Shinsei Bank as cheap against peers, the SWS DCF model also suggests the stock is undervalued, with a fair value estimate of ¥1,713.56 versus the current ¥1,449. If both earnings and cash flow views point to value, what is the market still worried about?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SBI Shinsei Bank for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 19 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mix of concerns and potential rewards around SBI Shinsei Bank, you may want to move quickly and review the underlying data yourself, then weigh up the 4 key rewards and 2 important warning signs.

Looking for more investment ideas beyond SBI Shinsei Bank?

If SBI Shinsei Bank has sharpened your focus on value and risk, now is the time to widen your search using targeted stock ideas that match your approach.

- Target quality at a discount by checking stocks highlighted in the 19 high quality undervalued stocks.

- Prioritize resilience and sleep easier at night by reviewing companies screened in the 53 resilient stocks with low risk scores.

- Spot potential future standouts early by scanning the screener containing 57 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com