easyJet Stock Draws Attention as Growth and Takeover Interest Collide

With inflation data sending mixed messages across regions and central banks weighing their next moves, many investors are looking for companies that can grow through changing macro conditions rather than relying on a single interest rate or oil price outcome. Fast growing stocks with high insider ownership can be one way to align with management teams that have significant skin in the game while still targeting strong business expansion. This article looks at the Fast Growing Stocks With High Insider Ownership screener and highlights 3 of the stocks that stand out within it, explaining why they may deserve a closer look.

easyJet (LSE:EZJ)

Overview: easyJet is a low cost European airline based in the UK, carrying passengers across its short haul network while also selling holiday packages through its EasyJet Holidays arm. Alongside core flights, it runs related services such as aircraft maintenance, tour operations and travel extras like insurance.

Operations: easyJet generates about £9.0b from its Airline segment and £2.1b from EasyJet Holidays, partly offset by £0.5b of intergroup eliminations, with the United Kingdom contributing around £5.8b of revenue and the rest coming from France, Switzerland and wider Europe.

Market Cap: £5.0b

easyJet sits at the crossroads of strong earnings forecasts and intense corporate interest, which is why investors are watching closely. Analysts see solid revenue and earnings growth potential, helped by higher margin holiday packages, growing ancillary income and a newer, more efficient fleet. Current profitability and P/E levels are not out of line with the broader UK market. At the same time, the live takeover situation, with Apollo’s preferred cash offer at £7.15 per share and the recent withdrawal of Castlelake, introduces both opportunity and uncertainty around deal terms, EU ownership rules and future capital structure. In addition, exposure to fuel costs, inflation and regulatory decisions on fees makes easyJet a complex case that some investors may wish to scrutinise more closely.

easyJet’s mix of airline earnings, higher margin holidays and a live takeover angle is only half the story. The 3 key rewards and 1 important warning sign might explain what deal terms and capital choices could really mean for shareholders.

Metals Exploration (AIM:MTL)

Overview: Metals Exploration is a London based mining company focused on finding, developing and operating gold and other precious and base metal projects, anchored by its 100% owned Runruno gold project north of Manila in the Philippines.

Operations: Metals Exploration generates approximately US$208.4m in revenue from its Metals & Mining, Gold & Other Precious Metals operations, entirely from the Philippines.

Market Cap: £421,679,985

Metals Exploration may interest you if you are looking for a high growth gold producer with clear project upside but are comfortable with balance sheet and governance questions that still need answering. Earnings have grown 19.6% a year over the past 5 years and revenue is forecast to grow 33.3% a year, supported by the Runruno mine and a new copper gold exploration project at Batong Buhay that brings both scale potential and sizeable spending commitments. A deep discount to one fair value estimate and strong profit margins offset concerns about full reliance on external borrowing, relatively low board independence and very high CEO pay, so the real story here is whether the growth runway and asset quality compensate for those risks.

Metals Exploration’s growth story looks powerful, but the real tension is whether its capital structure and governance are a springboard or a ceiling for that potential. The analysis report for Metals Exploration starts to unpack this before a key twist in the story.

Foresight Group Holdings (LSE:FSG)

Overview: Foresight Group Holdings is a London based asset manager that runs infrastructure, private equity, venture capital and listed funds, with a focus on renewable energy, energy transition projects, social and digital infrastructure, and natural capital across the UK, Europe and Australia. It raises capital from both institutions and retail investors, typically taking meaningful stakes and providing equity and credit to early stage and growth companies.

Operations: Foresight Group Holdings generates about £114.8m from Real Assets and £50.1m from Private Equity, with most revenue coming from the United Kingdom at £126.4m and a smaller but growing contribution of £25.7m from Australia and modest fees from several European markets.

Market Cap: £507.0m

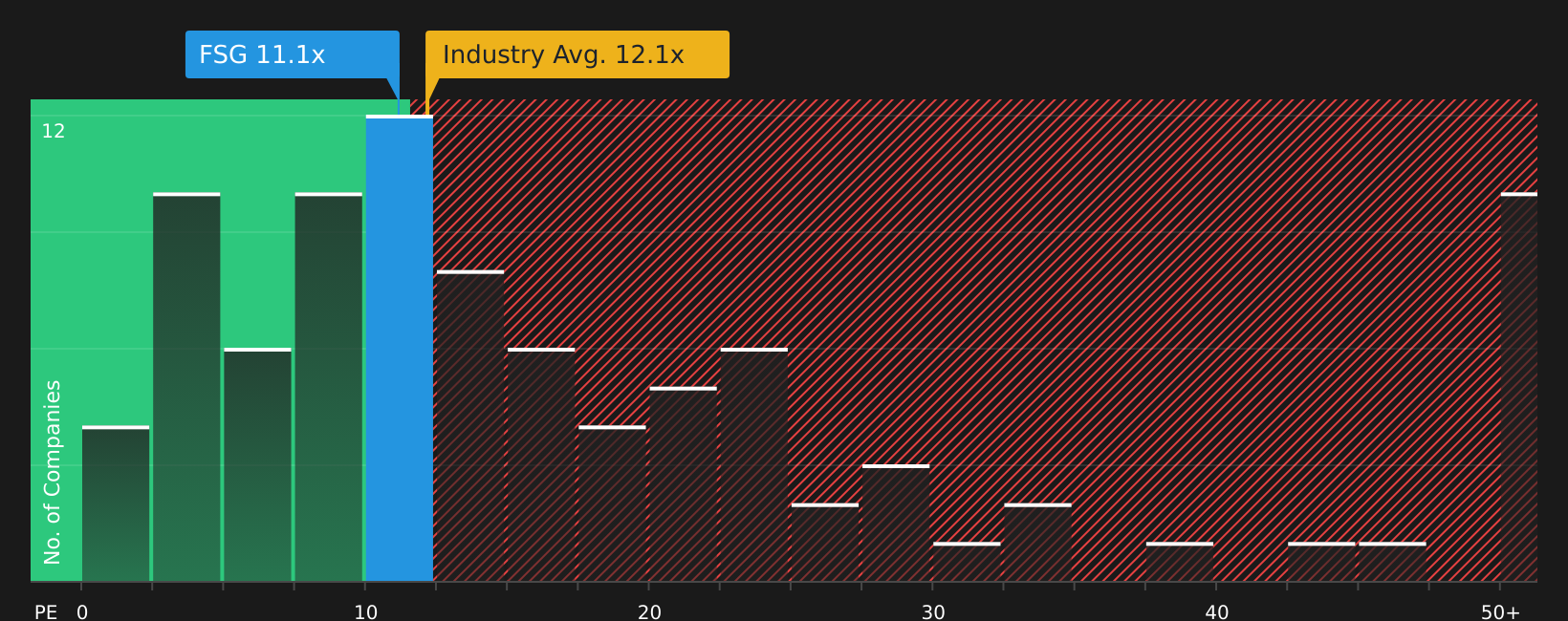

Foresight Group Holdings stands out in this screener because it couples strong earnings quality with a clear plan to grow fee based assets while steadily shrinking the share count through buybacks. Revenue reached £164.9m and net income £42.8m in the latest year, with margins improving as higher fee real assets and private equity strategies scale. Yet the P/E sits below both the UK Capital Markets industry and peer averages. At the same time, rising administrative costs, heavy exposure to UK and European infrastructure policy, and reliance on performance fees mean earnings are not risk free. For investors who like the idea of growing AUM, ongoing buybacks and solid governance, the real question is how these forces play out over the next few years.

Foresight Group Holdings has earnings quality, rising fee income and buybacks all working in its favor, yet the current valuation still looks out of sync. The analysis report for Foresight Group Holdings hints at what the market might be missing next.

The three stocks covered here are only a starting point, and the full Fast Growing Stocks With High Insider Ownership screener surfaces 55 more companies where fast growth potential sits alongside high insider ownership and aligned management incentives. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the opportunities in this theme that best match your own highest conviction ideas.

Take Control of Your Investment Journey

If easyJet or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Do

Fresh stock ideas do not stay under the radar for long, especially when momentum starts building and prices move. Scan these curated picks before the crowd catches on, and consider them before interest broadens.

- Target income potential while avoiding stretched payouts by reviewing companies in the 3 dividend fortresses that aim to keep yields elevated without overextending balance sheets.

- Explore developments in computing by scanning the 26 quantum computing stocks where early movers in advanced hardware and software could influence the sector before expectations fully adjust.

- Review the evolving AI build out by checking the 52 AI infrastructure stocks featuring companies positioned around data centers, chips and networks while this spending trend continues to develop.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com