- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 Promising Asian Penny Stocks With Market Caps Under US$400M

As we enter 2026, Asian markets are reflecting a mix of cautious optimism and strategic positioning, with investors closely watching economic indicators and policy shifts. Amidst this backdrop, penny stocks—often representing smaller or newer companies—continue to capture attention for their potential to offer significant growth opportunities at lower price points. While the term "penny stock" might seem outdated, these investments can still present valuable prospects when backed by strong financials and solid fundamentals.

Top 10 Penny Stocks In Asia

| Name | Share Price | Market Cap | Rewards & Risks |

| YKGI (Catalist:YK9) | SGD0.154 | SGD65.7M | ✅ 2 ⚠️ 4 View Analysis > |

| Lever Style (SEHK:1346) | HK$1.46 | HK$903.04M | ✅ 4 ⚠️ 1 View Analysis > |

| Asia Medical and Agricultural Laboratory and Research Center (SET:AMARC) | THB2.48 | THB1.04B | ✅ 3 ⚠️ 2 View Analysis > |

| TK Group (Holdings) (SEHK:2283) | HK$2.51 | HK$2.08B | ✅ 4 ⚠️ 1 View Analysis > |

| Atlantic Navigation Holdings (Singapore) (Catalist:5UL) | SGD0.109 | SGD57.06M | ✅ 2 ⚠️ 3 View Analysis > |

| Yangzijiang Shipbuilding (Holdings) (SGX:BS6) | SGD3.61 | SGD14.21B | ✅ 5 ⚠️ 1 View Analysis > |

| NagaCorp (SEHK:3918) | HK$4.75 | HK$21.01B | ✅ 5 ⚠️ 1 View Analysis > |

| Livestock Improvement (NZSE:LIC) | NZ$1.00 | NZ$137.01M | ✅ 2 ⚠️ 5 View Analysis > |

| Bosideng International Holdings (SEHK:3998) | HK$4.34 | HK$50.38B | ✅ 4 ⚠️ 2 View Analysis > |

| Scott Technology (NZSE:SCT) | NZ$2.84 | NZ$237.15M | ✅ 4 ⚠️ 1 View Analysis > |

Click here to see the full list of 952 stocks from our Asian Penny Stocks screener.

Let's review some notable picks from our screened stocks.

LC Logistics (SEHK:2490)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: LC Logistics, Inc. is a freight forwarding company offering integrated cross-border seaborne logistics and time charter services globally, with a market cap of HK$2.76 billion.

Operations: The company generates revenue primarily from its transportation - shipping segment, which amounts to CN¥2.10 billion.

Market Cap: HK$2.76B

LC Logistics has demonstrated significant earnings growth, with a remarkable 1961.4% increase over the past year, outpacing the shipping industry. The company maintains strong financial health, with short-term assets exceeding both short- and long-term liabilities, and more cash than total debt. Its operating cash flow covers its debt well. However, despite a high return on equity of 33.1%, the dividend yield of 4.56% is not well supported by free cash flows. The company's price-to-earnings ratio of 5x suggests it may be undervalued compared to the Hong Kong market average of 12.2x.

- Dive into the specifics of LC Logistics here with our thorough balance sheet health report.

- Understand LC Logistics' track record by examining our performance history report.

Biosino Bio-Technology and Science Incorporation (SEHK:8247)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Biosino Bio-Technology and Science Incorporation, along with its subsidiaries, is engaged in the manufacturing, selling, and distribution of in-vitro diagnostic reagents in Mainland China, with a market cap of HK$528.18 million.

Operations: The company generates revenue from its In-Vitro Diagnostic Reagent Products segment, amounting to CN¥225.06 million.

Market Cap: HK$528.18M

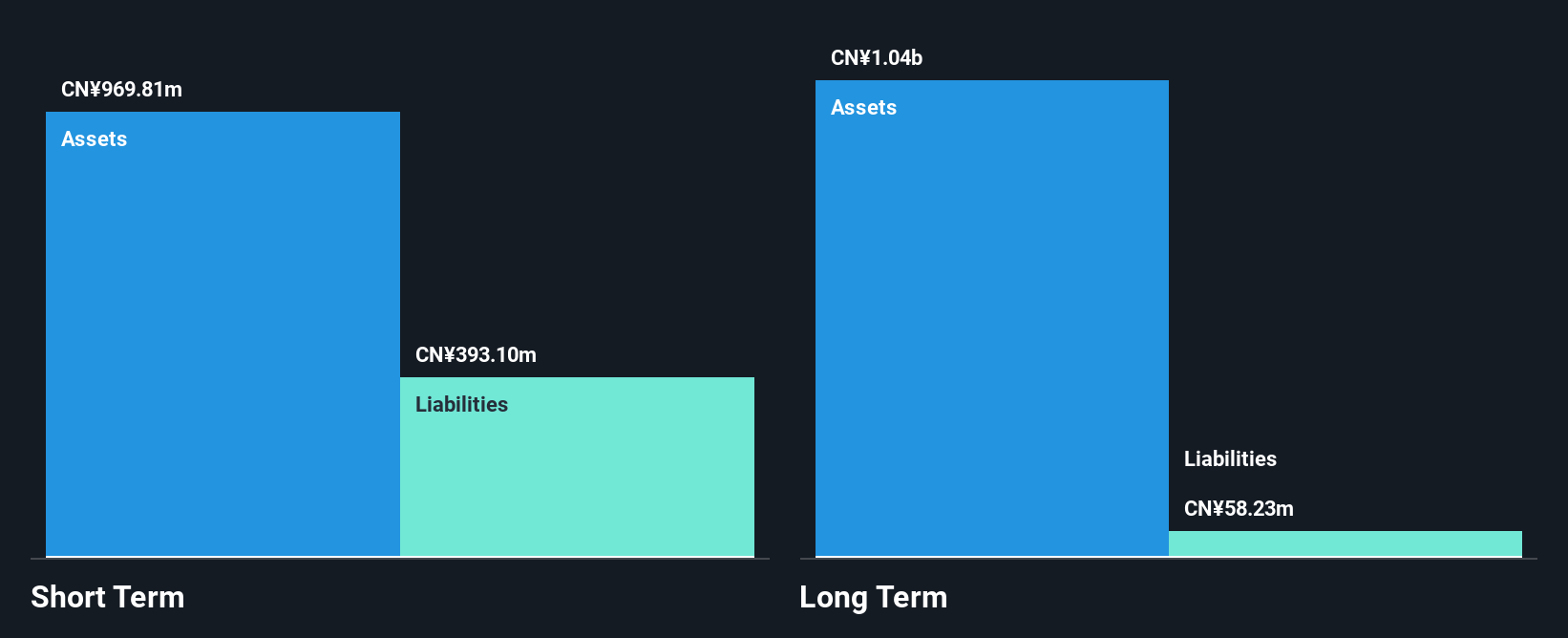

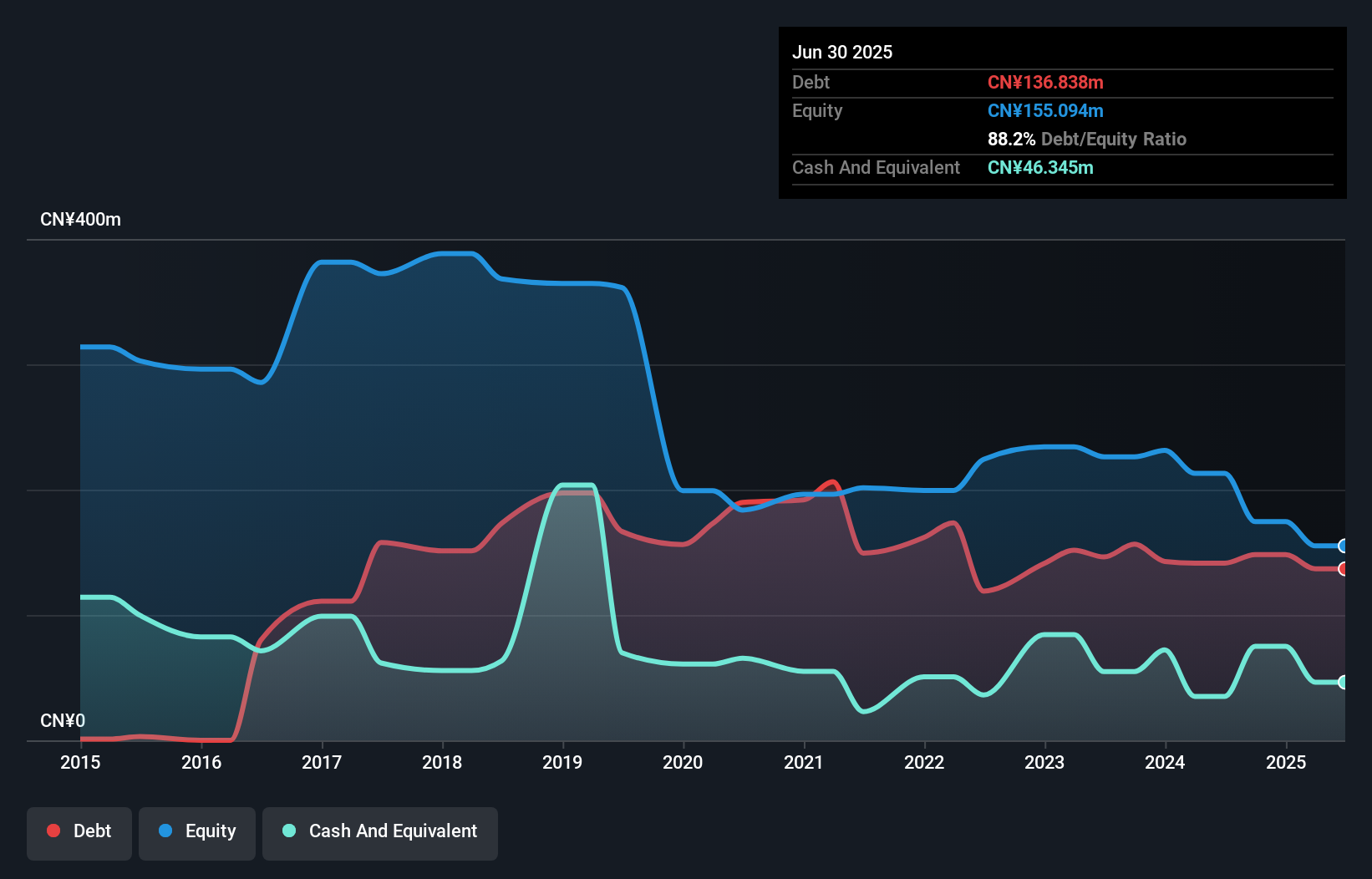

Biosino Bio-Technology and Science Incorporation is currently unprofitable, though it has managed to reduce its losses by 8.6% annually over the past five years. Despite a high net debt to equity ratio of 58.3%, the company has improved its debt position from 103.3% to 88.2%. Its cash runway is secure for over three years due to positive free cash flow growth of 15.1% per year, although short-term assets (CN¥245.9M) fall short of covering short-term liabilities (CN¥272.7M). The stock trades at a significant discount, approximately 44.2% below estimated fair value, but remains highly volatile with weekly volatility at 24%.

- Navigate through the intricacies of Biosino Bio-Technology and Science Incorporation with our comprehensive balance sheet health report here.

- Explore historical data to track Biosino Bio-Technology and Science Incorporation's performance over time in our past results report.

Wee Hur Holdings (SGX:E3B)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Wee Hur Holdings Ltd. is an investment holding company involved in general building and civil engineering construction in Singapore and Australia, with a market cap of SGD744.59 million.

Operations: The company's revenue is primarily derived from building construction (SGD137.48 million), workers dormitory operations (SGD84.26 million), property development in Singapore (SGD76.46 million), fund management (SGD43.72 million), PBSA operations (SGD2.12 million), property development in Australia (SGD0.93 million), and corporate activities (SGD3.55 million).

Market Cap: SGD744.59M

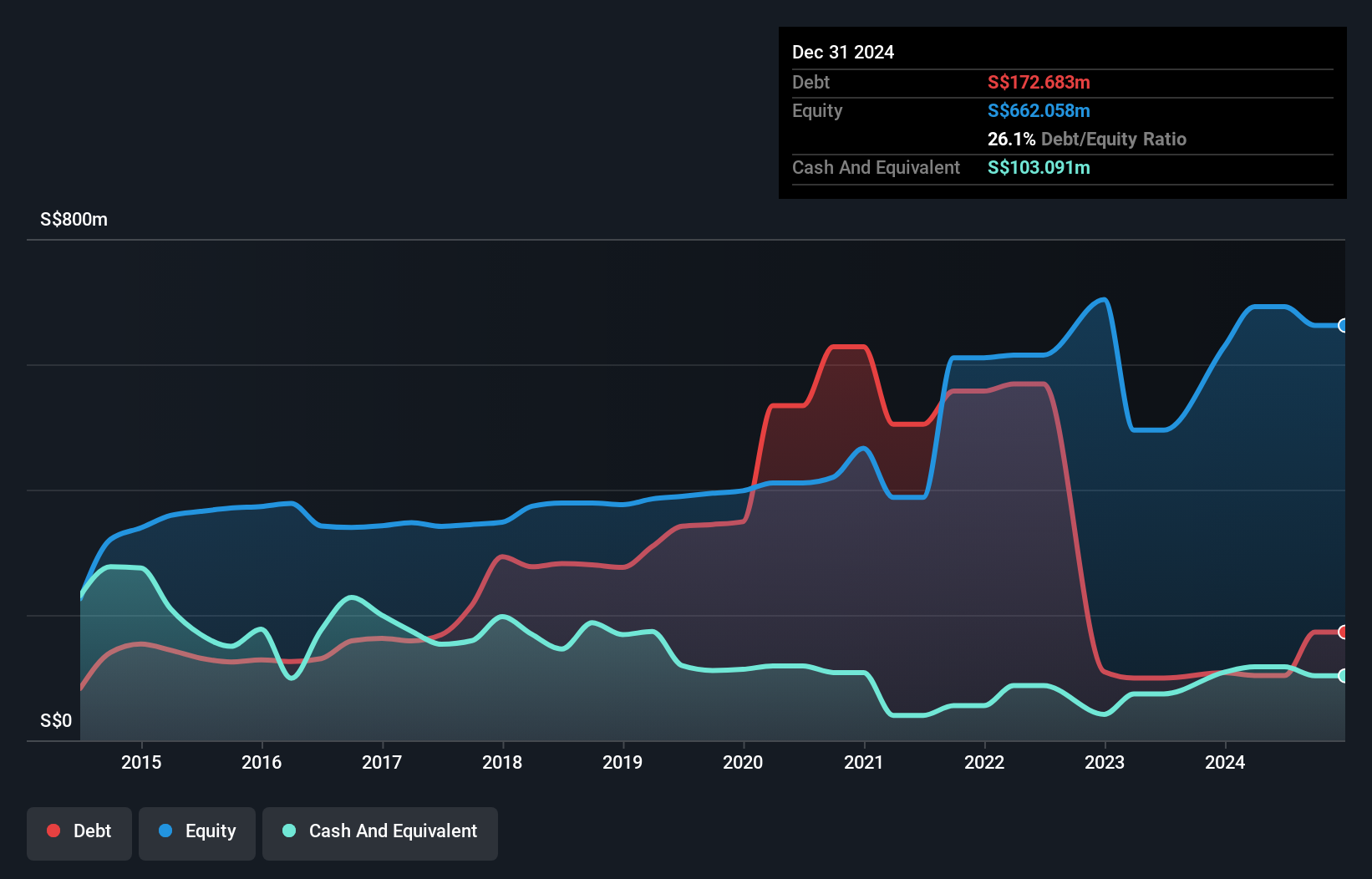

Wee Hur Holdings Ltd. has demonstrated financial stability with short-term assets (SGD550.1M) exceeding both short and long-term liabilities, indicating a solid liquidity position. The company has effectively reduced its debt to equity ratio from 130% to 34.6% over five years, and its debt is well covered by operating cash flow (37.1%). Despite recent negative earnings growth (-86.2%), Wee Hur's strategic initiatives, such as the joint venture for land development in Upper Thomson Road and partnership in establishing Wycombe Abbey School (Singapore), highlight its focus on diversifying revenue streams beyond traditional construction activities, potentially enhancing future profitability amidst current challenges like lower profit margins and large one-off losses impacting recent results.

- Click to explore a detailed breakdown of our findings in Wee Hur Holdings' financial health report.

- Evaluate Wee Hur Holdings' prospects by accessing our earnings growth report.

Where To Now?

- Click through to start exploring the rest of the 949 Asian Penny Stocks now.

- Searching for a Fresh Perspective? AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com