- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalKimura Chemical Plants (TSE:6378) Has Announced A Dividend Of ¥41.00

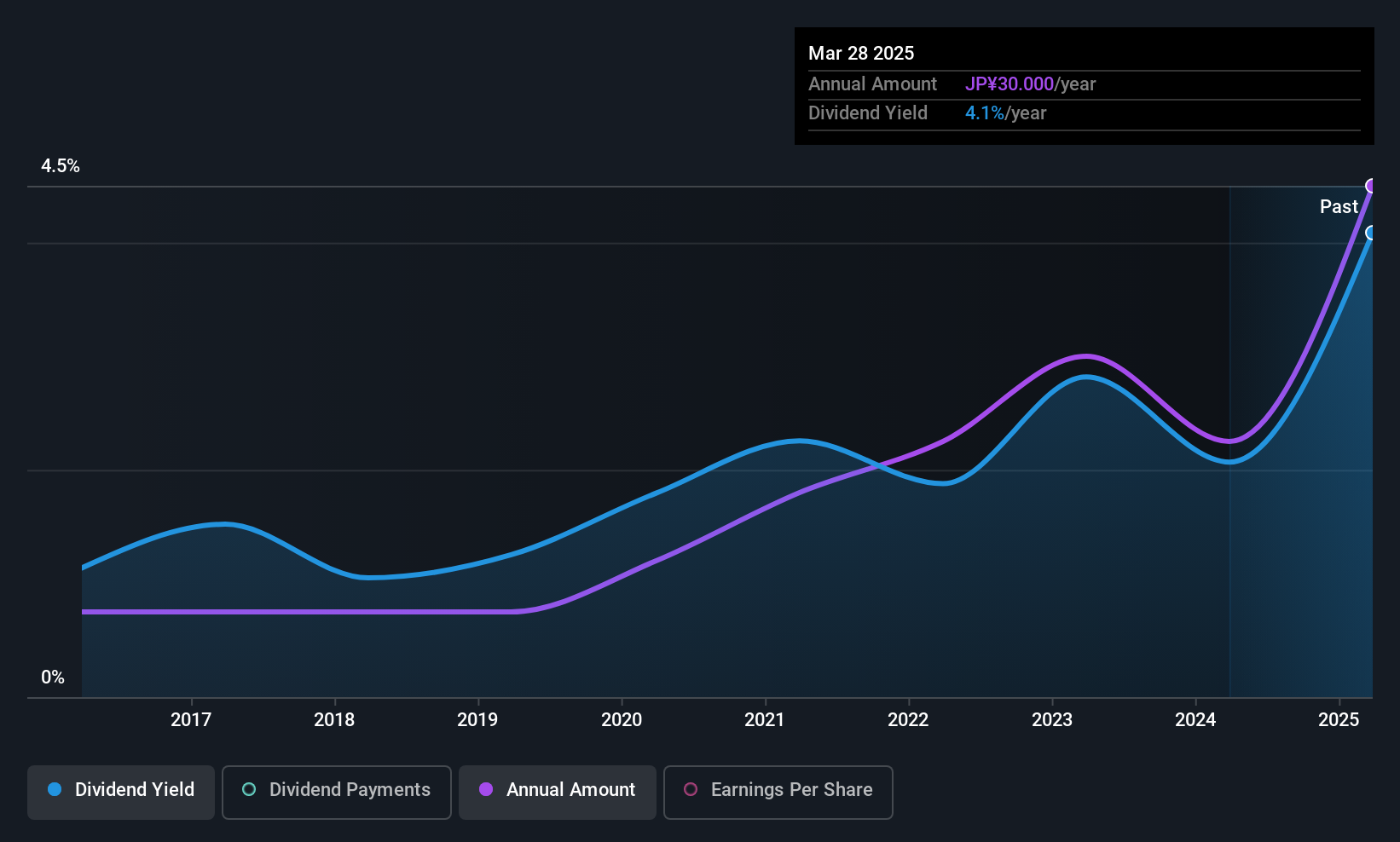

Kimura Chemical Plants Co., Ltd.'s (TSE:6378) investors are due to receive a payment of ¥41.00 per share on 11th of June. This makes the dividend yield 3.2%, which will augment investor returns quite nicely.

Kimura Chemical Plants' Future Dividend Projections Appear Well Covered By Earnings

If the payments aren't sustainable, a high yield for a few years won't matter that much. However, prior to this announcement, Kimura Chemical Plants was quite comfortably covering its dividend with earnings and it was paying more than 75% of its free cash flow to shareholders. The business is earning enough to make the dividend feasible, but the cash payout ratio of 86% shows that most of the cash is going back to the shareholders, which could constrain growth prospects going forward.

If the trend of the last few years continues, EPS will grow by 18.1% over the next 12 months. If the dividend continues on this path, the payout ratio could be 39% by next year, which we think can be pretty sustainable going forward.

See our latest analysis for Kimura Chemical Plants

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2016, the dividend has gone from ¥5.00 total annually to ¥41.00. This implies that the company grew its distributions at a yearly rate of about 23% over that duration. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. We are encouraged to see that Kimura Chemical Plants has grown earnings per share at 18% per year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for Kimura Chemical Plants' prospects of growing its dividend payments in the future.

Our Thoughts On Kimura Chemical Plants' Dividend

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Kimura Chemical Plants' payments, as there could be some issues with sustaining them into the future. While Kimura Chemical Plants is earning enough to cover the dividend, we are generally unimpressed with its future prospects. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. As an example, we've identified 2 warning signs for Kimura Chemical Plants that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.