China Index Research Institute: The core city “Xiaoyangchun” market continued in April, and second-hand housing market expectations improved

The Zhitong Finance App learned that the China Index Research Institute released a report saying that in April 2026, the “Xiaoyangchun” market in core cities continued, and second-hand housing transactions in key cities such as Beijing and Shanghai continued to increase year-on-year, reflecting that demand continues to be released and market expectations have improved. The decline in second-hand housing prices in the top ten cities was narrower than last month, and Shanghai maintained an upward trend from month to month. Looking at the trend, second-hand housing transactions in core cities are expected to remain active, and prices are expected to continue to fluctuate slightly. The current demand release is still mainly price-driven. The basis for market repair is not yet strong. The continued improvement of the market still depends on improvements in residents' expectations, and differentiation will continue to be the main characteristic of the market throughout the year.

At the policy level, on April 28, the Politburo meeting of the Central Committee stated that “efforts should be made to stabilize the real estate market and solidly push forward urban renewal.” On April 16, the Ministry of Finance and the Ministry of Housing and Construction issued the “Notice on Launching the 2026 Central Financial Support Urban Renewal Action”, which plans to grant subsidies to no more than 15 cities implementing urban renewal actions. The total amount of subsidies for each city in the East, Central, and Western regions shall not exceed 800 million yuan, 1 billion yuan, and 1.2 billion yuan, respectively. On April 22, 15 departments including the Communist Youth League and the National Development and Reform Commission issued a document introducing a number of measures to guarantee housing for young people. On April 24, a spokesperson for the Legal Working Committee of the Standing Committee of the National People's Congress introduced this year's key legislative work and stated that the Urban Real Estate Management Law will be revised; on the same day, the Ministry of Finance and the National Development and Reform Commission issued the “Notice on Expanding the Scope of the “Self-Audit and Spontaneous” Pilot for Local Government Special Bond Projects, clarifying that Hebei Province, Jiangxi Province, Hubei Province, and Chongqing will be included in the scope of the “self-examination and spontaneous” pilot for local government special bond projects, expanding the scope to 14 provinces and cities.

At the local level, Shenzhen has optimized policies to increase purchase restrictions on Futian, Nanshan and Baoan Xin'an streets, while increasing personal and household loan amounts. Households can borrow up to 3.51 million yuan. Updated relevant documents in cities such as Changsha, Chengdu, and Wuhan. Zhuhai, Tianjin, Guangzhou and other places have implemented relevant policies to revitalize stocks. Among them, Guangzhou explores industrial and commercial land renewal policies and formulates supporting rules. Many places such as Wuhan, Nanjing, Jinan, and Qingdao have optimized their provident fund loan policies. Among them, Nanjing has expanded the scope of offsite loans to all of Anhui Province, and Jinan and Qingdao have expanded the use of provident fund withdrawals to pay property fees, pay deeds, and use in urban renewal. Also, in April, Fujian issued about 12.9 billion yuan of special bonds to collect and buy unused land stocks.

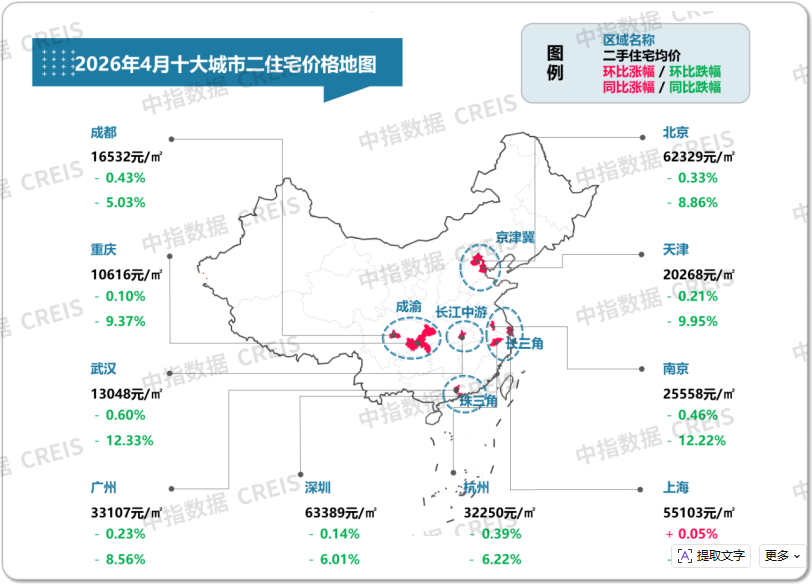

Second-hand housing prices in the top ten cities fell slightly in April, and Shanghai rose month-on-month

Figure: Average price of second-hand housing listings in the top ten cities in April 2026 and the month-on-month ratio

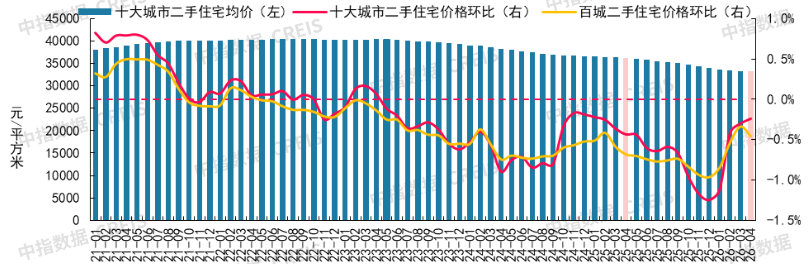

Figure: Average prices and month-on-month changes of second-hand housing in the top ten cities from January 2021 to April 2026

Data source: Middle Index Data CREIS

According to the Baicheng Price Index of the China Real Estate Index system, in April 2026, the average price of second-hand housing in Baicheng fell 0.46% month-on-month and 8.34% year-on-year; the average price of second-hand housing in the top ten cities fell 0.24% month-on-month, down 8.07% year on year.

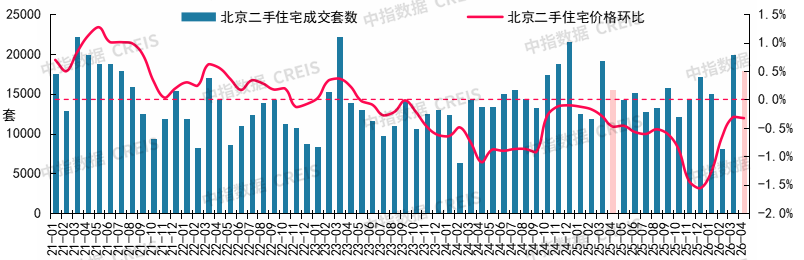

Beijing: Second-hand housing sales hit a month-on-month high in the past five years and April, and the month-on-month decline in prices was basically the same as last month

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Beijing from January 2021 to April 2026

Data source: Middle Index Data CREIS

In terms of transactions, in April 2026, 18,000 second-hand housing units were sold in Beijing, up 14.9% year on year, hitting a monthly high in the past five years and April. The “Xiaoyangchun” market continued to be popular. In January-April, 61,000 second-hand housing units were sold, up 3.1% year on year. In terms of prices, second-hand housing prices in Beijing fell 0.33% month-on-month in April. The decline was basically the same as last month. The year-on-year decline was 8.86%, and the decline was 0.14 percentage points narrower than the previous month.

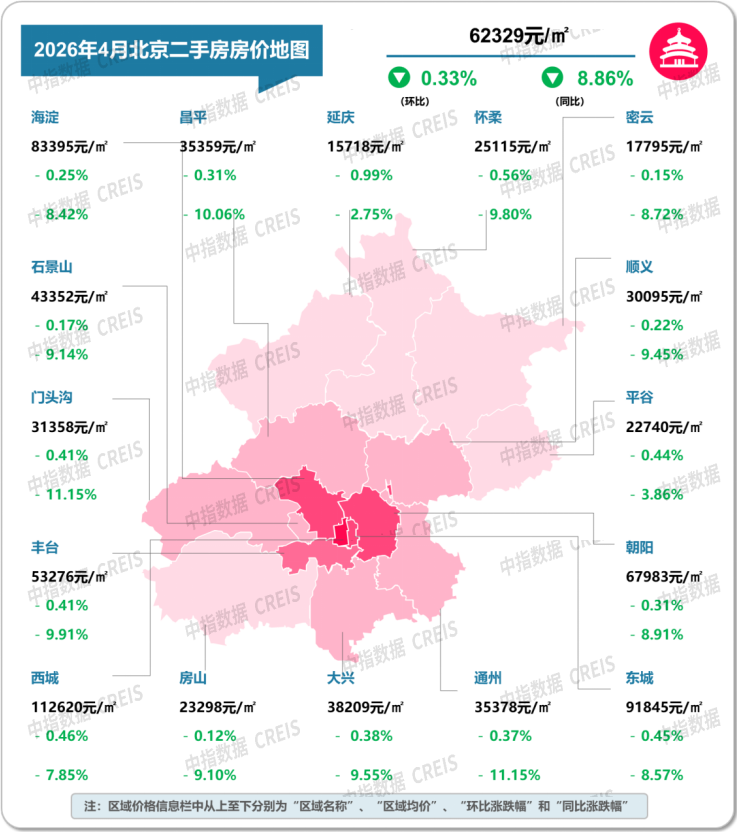

Figure: Average price of second-hand housing listings in Beijing's municipal districts in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

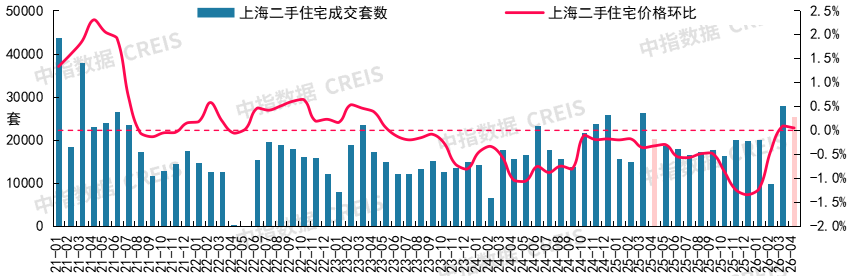

Shanghai: The second-hand housing market continues the “Xiaoyangchun” market. The transaction scale was high in the same period in April in recent years, and prices continued to rise

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Shanghai from January 2021 to April 2026

Data source: Middle Index Data CREIS

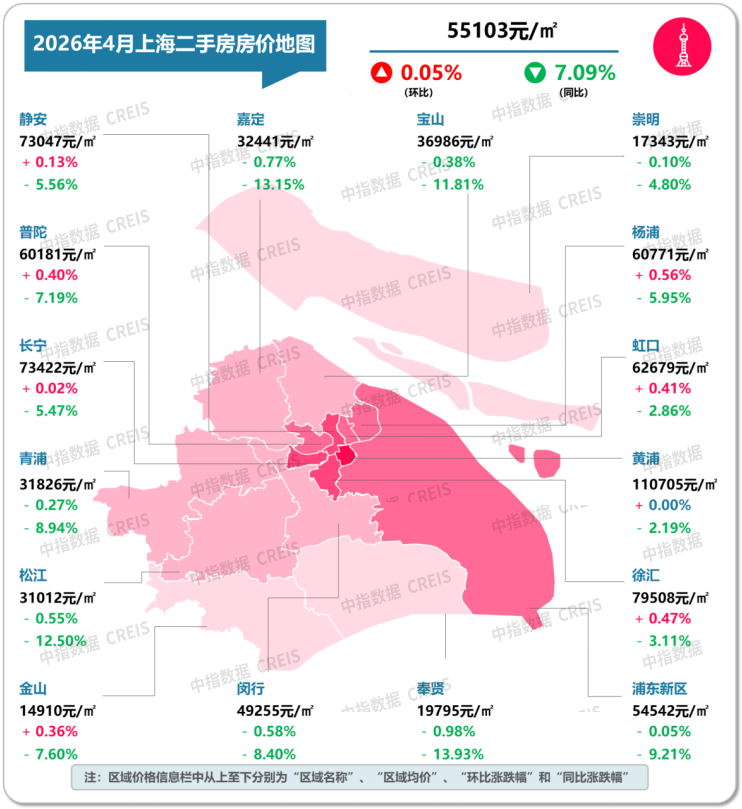

In terms of transactions, 25,000 second-hand residential units were sold in Shanghai in April 2026, an increase of 24.6% over the previous year. The transaction scale was high in the same period in April in recent years, and the market remained highly active. January-April turnover increased 7.6% year over year. In terms of prices, in April, the average price of second-hand residential listings in Shanghai continued to rise 0.05% month-on-month, and fell 7.09% year-on-year.

Figure: Average price of second-hand residential listings in Shanghai in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

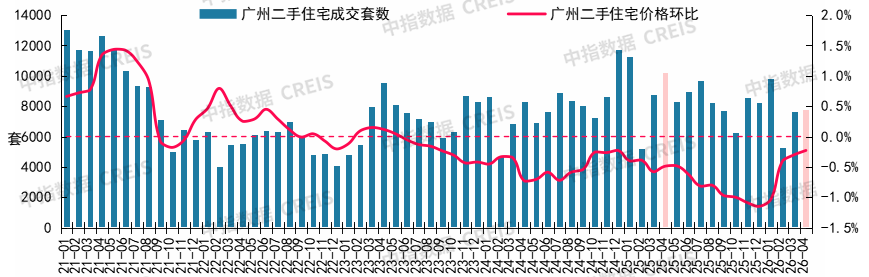

Guangzhou: The recovery of the second-hand housing market was weak in April, and the results were initially evident after the New Deal at the end of the month

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Guangzhou from January 2021 to April 2026

Data source: Middle Index Data CREIS

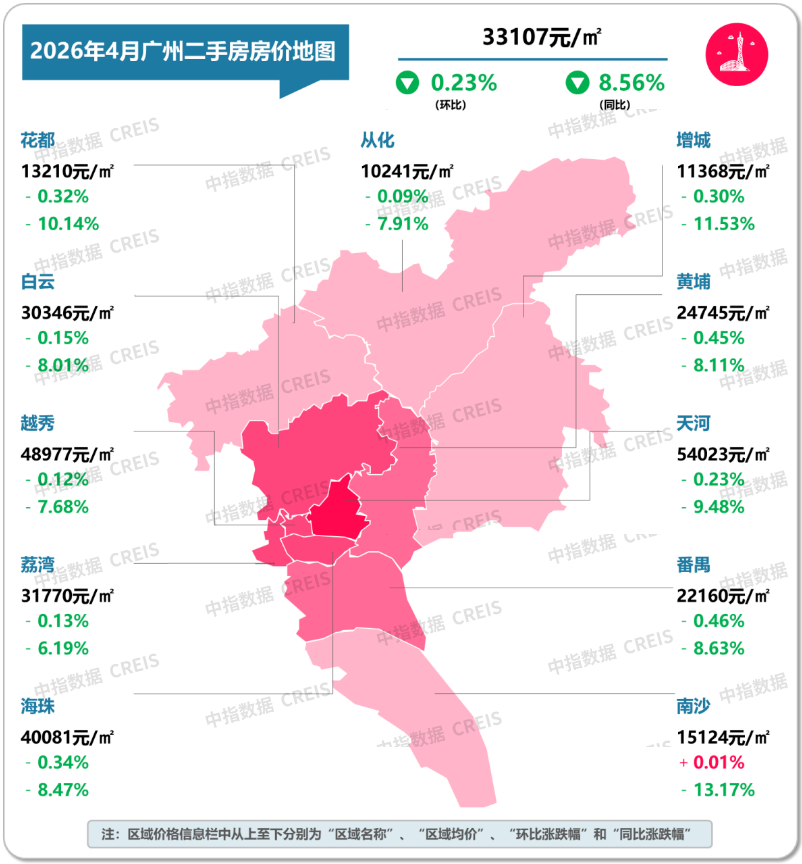

In terms of transactions, in April 2026, Guangzhou sold 7,754 second-hand residential units, a year-on-year decrease of 23.9%, and the cumulative turnover in January-April fell 13.9% year on year. Facing a market that continues to be under pressure, Guangzhou introduced the “Sui Eight Rules” on April 30. The results were initially evident after the new policy. According to data from the Guangzhou Housing and Construction Bureau, the average number of second-hand housing visitors and daily subscriptions in Guangzhou during the May 1st holiday increased 15.6% and 5.2%, respectively, compared to April, and the number of subscriptions increased 63.4% year on year. In terms of prices, in April, second-hand housing prices in Guangzhou fell 0.23% month-on-month and 8.56% year-on-year. The year-on-month decline was narrower than the previous month.

Figure: Average price of second-hand housing listings in Guangzhou's municipal districts in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

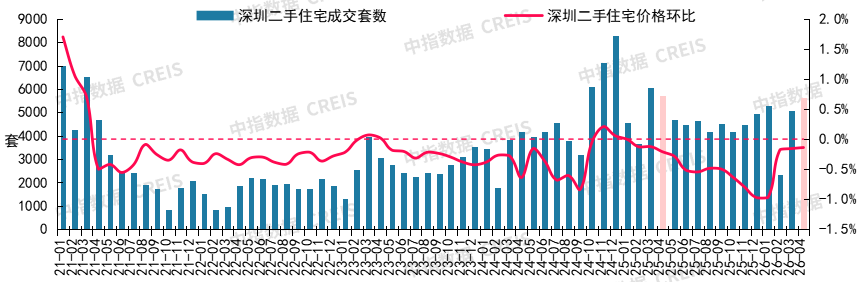

Shenzhen: The month-on-month decline in prices in April was basically the same as last month. Market activity increased significantly after the 4.29 New Deal

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Shenzhen from January 2021 to April 2026

Data source: Middle Index Data CREIS

In terms of transactions, in April 2026, 5,644 second-hand residential units were sold in Shenzhen. Under the influence of a high base, the year-on-year decrease was 1.6%, and the cumulative turnover in January-April fell 8.5% year on year. On April 29, Shenzhen relaxed purchase restrictions in some core regions and increased the amount of provident fund loans. Second-hand residential transactions increased 18.3% year-on-year from May 1 to 17, and market activity increased significantly after the New Deal. In terms of prices, in April 2026, second-hand housing prices in Shenzhen fell 0.14% month-on-month and 6.01% year-on-year, and the month-on-month decline was basically the same as last month.

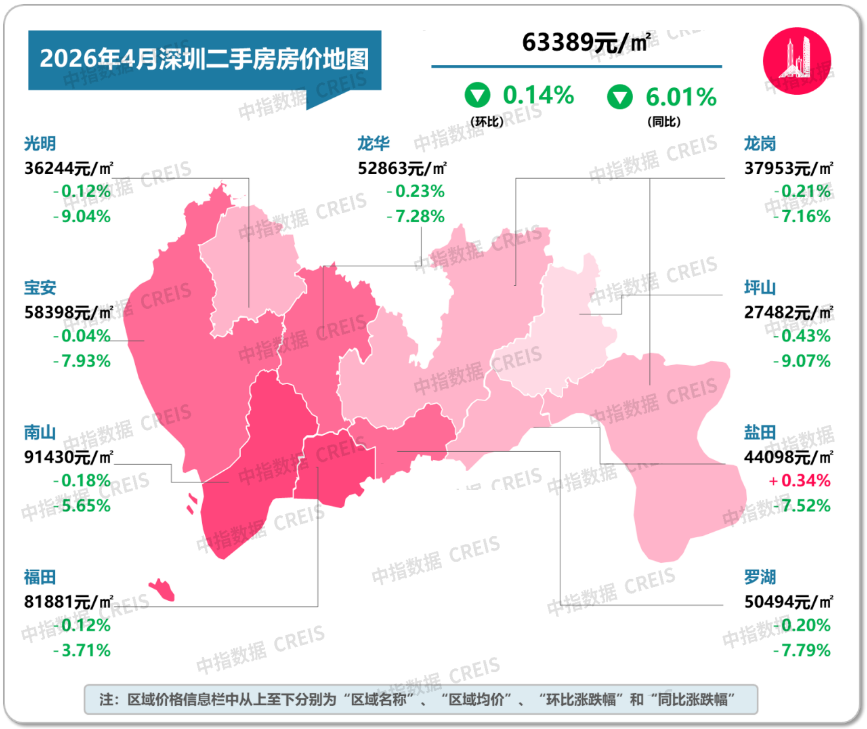

Figure: Average price of second-hand residential listings in various municipal districts in Shenzhen in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

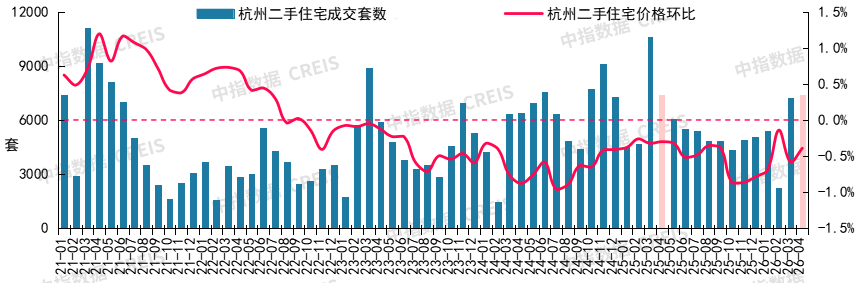

Hangzhou: Second-hand housing turnover is basically the same as last year, and price volatility continues to decline

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Hangzhou from January 2021 to April 2026

Data source: Middle Index Data CREIS

In terms of transactions, in April 2026, 7,433 second-hand residential units were sold in Hangzhou, an increase of 0.1% over the previous year. In January-April, a total of 22,000 second-hand housing units were sold, a year-on-year decrease of 18.0%. In terms of prices, in April, second-hand housing prices fell 0.39% month-on-month. The month-on-month decline was 0.19 percentage points narrower than the previous month, and 6.22% year-on-year, and the decline was 0.09 percentage points higher than the previous month.

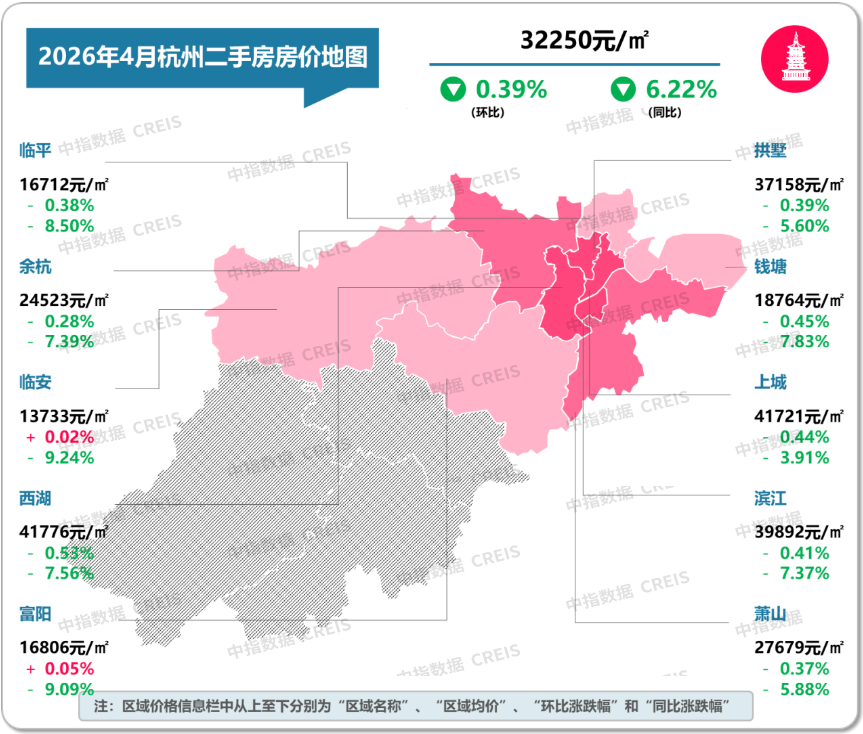

Figure: Average price of second-hand residential listings in Hangzhou in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

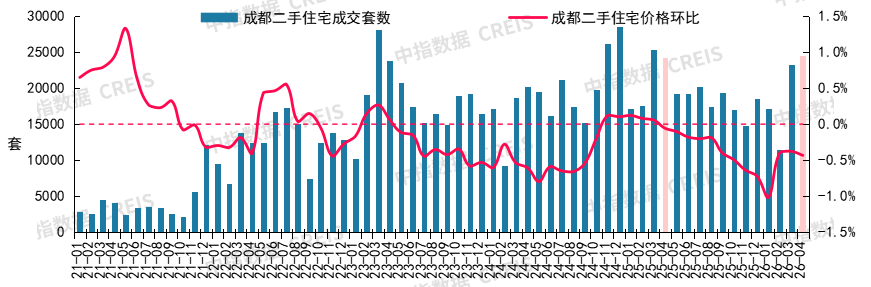

Chengdu: Demand for second-hand housing purchases continued to be released in April, and the year-on-month decline in prices increased slightly compared to the previous month

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Chengdu from January 2021 to April 2026

Data source: Middle Index Data CREIS

In terms of transactions, in April 2026, second-hand housing activity in Chengdu remained high, and demand for home purchases continued to be released. Second-hand housing sold 24,000 units, up 1.0% year on year, and the cumulative turnover from January to April decreased by 9.5% year on year. In terms of prices, second-hand housing prices in Chengdu fell 0.43% month-on-month and 5.03% year-on-year in April. The month-on-month decline was slightly larger than the previous month.

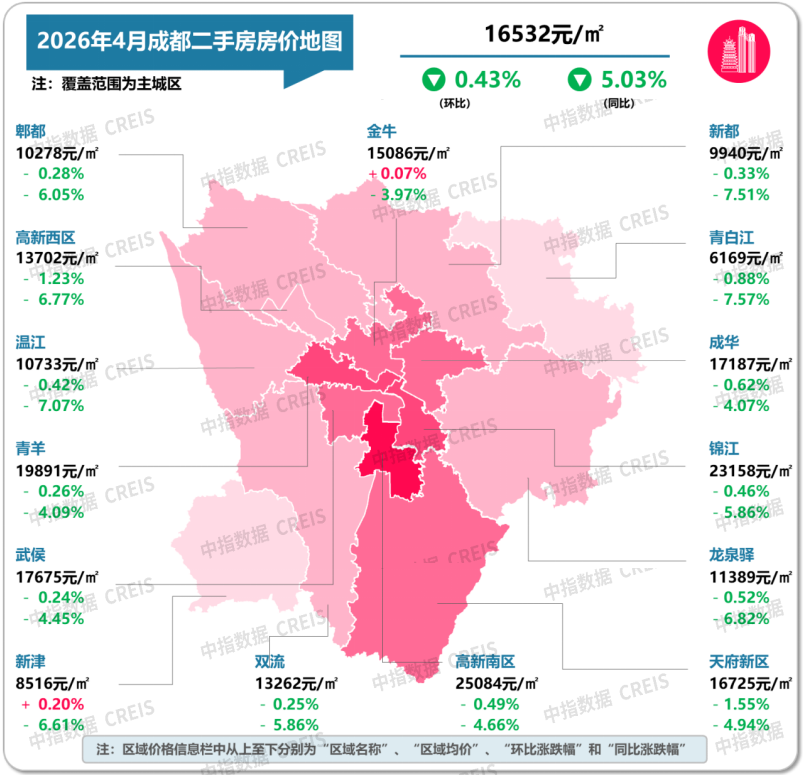

Figure: Average price of second-hand residential listings in various municipal districts of Chengdu in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

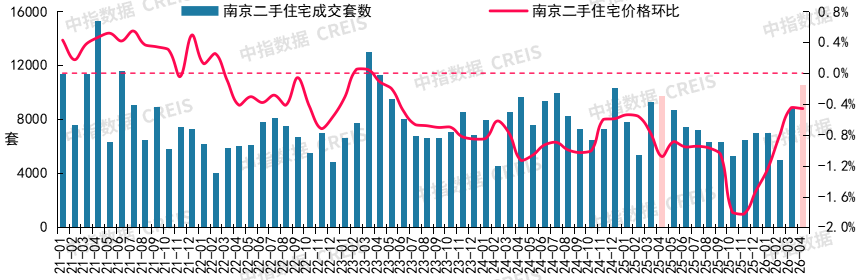

Nanjing: The second-hand housing market remains stable, and the month-on-month decline in prices is basically the same as last month

Figure: The month-on-month trend in the number and price of second-hand residential units sold in Nanjing from January 2021 to April 2026

Data source: Middle Index Data CREIS

In terms of transactions, in April 2026, 10,599 second-hand residential units were sold in Nanjing, an increase of 8.8% over the previous year. The cumulative year-on-year decline in January-April was 2.4%, and the market continued to recover. In terms of prices, in April, second-hand housing prices in Nanjing fell 0.46% month-on-month. The decline was basically the same as the previous month. The year-on-year decline was 12.22%, and the decline was 0.55 percentage points narrower than the previous month.

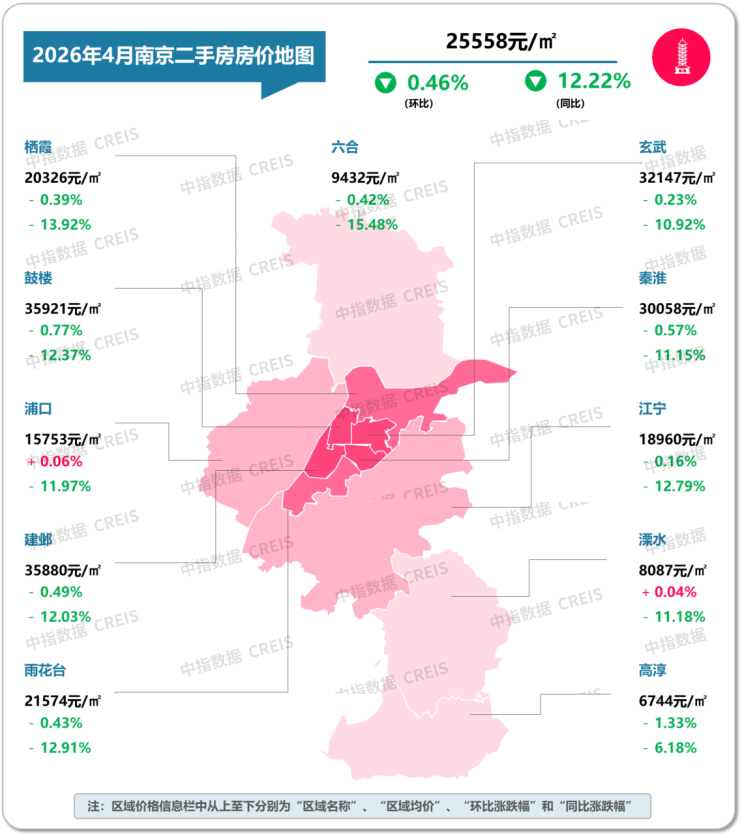

Figure: Average price of second-hand residential listings in Nanjing in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

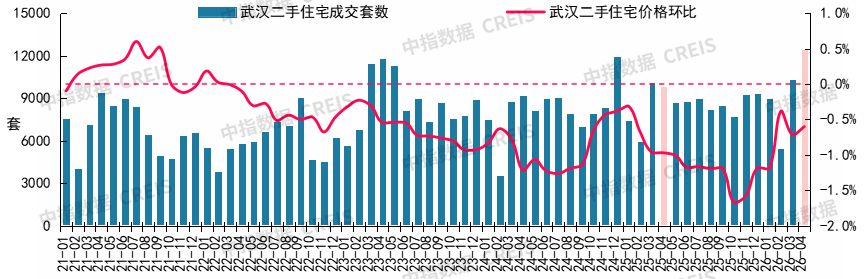

Wuhan: The release of demand for second-hand housing purchases accelerated markedly in April. The volume reached a record high, and prices fell 0.60% month-on-month

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Wuhan from January 2021 to April 2026

Data source: Middle Index Data CREIS

In terms of transactions, in April 2026, 12,000 second-hand housing units were sold in Wuhan, a monthly high in recent years, with a year-on-year increase of 26.8%. The cumulative year-on-year increase in January-April was 11.9%, and the overall second-hand housing market remained highly active. Wuhan issued the “Seven Rules of Han” New Deal at the end of April, which will help release demand for home buyers. In terms of prices, in April, second-hand housing prices in Wuhan fell 0.60% month-on-month, and the month-on-month decline narrowed by 0.12 percentage points.

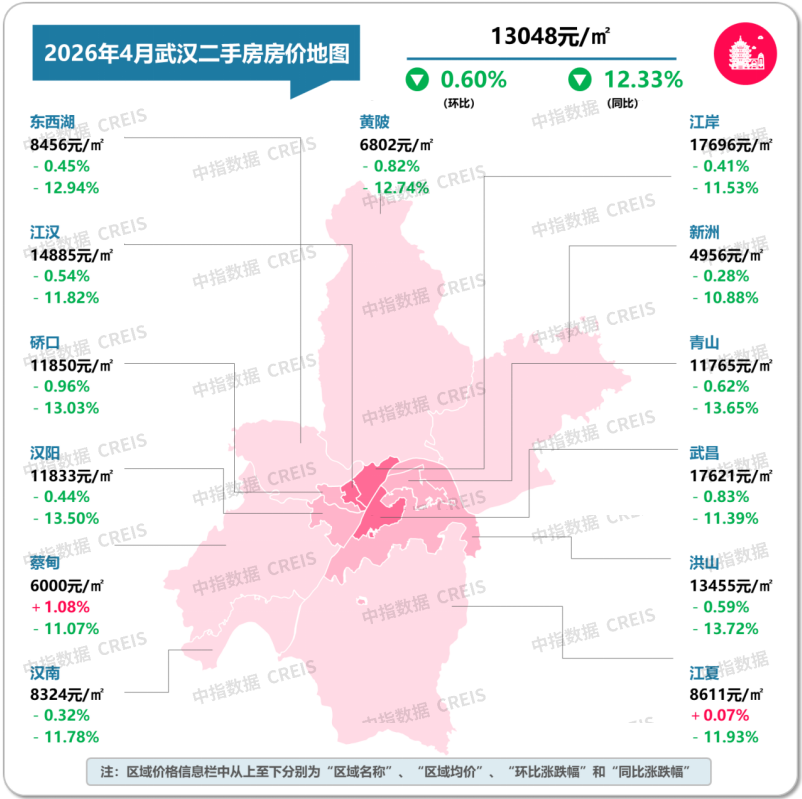

Figure: Average price of second-hand residential listings in various municipal districts in Wuhan in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

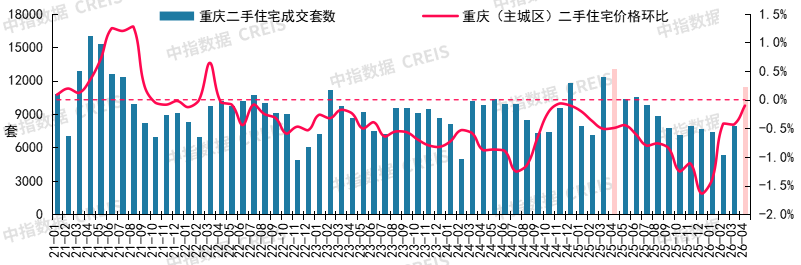

Chongqing (main urban area): The second-hand housing market recovered in April compared to the previous period, and the month-on-month price decline narrowed compared to the previous month

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Chongqing from January 2021 to April 2026

Data source: Middle Index Data CREIS

In terms of transactions, in April 2026, 11,000 second-hand residential units were sold in Chongqing (main urban area), an increase of 43% month-on-month and a year-on-year decrease of 12.6%. Compared with the obvious restoration in the first quarter, the cumulative year-on-year decrease in January-April was still 20.6%. In terms of prices, in April, second-hand housing prices in Chongqing (main urban area) fell 0.10% month-on-month and 9.37% year-on-year. The month-on-month decline was narrower than the previous month.

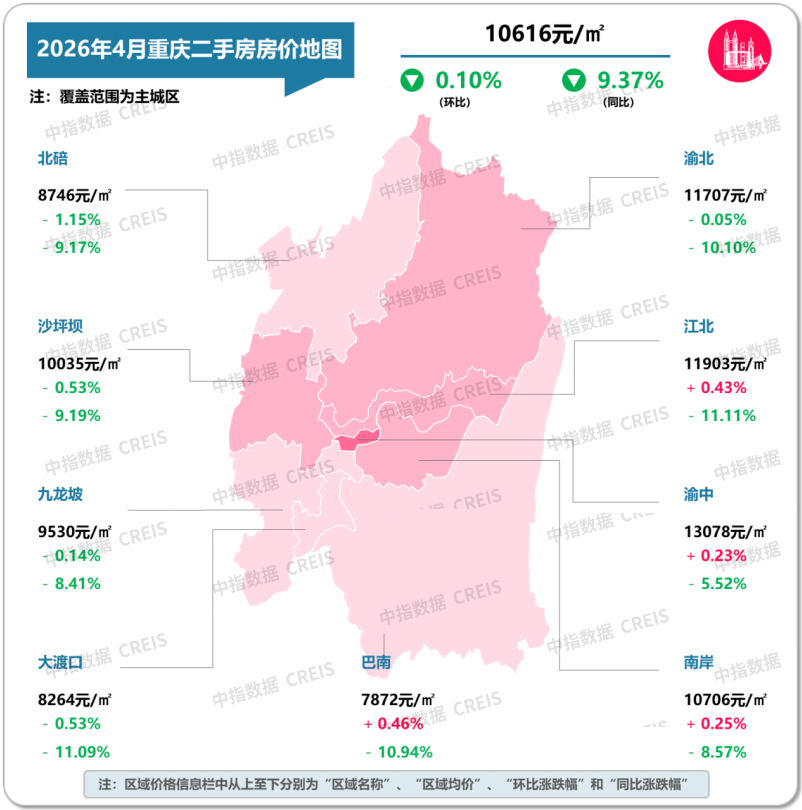

Figure: Average price of second-hand residential listings in Chongqing (main urban area) in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

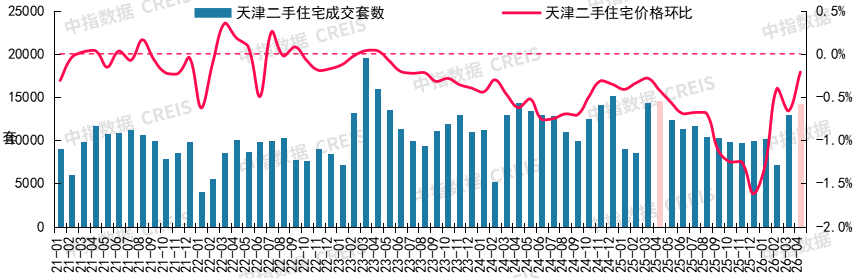

Tianjin: Market volume and price remained stable, and the month-on-month price decline was narrower than last month

Figure: Month-on-month trend in the number and price of second-hand residential units sold in Tianjin from January 2021 to April 2026

Data source: Middle Index Data CREIS

In terms of transactions, in April 2026, 14,000 second-hand residential units were sold in Tianjin, down 3.0% year on year, and cumulative sales volume from January to April decreased 4.7% year on year. In terms of prices, in April, second-hand housing prices in Tianjin fell 0.21% month-on-month. The month-on-month decline was 0.45 percentage points narrower than the previous month, 9.95% year-on-year, and 0.19 percentage points narrower than the previous month.

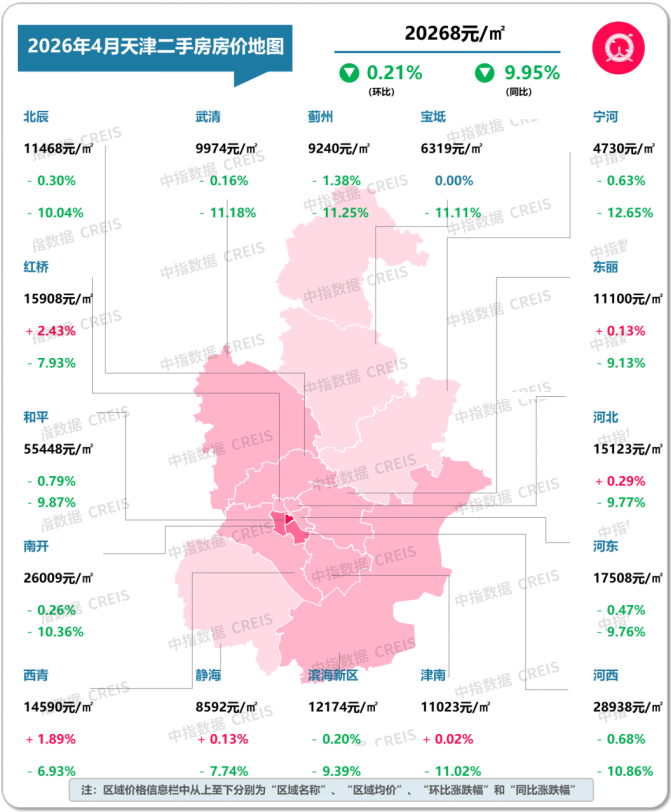

Figure: Average price of second-hand residential listings in various municipal districts in Tianjin in April 2026 and the month-on-month ratio

Data source: Middle Index Data CREIS

outlooks

Overall, the Politburo meeting set the tone for “striving to stabilize the real estate market and solidly push forward urban renewal.” “Strive for stability” continues the previous policy tone of “stabilizing the market”, indicating that stabilizing the market is still an important task. It is expected that the second-quarter policy will focus on consolidating the bottom-building trend; urban renewal emphasizes “steady progress,” which means that the pace of work is becoming more steady and effective. Due to the impact of this year's Spring Festival for about two weeks from last night, demand release has been delayed. Since April, the second-hand housing market in key cities such as Beijing and Shanghai has continued its active trend since spring, and the Guangshen market improved after policy optimization at the end of April.

Looking at the trend, second-hand housing transactions in core cities are expected to remain active, and prices are expected to continue to fluctuate slightly. The current demand release is still mainly price-driven. The basis for market repair is not yet strong. The continued improvement of the market still depends on improvements in residents' expectations, and differentiation will continue to be the main characteristic of the market throughout the year.