Is Innovent Biologics (SEHK:1801) Undervalued After Securing China Rights To Verzenios?

Innovent Biologics (SEHK:1801) has drawn fresh attention after securing exclusive commercialization rights for Eli Lilly’s breast cancer drug Verzenios in mainland China. This adds a reimbursed oncology product to its existing portfolio.

See our latest analysis for Innovent Biologics.

The Verzenios agreement lands at a time when Innovent Biologics’ share price has a 30 day share price return of 22.96% and a year to date share price return of 13.83%. Its 3 year total shareholder return of 176.43% contrasts with a more modest 11.36% total shareholder return over one year, hinting that momentum has cooled versus earlier gains.

If this kind of oncology partnership has caught your attention, it could be worth widening your watchlist to see what else is happening across 130 healthcare AI stocks

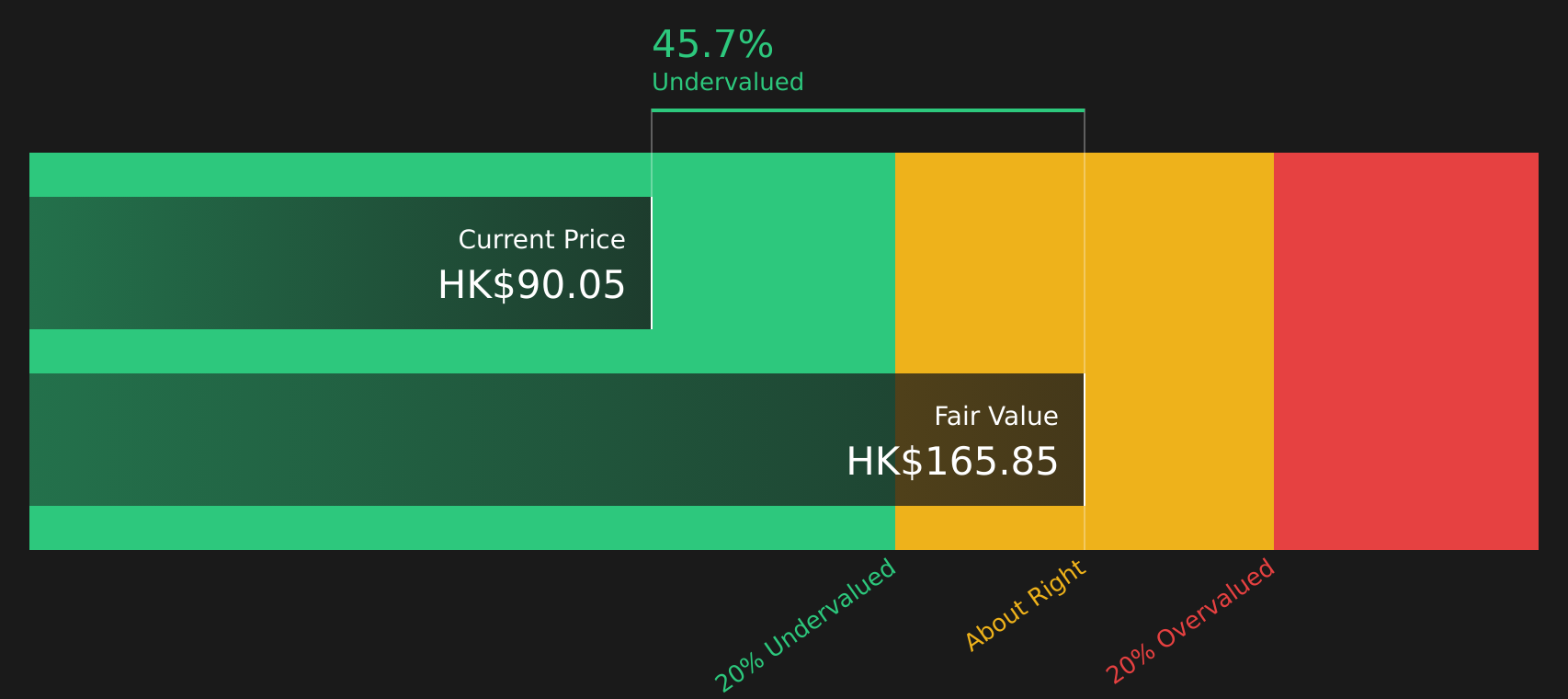

After Innovent Biologics’ recent jump and with the share price sitting at HK$89.70 against analyst and intrinsic estimates pointing higher, the gap between trading price and implied fair value is hard to ignore. How wide is it really?

Preferred Price to Sales Multiple of 10.3x: Is it justified?

On current data, Innovent Biologics looks cheap against several valuation checks, with the share price at HK$89.70 and multiple signals pointing to a discount versus peers, the broader industry and some intrinsic estimates.

The preferred metric here is the price to sales ratio, or P/S, which sits at 10.3x. For a biopharmaceutical company like Innovent Biologics, where reported earnings have only recently turned positive and cash flows can be lumpy, investors often look to P/S because revenue tends to be more stable than earnings and can better reflect the scale of the commercial portfolio.

On that 10.3x P/S, the stock is described as trading at good value relative to both similar companies and the wider Hong Kong Biotechs industry. It is below the peer average P/S of 19.4x and also under the sector average of 11.3x, which suggests the market is pricing Innovent Biologics more cautiously than many comparable biotechs despite its profitable status. The current ratio is also below an estimated fair P/S of 11.2x, a level the market could potentially move towards if sentiment and fundamentals stay aligned with those fair value assumptions.

Explore the SWS fair ratio for Innovent Biologics

Result: Price-to-Sales of 10.3x (UNDERVALUED)

However, the case for Innovent Biologics can weaken quickly if oncology pricing, reimbursement terms, or its newer commercial products fail to support current revenue levels.

Find out about the key risks to this Innovent Biologics narrative.

Another View on Innovent Biologics Using the SWS DCF Model

The P/S of 10.3x suggests Innovent Biologics is on the cheap side, but the SWS DCF model takes a different angle by focusing on estimated future cash flows. On that view, HK$89.70 is 45.7% below an intrinsic value of HK$165.30, which raises a bigger question: is the market underestimating the story, or are the cash flow assumptions too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Innovent Biologics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 212 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Innovent Biologics looking mixed between potential upside and clear uncertainty, it makes sense to move quickly and test the data for yourself. To weigh up both sides of the story, start by reviewing the 5 key rewards and 1 important warning sign

Looking for more investment ideas beyond Innovent Biologics?

If Innovent Biologics has sharpened your focus on opportunities, now is the time to widen your search and benchmark it against other potential ideas.

- Spot potential turnaround stories early by reviewing companies in the 224 elite penny stocks with strong financials before wider attention arrives.

- Target value oriented opportunities by scanning the 212 high quality undervalued stocks that combine quality fundamentals with attractive pricing.

- Prioritise resilience and capital preservation by comparing Innovent Biologics with companies in the 297 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com