How Investors Are Reacting To Brookdale Senior Living (BKD) Rising Occupancy And Debt Refinancing Moves

- Brookdale Senior Living Inc. recently reported that June 2026 consolidated weighted average occupancy reached 82.5%, with quarterly occupancy up 230 basis points year over year to 82.4%, and also refinanced a portion of its 2027 debt while expanding and extending its revolving credit facility.

- An interesting insight is that June produced Brookdale’s highest monthly net move-ins so far in 2026, suggesting that operational initiatives may be gaining traction in filling its communities.

- With June’s occupancy gains now in hand, we’ll explore how this operational momentum could influence Brookdale’s existing investment narrative.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

Brookdale Senior Living Investment Narrative Recap

To own Brookdale, you need to believe that steadily improving occupancy and tighter operations can translate into sustainable earnings from a still‑leveraged balance sheet. The June and Q2 2026 occupancy gains support that near term occupancy remains the key catalyst, while high leverage and refinancing needs stay the central risk. The recent refinancing and facility expansion help address near term debt timing, but do not fully remove balance sheet concerns.

The July 6 refinancing announcement is particularly relevant here, since it extends a portion of 2027 mortgage maturities out to 2036 and expands Brookdale’s revolving credit capacity to up to US$200,000,000 through 2029. That added runway may give the company more time to benefit from occupancy improvements before larger maturities come due, which matters if you see operational momentum as the main driver of the thesis.

Yet even with rising occupancy, investors should be aware that Brookdale’s elevated leverage and refinancing needs could still...

Read the full narrative on Brookdale Senior Living (it's free!)

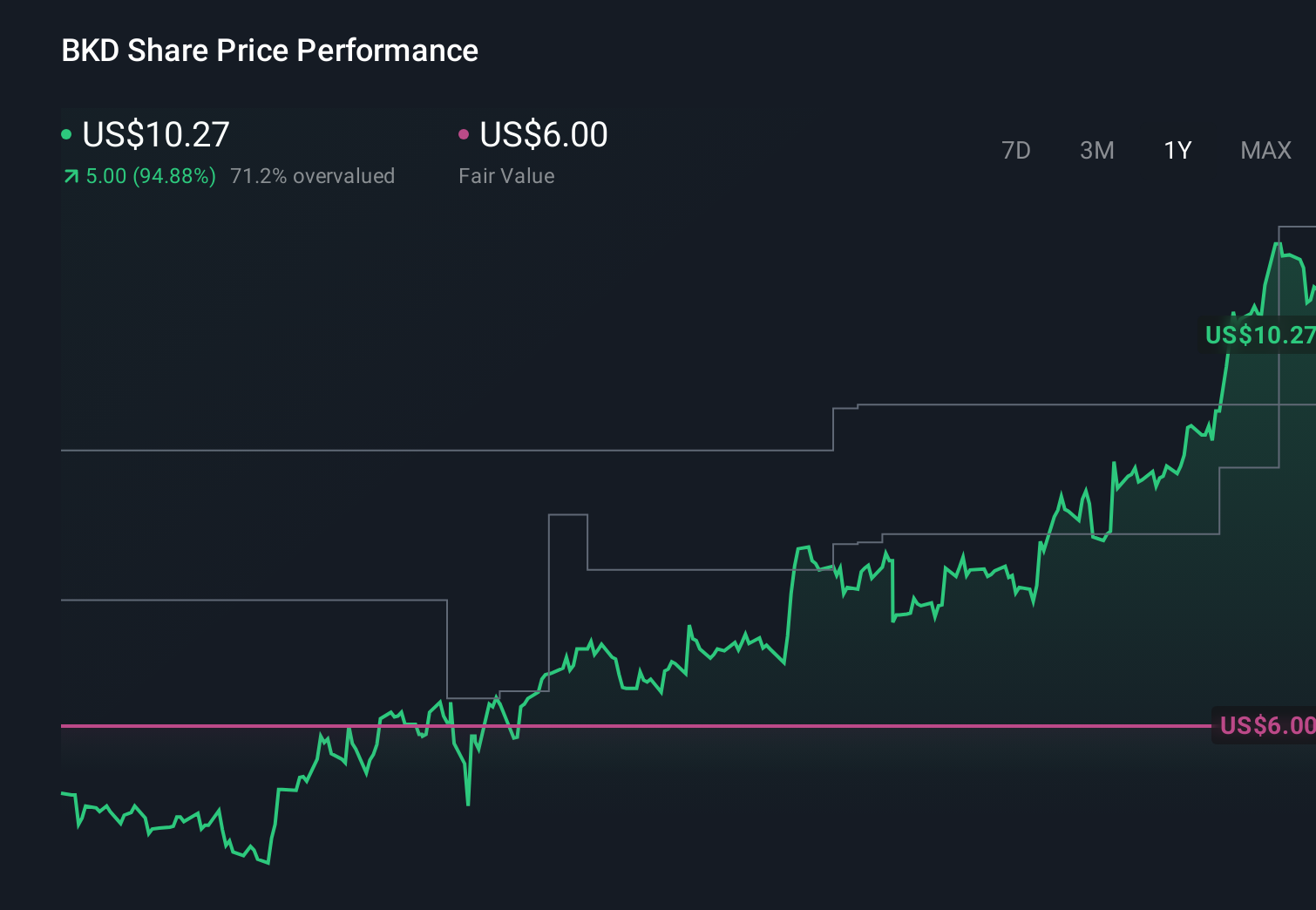

Brookdale Senior Living's narrative projects $3.2 billion revenue and $103.7 million earnings by 2029. This requires 2.6% yearly revenue growth and a $308.3 million earnings increase from -$204.6 million today.

Uncover how Brookdale Senior Living's forecasts yield a $19.58 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were projecting revenue of about US$3.3 billion and earnings near US$125 million by 2029, yet they still flagged risks like tech enabled alternatives capping occupancy and pricing power. If you only focus on June’s occupancy bump and new debt terms, you might miss how different these more pessimistic assumptions are and why it is worth comparing several viewpoints before deciding what you believe.

Explore 2 other fair value estimates on Brookdale Senior Living - why the stock might be worth as much as 11% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Brookdale Senior Living research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Brookdale Senior Living research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Brookdale Senior Living's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com