Mycronic (OM:MYCR) Lands A New SLX Order, Is The Upside Already Priced In?

Mycronic (OM:MYCR) announced a new SLX mask writer order from an existing customer in Asia, valued between US$5 million and US$7 million. Delivery is planned for the third quarter of 2026.

See our latest analysis for Mycronic.

The new SLX order lands at a time when Mycronic’s share price has climbed to SEK296.8, with a 90 day share price return of 24.71% and a 3 year total shareholder return of 156.00%. This points to momentum that has built steadily rather than in a single spike.

If this kind of demand story has your attention, it could be a good moment to look at other semiconductor related opportunities through our screener of 52 AI infrastructure stocks

After a strong 3 year run and a fresh SLX order under its belt, the real tension around Mycronic now is simple: does the current price still leave enough upside to justify the risks you are taking on?

Most Popular Narrative: 14% Overvalued

On the most followed valuation narrative, Mycronic’s fair value of SEK260.25 sits below the last close at SEK296.8, which puts the new SLX order into sharper context.

The analysts have a consensus price target of SEK260.25 for Mycronic based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK315.0, and the most bearish reporting a price target of just SEK176.0.

Want to see what kind of revenue path and margin profile need to line up for that fair value? The narrative leans heavily on growth, profitability and a premium earnings multiple.

Result: Fair Value of SEK260.25 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if tariffs continue to disrupt High Flex orders or a few key Global Technologies customers pull back, the current Mycronic narrative could quickly appear overly optimistic.

Find out about the key risks to this Mycronic narrative.

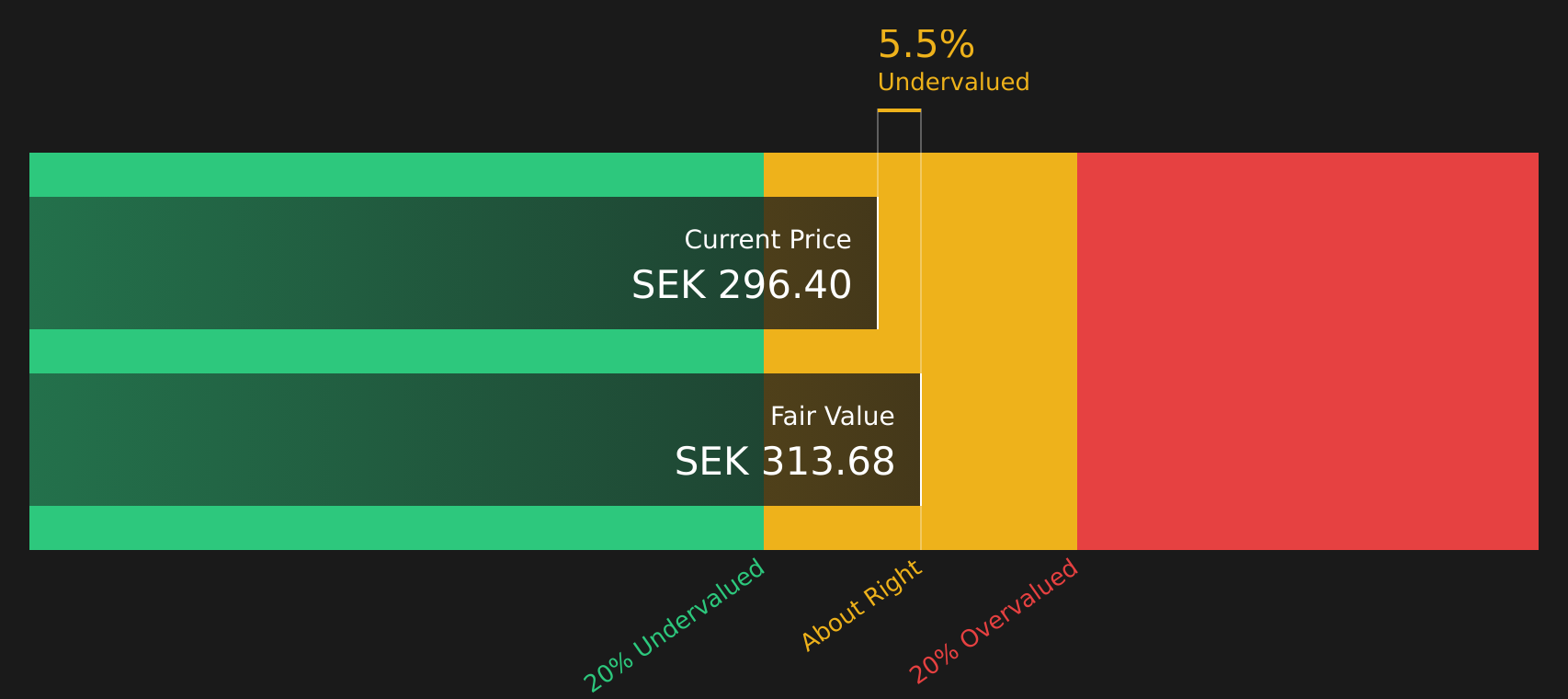

Another View: Mycronic Through The SWS DCF Lens

While the popular narrative has Mycronic trading about 14% above a SEK260.25 fair value, the Simply Wall St DCF model tells a different story. At SEK296.8, the stock is priced roughly 5.5% below an intrinsic value estimate of SEK314.05, which points to a modest cushion instead of a premium.

The gap between a higher P/E based target and a slightly undervalued DCF outcome leaves you with a clear question: Which set of assumptions about growth, margins and risk feels more realistic for Mycronic given what you know about the business and its order pipeline?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mycronic for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 213 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and caution around Mycronic resonates with you, do not wait too long to weigh the evidence yourself and see how the balance of risks and rewards sits for your portfolio, starting with the 2 key rewards and 1 important warning sign

Looking for more investment ideas beyond Mycronic?

If Mycronic has sharpened your interest, do not stop here. Broaden your watchlist with other focused ideas that could suit different roles in your portfolio.

Use these targeted stock lists on Simply Wall St to quickly surface opportunities that match what you care about most.

- Target future compounding potential by scanning companies that look attractively priced relative to their fundamentals using the 213 high quality undervalued stocks.

- Strengthen your income stream by finding companies that pair higher yields with resilience through the 471 dividend fortresses.

- Protect your downside by focusing on companies with sturdier finances and steadier risk profiles using the 292 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com